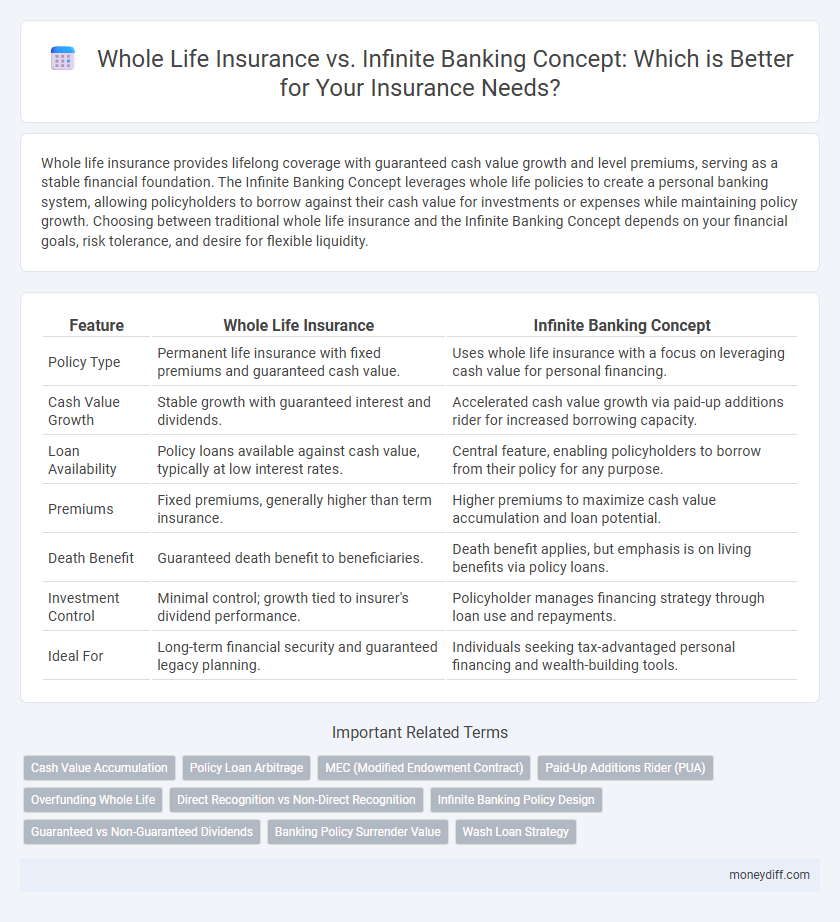

Whole life insurance provides lifelong coverage with guaranteed cash value growth and level premiums, serving as a stable financial foundation. The Infinite Banking Concept leverages whole life policies to create a personal banking system, allowing policyholders to borrow against their cash value for investments or expenses while maintaining policy growth. Choosing between traditional whole life insurance and the Infinite Banking Concept depends on your financial goals, risk tolerance, and desire for flexible liquidity.

Table of Comparison

| Feature | Whole Life Insurance | Infinite Banking Concept |

|---|---|---|

| Policy Type | Permanent life insurance with fixed premiums and guaranteed cash value. | Uses whole life insurance with a focus on leveraging cash value for personal financing. |

| Cash Value Growth | Stable growth with guaranteed interest and dividends. | Accelerated cash value growth via paid-up additions rider for increased borrowing capacity. |

| Loan Availability | Policy loans available against cash value, typically at low interest rates. | Central feature, enabling policyholders to borrow from their policy for any purpose. |

| Premiums | Fixed premiums, generally higher than term insurance. | Higher premiums to maximize cash value accumulation and loan potential. |

| Death Benefit | Guaranteed death benefit to beneficiaries. | Death benefit applies, but emphasis is on living benefits via policy loans. |

| Investment Control | Minimal control; growth tied to insurer's dividend performance. | Policyholder manages financing strategy through loan use and repayments. |

| Ideal For | Long-term financial security and guaranteed legacy planning. | Individuals seeking tax-advantaged personal financing and wealth-building tools. |

Understanding Whole Life Insurance: An Overview

Whole life insurance provides permanent coverage with fixed premiums and a guaranteed death benefit, accumulating cash value over time through a portion of paid premiums. The policy's cash value grows tax-deferred and can be accessed via loans or withdrawals, offering liquidity and financial flexibility. This stable growth and predictability differentiate whole life insurance from term policies and serve as the foundation for leveraging the infinite banking concept.

