Home insurance provides standard coverage with fixed premiums based on property value, location, and risk factors, offering predictable protection for homeowners. Usage-based home insurance adjusts premiums dynamically by monitoring real-time data such as occupancy patterns and security system usage, potentially lowering costs for low-risk properties. This personalized approach enhances property protection by aligning coverage with actual home usage and behavioral risks.

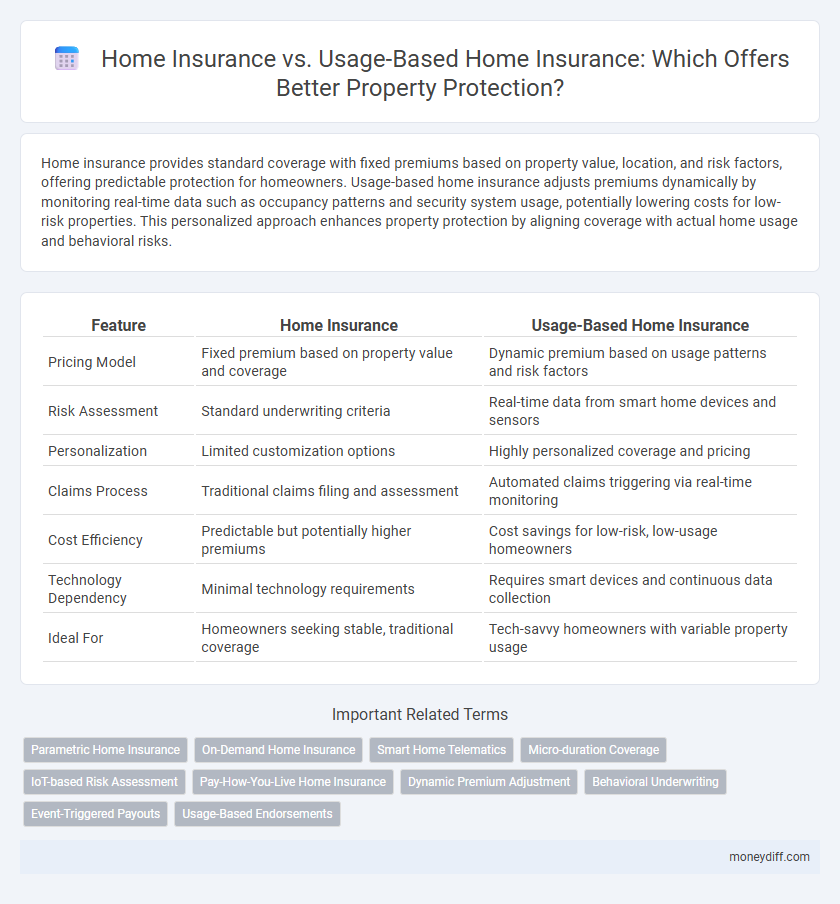

Table of Comparison

| Feature | Home Insurance | Usage-Based Home Insurance |

|---|---|---|

| Pricing Model | Fixed premium based on property value and coverage | Dynamic premium based on usage patterns and risk factors |

| Risk Assessment | Standard underwriting criteria | Real-time data from smart home devices and sensors |

| Personalization | Limited customization options | Highly personalized coverage and pricing |

| Claims Process | Traditional claims filing and assessment | Automated claims triggering via real-time monitoring |

| Cost Efficiency | Predictable but potentially higher premiums | Cost savings for low-risk, low-usage homeowners |

| Technology Dependency | Minimal technology requirements | Requires smart devices and continuous data collection |

| Ideal For | Homeowners seeking stable, traditional coverage | Tech-savvy homeowners with variable property usage |

Understanding Traditional Home Insurance

Traditional home insurance provides comprehensive coverage for property damage, theft, and liability based on a fixed premium determined by factors such as location, home value, and coverage limits. Policyholders benefit from predictable costs and broad protection without the need for monitoring specific behaviors or usage patterns. This type of insurance remains a reliable choice for securing homes against common risks with established underwriting criteria and claims processes.

What is Usage-Based Home Insurance?

