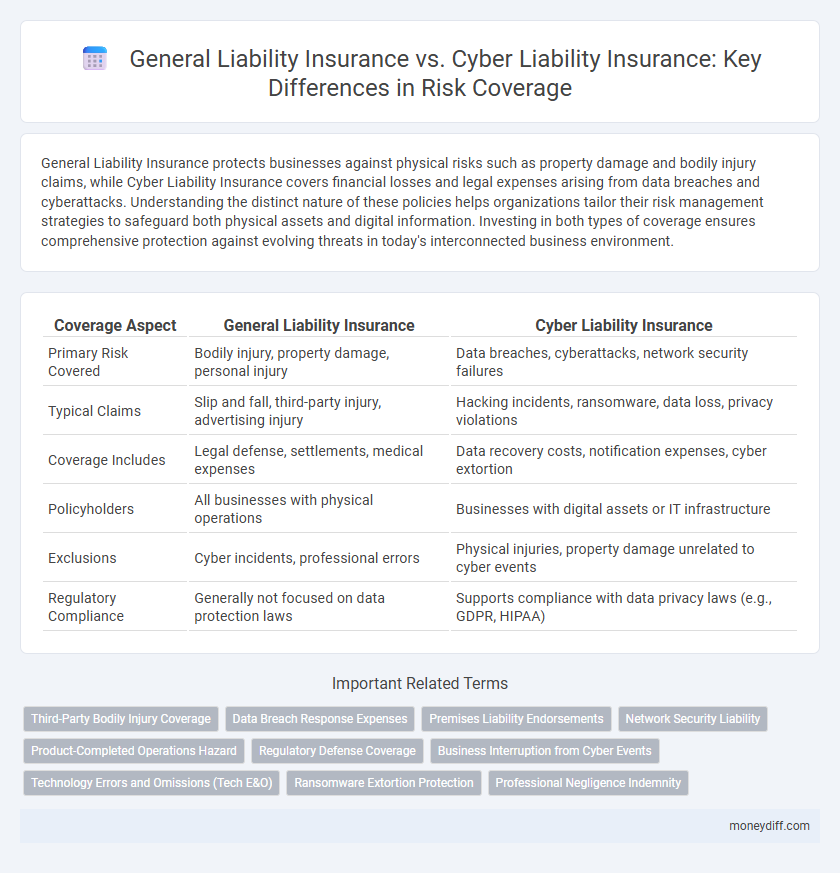

General Liability Insurance protects businesses against physical risks such as property damage and bodily injury claims, while Cyber Liability Insurance covers financial losses and legal expenses arising from data breaches and cyberattacks. Understanding the distinct nature of these policies helps organizations tailor their risk management strategies to safeguard both physical assets and digital information. Investing in both types of coverage ensures comprehensive protection against evolving threats in today's interconnected business environment.

Table of Comparison

| Coverage Aspect | General Liability Insurance | Cyber Liability Insurance |

|---|---|---|

| Primary Risk Covered | Bodily injury, property damage, personal injury | Data breaches, cyberattacks, network security failures |

| Typical Claims | Slip and fall, third-party injury, advertising injury | Hacking incidents, ransomware, data loss, privacy violations |

| Coverage Includes | Legal defense, settlements, medical expenses | Data recovery costs, notification expenses, cyber extortion |

| Policyholders | All businesses with physical operations | Businesses with digital assets or IT infrastructure |

| Exclusions | Cyber incidents, professional errors | Physical injuries, property damage unrelated to cyber events |

| Regulatory Compliance | Generally not focused on data protection laws | Supports compliance with data privacy laws (e.g., GDPR, HIPAA) |

Understanding General Liability Insurance

General Liability Insurance protects businesses from third-party claims involving bodily injury, property damage, and personal injury occurring on business premises or caused by business operations. It covers legal defense costs and settlements, providing crucial financial protection against common risks like slip-and-fall accidents and advertising injury. This insurance is essential for brick-and-mortar businesses seeking to safeguard physical assets and customer interactions.