What Is the Infinite Banking Concept?

The Infinite Banking Concept leverages whole life insurance policies to create a personal banking system, allowing policyholders to borrow against their cash value for various financial needs while the policy continues to grow tax-deferred. This strategy maximizes the cash value accumulation within a whole life insurance policy by using dividends and interest, providing liquidity, control, and tax advantages that traditional banking cannot match. By integrating the principles of whole life insurance, Infinite Banking facilitates wealth building and financial independence through disciplined policy management.

Key Features of Whole Life Insurance Policies

Whole life insurance policies provide a fixed premium, guaranteed death benefit, and cash value accumulation at a guaranteed interest rate, ensuring lifelong coverage and financial stability. Policyholders can access the cash value through tax-advantaged loans or withdrawals, which supports liquidity and flexible financial planning within the infinite banking concept. This permanent insurance model contrasts with term life by offering both protection and wealth-building potential through stable, predictable policy performance.

How Infinite Banking Works with Life Insurance

Infinite banking leverages whole life insurance policies by allowing policyholders to build cash value that can be borrowed against tax-free, creating a personal financing system. The policy's cash value grows tax-deferred through dividends and interest, enabling continuous access to funds without loan approval from traditional banks. This strategy maximizes the policy's potential by turning the insurance contract into a wealth-building and liquidity-generating tool.

Cash Value Growth: Whole Life vs. Infinite Banking

Whole life insurance policies offer steady, guaranteed cash value growth based on fixed premiums and insurer dividends, providing policyholders with predictable accumulation over time. Infinite banking leverages whole life insurance's cash value by maximizing premium payments and policy loans, enabling accelerated cash value growth and liquidity through strategic financing opportunities. The key distinction lies in infinite banking's emphasis on using the policy's cash value as a personal banking system, optimizing growth and flexibility beyond traditional whole life cash value accumulation.

Policy Loans & Liquidity Comparison

Whole life insurance policies provide guaranteed cash value accumulation with the option to borrow through policy loans at low-interest rates, offering reliable liquidity without affecting credit scores. Infinite banking leverages whole life policies to create a personal banking system, allowing policyholders to access liquidity through tax-free policy loans while maintaining the growth of cash value. Comparing both, infinite banking emphasizes strategic use of policy loans to maximize funds' continuous growth and flexible liquidity management beyond traditional whole life benefits.

Costs and Fees: Breaking Down the Expenses

Whole life insurance policies typically involve fixed premiums with costs that cover mortality risk, administrative fees, and guaranteed cash value growth, often resulting in higher upfront expenses. Infinite banking concept leverages whole life insurance but emphasizes using the policy's cash value as a personal financing tool, which can incur additional loan interest charges and potential policy fees. Understanding the breakdown of these expenses is crucial for policyholders to weigh long-term costs against the financial benefits offered by both strategies.

Flexibility and Control: Evaluating Each Strategy

Whole life insurance offers guaranteed cash value growth and stable premiums, providing predictable financial planning with limited flexibility. The Infinite Banking Concept leverages whole life policies for tax-advantaged borrowing, granting more control over liquidity and asset use compared to traditional whole life strategies. Evaluating flexibility and control requires assessing individual financial goals, risk tolerance, and the desire for customizable cash flow management within each approach.

Tax Benefits of Whole Life and Infinite Banking

Whole life insurance offers tax-deferred cash value growth and tax-free death benefits, making it a powerful tool for long-term financial planning. The Infinite Banking Concept leverages whole life policies to create a tax-advantaged personal banking system, allowing policyholders to borrow against their cash value without triggering taxable events. Both strategies maximize tax efficiency by minimizing taxable income and providing tax-free access to funds.

Which Is Best for Your Financial Goals?

Whole life insurance offers guaranteed cash value growth and lifelong coverage, making it ideal for long-term financial security and estate planning. The infinite banking concept leverages whole life policies to create a personal banking system, providing liquidity and control over borrowed funds with potential tax advantages. Choose whole life for stable asset growth and protection, or infinite banking if maximizing policy cash flow for loans aligns with your strategic wealth-building goals.

