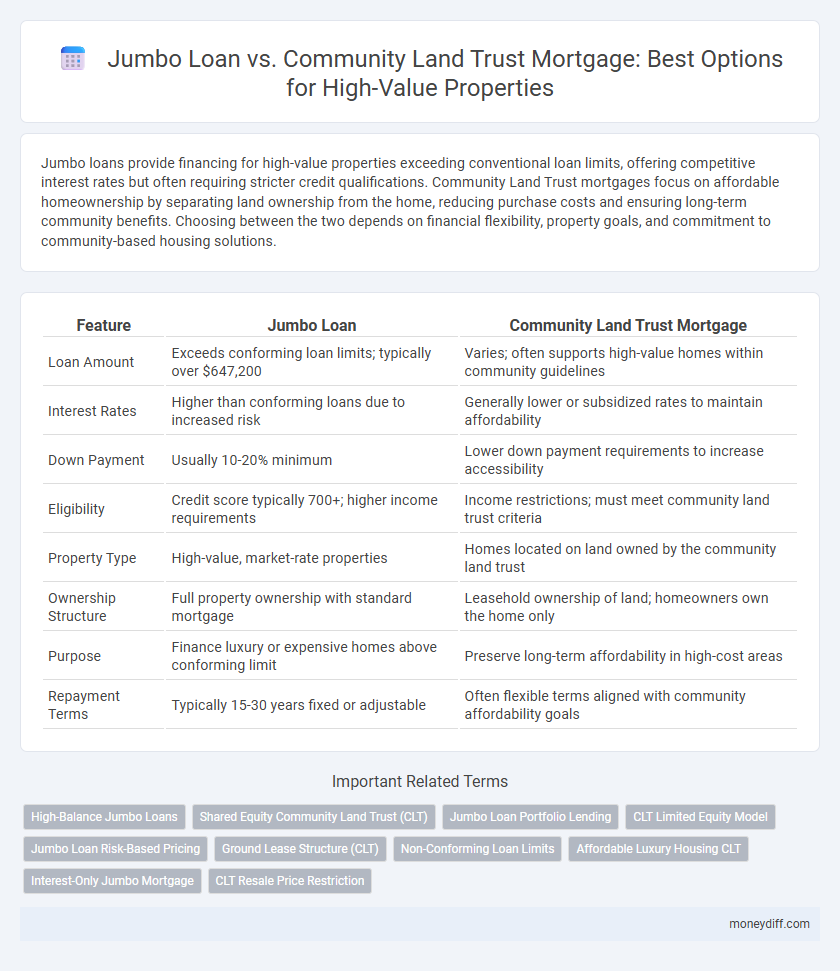

Jumbo loans provide financing for high-value properties exceeding conventional loan limits, offering competitive interest rates but often requiring stricter credit qualifications. Community Land Trust mortgages focus on affordable homeownership by separating land ownership from the home, reducing purchase costs and ensuring long-term community benefits. Choosing between the two depends on financial flexibility, property goals, and commitment to community-based housing solutions.

Table of Comparison

| Feature | Jumbo Loan | Community Land Trust Mortgage |

|---|---|---|

| Loan Amount | Exceeds conforming loan limits; typically over $647,200 | Varies; often supports high-value homes within community guidelines |

| Interest Rates | Higher than conforming loans due to increased risk | Generally lower or subsidized rates to maintain affordability |

| Down Payment | Usually 10-20% minimum | Lower down payment requirements to increase accessibility |

| Eligibility | Credit score typically 700+; higher income requirements | Income restrictions; must meet community land trust criteria |

| Property Type | High-value, market-rate properties | Homes located on land owned by the community land trust |

| Ownership Structure | Full property ownership with standard mortgage | Leasehold ownership of land; homeowners own the home only |

| Purpose | Finance luxury or expensive homes above conforming limit | Preserve long-term affordability in high-cost areas |

| Repayment Terms | Typically 15-30 years fixed or adjustable | Often flexible terms aligned with community affordability goals |

Understanding Jumbo Loans: Key Features and Requirements

Jumbo loans are non-conforming mortgages that exceed the conforming loan limits set by the Federal Housing Finance Agency, typically required for high-value properties above $726,200 in most U.S. markets. These loans demand stringent credit scores, lower debt-to-income ratios, and larger down payments, often ranging from 10% to 20%, to mitigate lender risk. Understanding the loan's requirements, such as extensive documentation and higher interest rates compared to conforming loans, is critical for borrowers navigating high-value property financing.