What Is Cyber Liability Insurance?

Cyber Liability Insurance protects businesses from financial losses resulting from data breaches, cyber-attacks, and other technology-related risks. It covers expenses such as legal fees, notification costs, and regulatory fines associated with compromised sensitive information. This insurance is essential for managing the growing threats in the digital landscape, distinct from General Liability Insurance, which typically covers physical injury and property damage.

Key Differences Between General and Cyber Liability

General Liability Insurance primarily covers physical risks such as bodily injury, property damage, and personal injury claims arising from business operations or premises. Cyber Liability Insurance focuses on digital risks including data breaches, cyberattacks, and privacy violations that compromise sensitive information or disrupt business technology systems. Key differences lie in coverage scope: General Liability addresses tangible incidents while Cyber Liability protects against intangible cyber threats and regulatory penalties related to data security.

Coverage Scope: General Liability vs Cyber Liability

General Liability Insurance primarily covers physical damages, bodily injury, property damage, and personal injury claims arising from business operations, while Cyber Liability Insurance focuses on risks related to data breaches, cyberattacks, and electronic data loss. General Liability does not extend to digital threats or cyber incidents, leaving businesses exposed to the financial impact of hacking, malware, and privacy violations without Cyber Liability coverage. Cyber Liability Insurance addresses expenses such as data recovery, legal fees, notification costs, and crisis management following cyber incidents, complementing the traditional protections offered by General Liability Insurance.

Common Claims Covered by General Liability Insurance

General Liability Insurance commonly covers claims related to bodily injury, property damage, and personal injury such as libel or slander occurring on business premises. It also protects against product liability claims and advertising injuries that could lead to financial loss. Cyber Liability Insurance, in contrast, addresses data breaches, cyberattacks, and network security failures, making it essential for digital risk management.

Common Claims Covered by Cyber Liability Insurance

Cyber Liability Insurance primarily covers claims related to data breaches, including unauthorized access to sensitive customer information, and the costs of notifying affected parties. It also addresses expenses from cyber extortion, such as ransomware attacks, and legal fees arising from privacy violations or regulatory fines. Common claims often involve network security failures, data loss, and business interruption due to cyber incidents.

Cost Comparison: General Liability vs Cyber Liability

General Liability Insurance typically costs between $400 and $1,000 annually for small businesses, providing coverage for bodily injury, property damage, and legal defense. Cyber Liability Insurance premiums range from $500 to $3,000 per year, depending on the extent of coverage for data breaches, cyber extortion, and business interruption. The higher cost of cyber liability reflects the growing risks associated with digital threats and the complexity of mitigating cyber risks compared to traditional general liability exposures.

Risk Assessment: Choosing the Right Policy

General Liability Insurance primarily covers physical damages and bodily injuries arising from business operations, while Cyber Liability Insurance addresses risks related to data breaches, cyberattacks, and technology failures. A thorough risk assessment should evaluate potential exposures such as property damage versus digital asset vulnerabilities, emphasizing the significance of protecting confidential data, intellectual property, and customer information. Selecting the right policy depends on identifying whether traditional operational risks or emerging cyber threats pose a greater threat to the business's financial stability and reputation.

Industries That Benefit from Each Insurance Type

General Liability Insurance is essential for industries like construction, retail, and hospitality where physical injuries, property damage, and third-party claims are common risks. Cyber Liability Insurance is crucial for technology firms, financial institutions, and e-commerce businesses that face threats such as data breaches, cyberattacks, and privacy violations. Understanding the specific risk exposures in sectors like manufacturing or healthcare guides companies to select the appropriate coverage for comprehensive protection.

How to Integrate Both Insurances for Optimal Protection

Combining General Liability Insurance with Cyber Liability Insurance ensures comprehensive risk management by covering physical damages and data breaches, respectively. Businesses should assess their specific exposures and coordinate with insurers to tailor policies that avoid coverage gaps and overlaps. Implementing an integrated insurance strategy enhances financial resilience against both traditional liabilities and evolving cyber threats.

