An emergency fund goal is designed to provide a financial safety net for unexpected expenses or sudden income loss, ensuring stability during crises. In contrast, a sinking fund goal targets planned future expenses by saving gradually over time, preventing debt accumulation for known costs. Effective money management balances both goals to maintain financial security while preparing for anticipated expenditures.

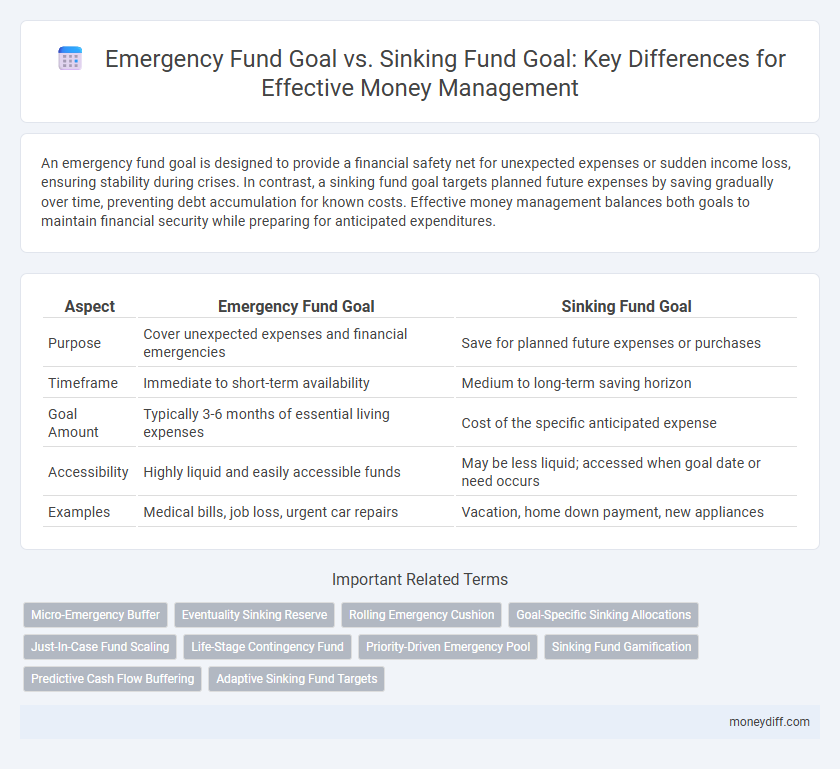

Table of Comparison

| Aspect | Emergency Fund Goal | Sinking Fund Goal |

|---|---|---|

| Purpose | Cover unexpected expenses and financial emergencies | Save for planned future expenses or purchases |

| Timeframe | Immediate to short-term availability | Medium to long-term saving horizon |

| Goal Amount | Typically 3-6 months of essential living expenses | Cost of the specific anticipated expense |

| Accessibility | Highly liquid and easily accessible funds | May be less liquid; accessed when goal date or need occurs |

| Examples | Medical bills, job loss, urgent car repairs | Vacation, home down payment, new appliances |

Understanding Emergency Fund Goals

An emergency fund goal focuses on setting aside three to six months' worth of essential living expenses to cover unexpected events like job loss or medical emergencies. This fund prioritizes liquidity and accessibility to provide immediate financial security without incurring debt. Unlike sinking funds, which allocate money for planned future expenses, emergency funds are strictly reserved for unforeseeable financial crises.

Defining Sinking Fund Goals

A sinking fund goal involves setting aside a specific amount of money over time for a planned future expense, such as car repairs or a vacation, ensuring funds are available without incurring debt. Unlike an emergency fund goal, which covers unexpected financial crises, sinking funds are allocated for predictable, non-urgent costs. Establishing sinking fund goals requires identifying the expense, estimating the total cost, and determining regular contributions to meet the target by the desired date.

Key Differences Between Emergency and Sinking Fund Goals

Emergency fund goals prioritize liquidity and accessibility, designed to cover unexpected expenses like job loss or medical emergencies, typically holding three to six months' worth of living expenses. Sinking fund goals, by contrast, focus on saving for anticipated future costs such as vacations, home repairs, or large purchases, usually set with specific time frames and amounts in mind. The key difference lies in the purpose and usage frequency: emergency funds address unforeseen crises, while sinking funds plan for predictable, non-recurring expenditures.

When to Prioritize an Emergency Fund

Prioritize an emergency fund when facing unpredictable financial risks such as job loss, medical expenses, or urgent home repairs, ensuring liquidity for immediate needs. An adequately funded emergency account typically covers three to six months of essential living expenses, providing a financial safety net. Only after securing this foundation should a sinking fund be targeted for planned expenses like vacations or large purchases.

Setting Sinking Fund Targets for Planned Expenses

Setting sinking fund targets for planned expenses involves allocating specific amounts periodically to cover future costs like car repairs, vacations, or home maintenance, ensuring financial readiness without disrupting cash flow. Unlike emergency funds designed for unexpected events, sinking funds are goal-oriented and help prevent debt by spreading out payments over time. Clear timelines and precise savings goals optimize money management and enhance budget stability.

How to Calculate Your Emergency Fund Needs

Calculate your emergency fund needs by assessing essential monthly expenses such as housing, utilities, groceries, transportation, and insurance for a minimum of three to six months. Use a detailed budget breakdown to determine fixed and variable costs, ensuring your emergency fund covers unexpected income loss or urgent expenses. Unlike sinking funds designed for planned purchases, emergency funds must prioritize liquidity and immediate access for financial security during unforeseen events.