What Is a Community Land Trust Mortgage?

A Community Land Trust (CLT) mortgage involves financing where the borrower owns the home but leases the land from a nonprofit trust, allowing for more affordable access to high-value properties. Unlike jumbo loans, which require higher credit scores and larger down payments due to exceeding conforming loan limits, CLT mortgages help stabilize housing costs by removing land ownership from the financing equation. This model supports long-term affordability and community control while providing an alternative path to homeownership in competitive markets.

Eligibility Criteria for Jumbo Loans vs. Community Land Trust Mortgages

Jumbo loans require borrowers to meet higher credit scores, lower debt-to-income ratios, and substantial down payments, typically exceeding conforming loan limits for high-value properties. Community Land Trust (CLT) mortgages focus on income eligibility and community residency requirements, offering more flexible credit scores and lower down payments by separating land ownership from housing ownership. These differences reflect Jumbo loans' emphasis on borrower financial strength, while CLT mortgages prioritize affordability and long-term community stewardship.

Down Payment Differences: Jumbo Loan vs. CLT Mortgage

Jumbo loans typically require a down payment of 20% or more for high-value properties due to their non-conforming loan status, making upfront costs significantly higher. In contrast, Community Land Trust (CLT) mortgages often require a lower down payment, sometimes as low as 1-5%, since borrowers purchase the home but lease the land, reducing overall loan amounts and barriers to entry. This fundamental difference in down payment structures directly impacts buyer affordability and access to premium real estate markets.

Interest Rates and Terms: Which Is More Cost-Effective?

Jumbo loans typically feature higher interest rates and stricter qualification criteria due to the increased risk of financing high-value properties. Community Land Trust (CLT) mortgages often offer lower interest rates and more flexible terms, making homeownership more affordable in high-cost areas through shared equity models. Evaluating cost-effectiveness involves comparing the long-term interest savings and equity retention benefits of CLT mortgages against the often higher monthly payments and total interest costs associated with jumbo loans.

Property Value Limits: Navigating High-Value Transactions

Jumbo loans cater to high-value properties exceeding conforming loan limits, typically above $726,200 in most U.S. regions, enabling buyers to finance luxury homes without conforming loan restrictions. Community Land Trust mortgages focus on affordability by limiting property value and resale price, often capping values below market rates to maintain community access and prevent speculation. Understanding these property value limits is essential for navigating high-value transactions, as jumbo loans allow unrestricted market prices while community land trusts impose caps to ensure long-term affordability.

Credit Score and Income Considerations

Jumbo loans typically require higher credit scores, often above 700, and substantial income documentation due to the larger loan amounts associated with high-value properties. Community Land Trust mortgages generally offer more flexible credit requirements and income considerations, aiming to increase affordability for buyers within income limits. Borrowers with strong credit profiles may favor jumbo loans for greater financing options, while those seeking affordability might benefit from the income-based qualifications of Community Land Trust mortgages.

Ownership Structure: Fee Simple vs. Ground Lease

Jumbo loans typically involve fee simple ownership, granting borrowers full property rights and the ability to sell or modify the asset without restrictions. In contrast, a community land trust mortgage features a ground lease structure, where homeowners own the structure but lease the land, preserving affordability and community control. This distinction impacts long-term equity, financing options, and transferability for high-value properties.

Pros and Cons: Jumbo Loan vs. Community Land Trust Mortgage

Jumbo loans offer financing for high-value properties exceeding conforming loan limits, providing competitive interest rates and flexible terms but often require stricter credit qualifications and larger down payments. Community Land Trust mortgages facilitate affordable homeownership by separating land ownership from the home, lowering initial costs and preserving long-term affordability, though they may limit property appreciation and resale options. Choosing between these options depends on factors like borrower creditworthiness, desired equity growth, and long-term financial goals.