Related Important Terms

Third-Party Bodily Injury Coverage

General Liability Insurance provides essential third-party bodily injury coverage for physical accidents occurring on business premises or due to business operations, protecting against medical expenses and legal claims. Cyber Liability Insurance, however, primarily addresses data breaches and cyberattacks, offering limited or no coverage for physical injuries to third parties.

Data Breach Response Expenses

General Liability Insurance typically excludes coverage for Data Breach Response Expenses, leaving businesses financially vulnerable to costs associated with notifying affected parties, legal fees, and credit monitoring services. Cyber Liability Insurance specifically addresses these risks by covering expenses related to managing and mitigating the impact of data breaches, including regulatory fines and forensic investigations.

Premises Liability Endorsements

General Liability Insurance with Premises Liability Endorsements covers bodily injury and property damage occurring on business premises, protecting against slip-and-fall accidents and other on-site hazards. Cyber Liability Insurance, in contrast, addresses data breaches and cyberattacks, offering coverage for cyber extortion, data restoration, and privacy liability unrelated to physical premises risks.

Network Security Liability

General Liability Insurance covers bodily injury and property damage but excludes Network Security Liability risks such as data breaches and cyberattacks. Cyber Liability Insurance specifically addresses Network Security Liability by protecting businesses against costs related to data loss, cyber extortion, and network intrusions.

Product-Completed Operations Hazard

General Liability Insurance covers Product-Completed Operations Hazard by protecting businesses against claims of bodily injury or property damage resulting from products or completed work, whereas Cyber Liability Insurance specifically addresses risks related to data breaches, cyberattacks, and electronic information loss. For manufacturers or contractors, General Liability policies provide essential coverage for physical damages linked to finished goods or services, while Cyber Liability is critical for safeguarding digital assets and sensitive customer information from evolving cyber threats.

Regulatory Defense Coverage

General Liability Insurance primarily covers bodily injury and property damage claims but typically excludes coverage for data breaches and cyber incidents, making it insufficient for regulatory defense costs related to cybersecurity violations. Cyber Liability Insurance specifically addresses regulatory defense coverage by protecting businesses against fines, penalties, and legal expenses arising from data breaches and non-compliance with data protection laws like GDPR and CCPA.

Business Interruption from Cyber Events

General Liability Insurance covers traditional risks like bodily injury and property damage but typically excludes losses from business interruption caused by cyber events. Cyber Liability Insurance specifically addresses financial losses due to cyberattacks, including data breaches and ransomware, offering critical protection for business interruption risks stemming from these digital threats.

Technology Errors and Omissions (Tech E&O)

General Liability Insurance covers physical damages and bodily injuries but does not protect against technology-related risks, whereas Cyber Liability Insurance specifically addresses data breaches and cyberattacks impacting digital assets. Technology Errors and Omissions (Tech E&O) insurance bridges this gap by covering professional mistakes, software failures, and technology service errors that neither general liability nor standard cyber policies fully encompass.

Ransomware Extortion Protection

General Liability Insurance primarily covers bodily injury and property damage claims but typically excludes cyber incidents like ransomware extortion, leaving businesses vulnerable to significant financial losses. Cyber Liability Insurance specifically addresses risks such as ransomware attacks, providing critical coverage for data recovery, extortion payments, and associated legal expenses.

Professional Negligence Indemnity

General Liability Insurance covers claims related to bodily injury, property damage, and advertising mistakes but typically excludes professional negligence indemnity, which is specifically addressed by Cyber Liability Insurance. Cyber Liability Insurance provides protection against risks such as data breaches, cyberattacks, and professional errors in managing digital information, ensuring coverage for financial losses stemming from cyber incidents and professional negligence in IT services.

General Liability Insurance vs Cyber Liability Insurance for risk coverage. Infographic