Term insurance offers affordable life coverage for a specified period with no cash value, providing a death benefit only if the insured passes away during the term. Return of premium insurance combines term coverage with a refund feature, returning premiums paid if the policyholder outlives the term, typically resulting in higher costs. Choosing between these depends on balancing budget constraints and the desire for potential premium recovery.

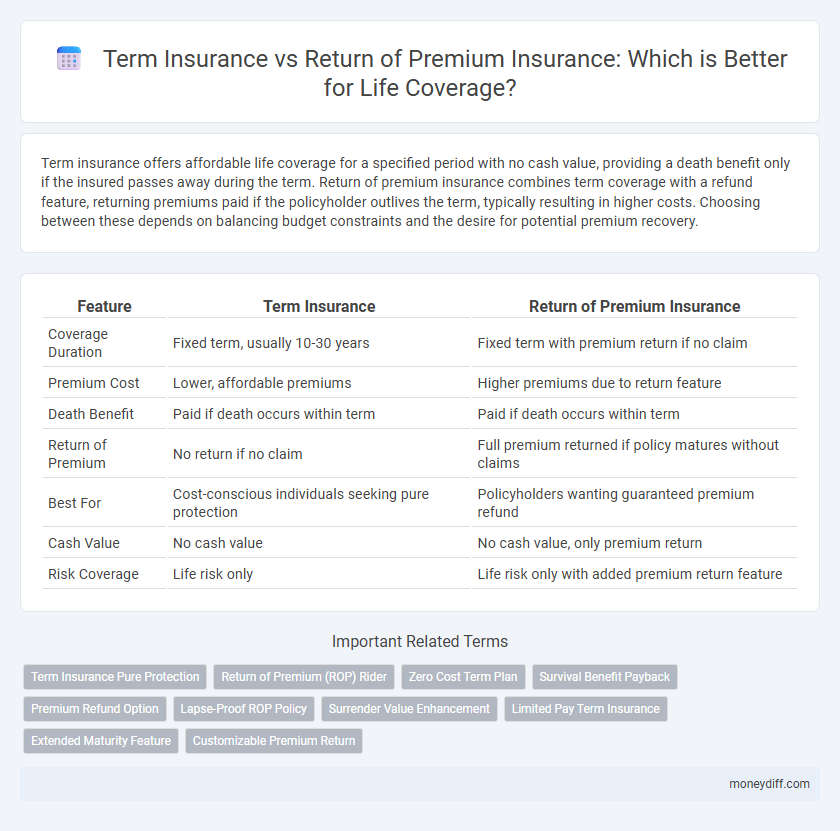

Table of Comparison

| Feature | Term Insurance | Return of Premium Insurance |

|---|---|---|

| Coverage Duration | Fixed term, usually 10-30 years | Fixed term with premium return if no claim |

| Premium Cost | Lower, affordable premiums | Higher premiums due to return feature |

| Death Benefit | Paid if death occurs within term | Paid if death occurs within term |

| Return of Premium | No return if no claim | Full premium returned if policy matures without claims |

| Best For | Cost-conscious individuals seeking pure protection | Policyholders wanting guaranteed premium refund |

| Cash Value | No cash value | No cash value, only premium return |

| Risk Coverage | Life risk only | Life risk only with added premium return feature |

Understanding Term Insurance: Key Features

Term insurance offers life coverage for a specified period, providing a death benefit only if the insured passes away during the term. Premiums are generally lower compared to permanent policies, making it a cost-effective solution for temporary financial protection. It does not build cash value, emphasizing pure risk coverage without savings or investment components.

What is Return of Premium (ROP) Insurance?

Return of Premium (ROP) insurance is a type of term life insurance policy that refunds the total premiums paid if the insured survives the policy term. Unlike traditional term insurance, which provides coverage without any payout if no claim is made, ROP insurance acts as a forced savings plan, combining life coverage with a refund feature. This option often comes with higher premiums, appealing to policyholders seeking financial return alongside life protection.

Cost Comparison: Term Insurance vs ROP

Term insurance typically offers lower initial premiums compared to Return of Premium (ROP) insurance, making it more affordable for budget-conscious individuals seeking pure life coverage. ROP insurance premiums are higher because they include a savings component that returns the total paid premiums if the insured outlives the policy term. Over the long term, ROP policies tend to cost 20-30% more than term insurance, but they provide the benefit of premium recovery, reducing the effective cost of coverage for those who value this feature.

Policy Duration and Flexibility

Term insurance offers fixed policy durations, typically ranging from 10 to 30 years, providing straightforward coverage with lower premiums but limited flexibility in extending coverage beyond the term. Return of premium (ROP) insurance also spans similar durations but includes the benefit of returning paid premiums if the insured outlives the policy, often at higher cost and with less adaptability for mid-term adjustments. Policyholders seeking customizable coverage periods and potential premium recovery must weigh the trade-offs between the fixed, budget-friendly nature of term insurance and the premium reimbursement feature of ROP plans.

Payout Structure Explained

Term insurance offers a death benefit payout only if the insured passes away within the policy term, providing pure protection with no maturity value. Return of premium insurance refunds all paid premiums to the policyholder if they survive the term, combining coverage with a savings component. This payout structure affects premium costs, with return of premium plans generally having higher premiums due to the guaranteed return feature.

Tax Benefits of Each Option

Term insurance premiums are generally lower and offer tax deductions under Section 80C of the Income Tax Act, with the death benefit being tax-free under Section 10(10D). Return of premium (ROP) insurance policies provide the advantage of receiving the total premiums paid if the insured survives the policy term, with the maturity amount typically exempt from tax under Section 10(10D), though the premiums are higher compared to term plans. Both options deliver significant tax savings, but term insurance maximizes immediate tax deductions while ROP policies combine tax benefits with the potential return of paid premiums.