Choosing the Best Mortgage Option for High-Value Properties

Jumbo loans offer higher loan limits for expensive properties but often require stringent credit scores and larger down payments compared to community land trust mortgages, which provide affordable homeownership by separating land ownership from the property. Community land trust mortgages reduce upfront costs and promote long-term affordability, ideal for buyers looking to maintain financial flexibility in high-value markets. Evaluating factors like interest rates, eligibility criteria, and long-term cost savings is essential when choosing between jumbo loans and community land trust mortgages for premium real estate investment.

Related Important Terms

High-Balance Jumbo Loans

High-Balance Jumbo Loans offer financing for high-value properties that exceed conforming loan limits, providing competitive interest rates and flexible underwriting criteria compared to standard jumbo loans. In contrast, Community Land Trust Mortgages focus on affordability and long-term housing stability by separating land ownership from property ownership, which may limit property appreciation potential but enhance community access.

Shared Equity Community Land Trust (CLT)

Shared Equity Community Land Trust (CLT) mortgages provide an affordable alternative to traditional Jumbo Loans for high-value properties by allowing buyers to share equity with the trust, reducing upfront costs and monthly payments. Unlike Jumbo Loans, CLTs promote long-term community ownership and stability by limiting resale prices, ensuring homes remain accessible to future buyers.

Jumbo Loan Portfolio Lending

Jumbo loan portfolio lending provides flexible underwriting criteria and faster approval for high-value properties exceeding conforming loan limits, enabling borrowers to secure financing without relying on government-sponsored entities. In contrast, community land trust mortgages focus on affordability and long-term community ownership, typically limiting loan amounts and restricting use for high-end real estate investments.

CLT Limited Equity Model

Jumbo loans typically require higher credit scores and larger down payments for high-value properties, whereas Community Land Trust (CLT) mortgages use a Limited Equity Model to keep homes affordable by restricting resale prices and maintaining long-term community ownership. The CLT structure ensures equity gains are shared, promoting housing stability in high-cost markets without the burden of traditional market-driven appreciation.

Jumbo Loan Risk-Based Pricing

Jumbo loans feature risk-based pricing reflecting the increased credit risk associated with high-value properties, often resulting in higher interest rates compared to conventional loans. Community Land Trust mortgages typically offer more stable, lower-cost financing by limiting property appreciation, thus reducing lender risk and making them an alternative for affordable access in high-value markets.

Ground Lease Structure (CLT)

Jumbo loans offer high-value property financing with conventional mortgage terms, while Community Land Trust (CLT) mortgages utilize a ground lease structure that separates land ownership from homeownership to promote affordable housing equity. The CLT ground lease reduces initial purchase costs and limits resale prices, creating long-term affordability compared to traditional jumbo loan financing.

Non-Conforming Loan Limits

Jumbo loans exceed conforming loan limits set by the Federal Housing Finance Agency, requiring higher credit scores, larger down payments, and often higher interest rates due to increased risk. Community Land Trust mortgages for high-value properties offer an alternative by separating land ownership from home ownership, potentially lowering upfront costs and making homeownership more accessible despite non-conforming loan limits.

Affordable Luxury Housing CLT

Jumbo loans finance high-value properties exceeding conforming loan limits, often requiring stringent credit criteria and higher down payments, while Community Land Trust (CLT) mortgages for Affordable Luxury Housing enable long-term homeownership through shared equity models, reducing initial costs and promoting community stability. CLT mortgages offer a sustainable, affordable alternative to traditional jumbo loans by capping resale prices and maintaining affordability for future buyers in upscale neighborhoods.

Interest-Only Jumbo Mortgage

Interest-only jumbo mortgages for high-value properties offer reduced initial payments by allowing borrowers to pay only the interest for a set period, often making them attractive compared to Community Land Trust mortgages, which typically involve shared equity and offer lower purchase prices but include ongoing land lease fees. Jumbo loans often have higher interest rates and stricter qualification criteria due to the loan size exceeding conforming limits, whereas Community Land Trust mortgages provide long-term affordability through communal ownership models but less equity buildup.

CLT Resale Price Restriction

Jumbo loans finance high-value properties without resale price restrictions, allowing market-driven appreciation, whereas Community Land Trust (CLT) mortgages impose resale price restrictions to maintain long-term affordability by limiting profit upon resale. These restrictions ensure CLT homes remain accessible to lower-income buyers, contrasting with the unlimited equity gains typical of jumbo loan properties.

Jumbo Loan vs Community Land Trust Mortgage for high-value properties. Infographic