Related Important Terms

Cash Value Accumulation

Whole life insurance provides guaranteed cash value accumulation through fixed premiums and a stable interest rate, ensuring predictable growth over time. The infinite banking concept leverages whole life policies to maximize cash value growth and liquidity, allowing policyholders to borrow against their accumulated cash value for tax-advantaged financing.

Policy Loan Arbitrage

Whole life insurance policies offer guaranteed cash value growth, enabling policyholders to leverage policy loans at low, fixed interest rates, which can be strategically used for loan arbitrage by investing borrowed funds in higher-yield opportunities. The Infinite Banking Concept capitalizes on this mechanism, turning whole life policy loans into a personal banking system that maximizes tax-advantaged growth and liquidity, optimizing long-term financial leverage and wealth accumulation.

MEC (Modified Endowment Contract)

Whole life insurance policies structured under the Infinite Banking Concept must be carefully managed to avoid becoming a Modified Endowment Contract (MEC), which triggers less favorable tax treatment on loans and withdrawals. Ensuring premium payments do not exceed IRS limits is essential to maintain the policy's tax advantages and preserve its utility as a funding vehicle in Infinite Banking strategies.

Paid-Up Additions Rider (PUA)

The Paid-Up Additions (PUA) rider significantly enhances whole life insurance policies by allowing policyholders to increase cash value and death benefits through additional premium payments, which aligns closely with the Infinite Banking Concept's strategy of building tax-advantaged, accessible cash value for personal financing. Incorporating PUAs accelerates policy growth, maximizing the efficiency of using whole life insurance as a self-bank, providing liquidity and financial flexibility unmatched by traditional term insurance products.

Overfunding Whole Life

Overfunding a whole life insurance policy enhances cash value growth, providing a powerful foundation for the Infinite Banking Concept by allowing policyholders to borrow against accumulated funds with tax advantages and flexible repayment terms. This strategy leverages the guaranteed dividends and stable returns of whole life insurance to create a self-sustaining personal banking system that can finance major expenses while maintaining lifelong coverage.

Direct Recognition vs Non-Direct Recognition

Direct recognition dividend options in infinite banking policies adjust loan interest rates based on outstanding policy loans, optimizing cash value growth and loan management, whereas whole life policies with non-direct recognition maintain uniform dividend rates regardless of loans, potentially diluting cash value accumulation during loan usage. Understanding the impact of direct versus non-direct recognition on loan interest and dividend credits is crucial for policyholders aiming to maximize the financial efficiency of whole life insurance in infinite banking strategies.

Infinite Banking Policy Design

Infinite Banking Policy Design leverages whole life insurance's cash value growth and tax advantages to create a personalized banking system, enabling policyholders to borrow against their accumulated cash value at favorable rates. This strategy prioritizes efficient premium structuring, consistent dividend payments, and maximizing cash value accumulation to optimize liquidity, control, and long-term financial growth.

Guaranteed vs Non-Guaranteed Dividends

Whole life insurance policies typically offer guaranteed dividends based on the insurer's financial performance, providing policyholders with predictable growth and stability. In contrast, infinite banking concept strategies often rely on non-guaranteed dividends, which can fluctuate annually and impact the policy's cash value accumulation and loan repayment potential.

Banking Policy Surrender Value

Whole life insurance policies build cash value over time with guaranteed growth and dividends, offering stable surrender values that can be accessed without taxes, which supports the infinite banking concept by enabling policyholders to borrow against their accumulated value. Infinite banking leverages these surrender values strategically, allowing individuals to create personal banking systems through policy loan mechanics while maintaining coverage and cash value growth.

Wash Loan Strategy

The Wash Loan Strategy leverages whole life insurance policies by using policy loans to access cash value without triggering taxable events, effectively optimizing liquidity and tax advantages compared to traditional infinite banking methods. Whole life insurance's guaranteed cash value growth and fixed premiums create a stable foundation for executing wash loans, enhancing financial flexibility and wealth accumulation within the insurance framework.

Whole life vs Infinite banking concept for insurance. Infographic