Pros and Cons of Term Insurance

Term insurance offers affordable life coverage for a specified period, providing a high sum assured at lower premiums compared to permanent policies. Its main drawback is the lack of maturity benefits, meaning if the insured outlives the term, no money is returned. This type of policy suits individuals seeking budget-friendly protection without the need for cash value accumulation.

Pros and Cons of Return of Premium Insurance

Return of premium (ROP) insurance refunds the total premiums paid if the insured outlives the policy term, providing a savings-like benefit alongside life coverage. Its main advantage is the potential to recover costs, making it appealing for those seeking both protection and a financial return, but it typically comes with higher premiums than traditional term insurance. The drawback lies in the increased expense without investment growth, and if the policyholder dies early, the beneficiaries receive only the death benefit, not the premiums paid.

Which Insurance Suits Your Financial Goals?

Term insurance offers affordable life coverage for a specific period, ideal for individuals seeking cost-effective protection without investment returns. Return of premium insurance provides the benefit of refunding premiums if no claim is made, suited for those prioritizing risk-averse savings alongside life coverage. Choosing between these plans depends on financial goals--whether affordability or guaranteed premium recovery aligns better with your long-term financial strategy.

Choosing the Right Life Coverage for You

Term insurance offers affordable life coverage for a specified period, providing financial protection only if the insured passes away during the term. Return of premium insurance combines life coverage with a savings component, refunding all paid premiums if the insured outlives the policy term, resulting in higher overall costs. Selecting the right policy depends on your budget, financial goals, and preference for risk versus potential premium recovery.

Related Important Terms

Term Insurance Pure Protection

Term insurance provides pure protection by offering a death benefit only if the insured passes away within the policy term, making it a cost-effective choice for temporary life coverage. Unlike Return of Premium insurance, term insurance does not refund premiums if the policyholder survives the term, resulting in lower initial premiums and straightforward coverage focused solely on risk protection.

Return of Premium (ROP) Rider

Return of Premium (ROP) Rider on term insurance policies offers a unique feature where policyholders receive a full refund of premiums paid if they outlive the policy term, enhancing traditional term coverage by providing savings alongside life protection. This rider increases the overall cost but appeals to risk-averse individuals seeking guaranteed returns without sacrificing the lower premiums characteristic of term insurance.

Zero Cost Term Plan

Zero Cost Term Plan offers life coverage with the advantage of a pure term insurance policy where the entire premium paid is returned at policy maturity, effectively eliminating the cost of insurance. Unlike traditional term insurance that provides protection without any payout if the insured survives the term, the Return of Premium option ensures financial security by reimbursing premiums, making it a cost-efficient choice for long-term life coverage.

Survival Benefit Payback

Term insurance provides life coverage for a specified period without any survival benefit payout, whereas Return of Premium (ROP) insurance refunds the total premiums paid if the insured survives the policy term, offering a financial payback. The ROP feature enhances policy value by combining death protection with a survival benefit, making it a preferred choice for policyholders seeking both coverage and premium recovery.

Premium Refund Option

Term insurance offers affordable life coverage for a specified period without any payout if the insured survives, whereas Return of Premium (ROP) insurance refunds the total premiums paid if no claim is made, effectively acting as a forced savings plan. The premium refund option in ROP policies increases the upfront cost but provides financial security by returning the accumulated premiums, contrasting with standard term policies that forgo any refund upon policy expiry.

Lapse-Proof ROP Policy

Return of premium (ROP) insurance ensures policyholders receive all paid premiums back if no claim is made, offering a lapse-proof financial safety net unlike traditional term insurance, which forfeits premiums upon policy lapse. This ROP feature eliminates the risk of losing investment value, providing both life coverage and guaranteed premium refunds, appealing to risk-averse individuals seeking secure, long-term financial planning.

Surrender Value Enhancement

Term insurance offers pure life coverage with no surrender value, making it cost-effective but non-refundable, while Return of Premium (ROP) insurance combines life coverage with a surrender value by refunding premiums paid if the policyholder outlives the term, enhancing financial benefits. ROP policies typically have higher premiums but provide a cash value component that improves surrender value enhancement compared to standard term insurance.

Limited Pay Term Insurance

Limited Pay Term Insurance provides life coverage for a specified term with premiums payable only for a limited period, offering cost savings compared to lifelong payment plans; unlike Return of Premium (ROP) insurance, it does not refund premiums if the insured outlives the policy term. Term insurance delivers pure protection without cash value buildup, whereas ROP policies combine protection with a premium refund feature, resulting in higher overall costs but added financial return benefits.

Extended Maturity Feature

Term insurance offers affordable life coverage for a specified period, while Return of Premium (ROP) insurance refunds the premiums if the insured outlives the policy term, providing added value. The Extended Maturity Feature in ROP policies allows coverage to continue beyond the original term without additional premiums until a set age, enhancing financial protection compared to standard term insurance.

Customizable Premium Return

Term insurance offers affordable life coverage with fixed premiums, while Return of Premium (ROP) insurance provides the added benefit of customizable premium return options, allowing policyholders to recover paid premiums if no claim is made by the policy term's end. Customizable premium return features in ROP policies enable tailored refund schedules and amounts, enhancing financial flexibility and increasing long-term value compared to standard term insurance.

Term insurance vs Return of premium insurance for life coverage. Infographic