Building Effective Sinking Fund Categories

Building effective sinking fund categories enhances financial preparedness by allocating specific amounts for anticipated expenses such as car maintenance, home repairs, and annual insurance premiums. Unlike an emergency fund, which targets unforeseen crises, sinking funds compartmentalize savings for planned costs, ensuring that large payments do not disrupt monthly budgets. This strategic categorization promotes disciplined money management and reduces reliance on credit during predictable financial obligations.

Benefits of Separate Emergency and Sinking Funds

Maintaining separate emergency and sinking funds enhances financial clarity by allocating resources specifically for unexpected expenses and planned future purchases, preventing the depletion of essential savings. This segregation reduces stress during emergencies since emergency funds remain untouched for non-urgent goals, while sinking funds accumulate gradually for large expenditures like vacations or home repairs. Clear categorization improves budgeting accuracy, enabling better tracking and disciplined saving habits tailored to distinct financial priorities.

Common Mistakes in Managing Funds

A common mistake in managing emergency and sinking funds is failing to clearly differentiate their purposes, leading to misuse of funds intended for unexpected expenses versus planned purchases. Overlapping these funds can result in inadequate savings during financial emergencies or insufficient resources for upcoming large expenses. Ensuring distinct fund allocation improves financial discipline and readiness for both sudden crises and scheduled financial goals.

Optimizing Your Money Management Strategy

Emergency fund goals prioritize liquidity and quick access to cover unexpected expenses, typically recommending three to six months of living expenses saved in a highly accessible account. Sinking fund goals involve setting aside money over time for planned future expenses like vacations or car repairs, enhancing budget predictability and preventing debt accumulation. Optimizing your money management strategy requires balancing both funds to ensure financial security while efficiently managing routine and unforeseen costs.

Related Important Terms

Micro-Emergency Buffer

A Micro-Emergency Buffer is a small, easily accessible emergency fund designed to cover unexpected expenses without disrupting financial stability, typically ranging from $500 to $1,000. Unlike sinking funds that are allocated for predictable, planned expenses, this buffer specifically targets urgent, unplanned financial shocks to prevent reliance on credit or high-interest debt.

Eventuality Sinking Reserve

An emergency fund goal focuses on covering unexpected expenses such as medical emergencies or job loss, while a sinking fund goal targets planned future expenses like vacations or major purchases, ensuring steady savings without financial strain. Prioritizing an eventuality sinking reserve allows for proactive money management by allocating funds systematically for predictable costs, enhancing overall financial stability.

Rolling Emergency Cushion

A Rolling Emergency Cushion serves as a flexible emergency fund goal designed to cover unexpected expenses over a continuous period, typically three to six months of essential living costs, ensuring liquidity without disruptive withdrawals. In contrast, a sinking fund goal targets specific, planned expenses by setting aside money over time, but it lacks the adaptive buffer that a rolling emergency cushion provides for unforeseen financial challenges.

Goal-Specific Sinking Allocations

Goal-specific sinking allocations focus on directing funds toward predefined sinking fund goals, ensuring disciplined savings for anticipated expenses such as car repairs or vacations. Unlike emergency funds designed for unforeseen financial crises, sinking funds target planned purchases or obligations, promoting strategic money management and financial stability.

Just-In-Case Fund Scaling

Emergency fund goals prioritize immediate access to three to six months' worth of essential expenses to cover unforeseen financial crises, ensuring liquidity and peace of mind. Sinking fund goals focus on planned, periodic savings for future specific purchases or expenses, allowing for cost distribution over time without disrupting cash flow.

Life-Stage Contingency Fund

Emergency fund goals prioritize maintaining three to six months of living expenses to cover unexpected life-stage events such as job loss or medical emergencies, providing immediate financial security. Sinking fund goals focus on saving predetermined amounts for planned life-stage expenses like home repairs or education, ensuring smooth financial management without disrupting the primary budget.

Priority-Driven Emergency Pool

Priority-Driven Emergency Pool focuses on creating a financial buffer specifically for unexpected expenses, distinguishing itself from a sinking fund that is earmarked for planned, periodic expenditures. This approach ensures that urgent, unforeseen costs are covered without disrupting budgeted funds allocated for anticipated goals, optimizing overall money management strategy.

Sinking Fund Gamification

Sinking fund goals enhance money management by breaking down large expenses into smaller, manageable savings targets, using gamification to boost motivation and track progress effectively. This approach contrasts with emergency funds, which prioritize immediate financial protection, as sinking funds encourage proactive, planned spending through engaging visual milestones and rewards.

Predictive Cash Flow Buffering

Emergency fund goals prioritize creating a predictive cash flow buffer to cover unexpected expenses, ensuring financial stability during unforeseen events. Sinking fund goals focus on systematically saving for anticipated future expenditures, enabling smooth cash flow management without disrupting overall budgeting.

Adaptive Sinking Fund Targets

Adaptive sinking fund targets enable precise allocation of funds for specific goals, adjusting contributions based on fluctuating expenses and timeframes. This approach contrasts with emergency fund goals, which focus on maintaining a fixed reserve for unexpected financial crises rather than planned, variable expenses.

Emergency fund goal vs Sinking fund goal for money management. Infographic