Usage-based home insurance leverages data from smart home devices and sensors to monitor property conditions and adjust premiums based on actual risk factors. This approach enables personalized coverage by analyzing real-time information on factors like fire hazards, water leaks, and security system activity. Traditional home insurance relies on static assessments, whereas usage-based policies dynamically adapt to your lifestyle and property usage for optimized protection.

Key Differences between Home Insurance and Usage-Based Policies

Home insurance typically offers fixed premiums based on property characteristics and risk factors, while usage-based home insurance adjusts premiums dynamically according to homeowner behavior and real-time data, such as occupancy patterns and security system usage. Traditional policies emphasize coverage limits and standardized risk assessments, whereas usage-based policies leverage smart home technology to provide more personalized pricing and enhanced loss prevention. Key differences include premium calculation methods, reliance on telematics or IoT devices, and potential cost savings aligned with proactive property protection measures.

Coverage Options: Standard vs. Usage-Based Home Insurance

Standard home insurance offers fixed coverage options that protect against common risks like fire, theft, and natural disasters, with premiums based on property value and location. Usage-based home insurance adjusts coverage and premiums dynamically by monitoring homeowner behavior, security system usage, and maintenance frequency through smart home devices. This approach provides personalized protection and potential cost savings by aligning coverage with actual risk factors specific to the property and its usage patterns.

Premium Calculation: Fixed Rates vs. Usage-Based Models

Home insurance typically features fixed-rate premiums determined by property value, location, and risk factors, offering predictable costs for homeowners. Usage-based home insurance calculates premiums dynamically based on real-time data such as occupancy patterns, energy consumption, and security system usage, providing personalized pricing. This model incentivizes safer property behaviors and can result in lower premiums for low-risk homeowners.

Customization and Flexibility in Coverage

Usage-based home insurance offers enhanced customization by allowing policyholders to adjust coverage based on real-time data, such as property usage patterns and risk factors, leading to more accurate premium pricing. Traditional home insurance provides fixed coverage options that may not reflect the specific needs or behaviors of the homeowner, often resulting in overpayment for unnecessary protection. This flexibility in usage-based policies ensures tailored risk management, optimizing property protection and financial efficiency.

Cost-Effectiveness: Which Option Saves More?

Usage-based home insurance often proves more cost-effective by tailoring premiums to actual usage patterns and risk levels, reducing unnecessary costs compared to traditional home insurance's flat-rate pricing. Traditional home insurance can be more expensive due to standardized rates that do not consider the homeowner's specific behaviors or security measures. Homeowners seeking savings should evaluate their property usage and risk exposure to determine if the dynamic pricing model of usage-based insurance aligns better with their cost-saving goals.

Suitability: Who Should Choose Usage-Based Home Insurance?

Usage-based home insurance suits homeowners who prefer personalized premiums reflecting their actual property usage and risk behaviors. Ideal candidates include individuals with energy-efficient homes, frequent property monitoring, or those seeking to reduce costs through data-driven discounts. This model is particularly beneficial for tech-savvy users comfortable with sharing real-time occupancy and maintenance data for optimized coverage.

Claims Process: Traditional vs. Usage-Based Approach

Home insurance claims process typically involves fixed premiums and manual reporting, often leading to longer settlement times due to detailed assessments. Usage-based home insurance employs smart home devices and real-time data, enabling faster claim verification and personalized risk evaluation. The data-driven approach reduces fraud, accelerates payouts, and improves overall customer satisfaction in property protection.

Future Trends in Home Insurance and Usage-Based Models

Future trends in home insurance emphasize integration of smart home technology and real-time data analytics to enhance personalized coverage and risk assessment. Usage-based home insurance models leverage IoT devices and sensor data to adjust premiums dynamically, reflecting actual property usage and behavior patterns. This shift toward data-driven underwriting promises increased efficiency, cost savings, and tailored protection in the evolving home insurance landscape.

Related Important Terms

Parametric Home Insurance

Parametric home insurance provides simplified protection by paying predetermined amounts when specific triggers, such as earthquake magnitude or flood levels, occur, contrasting traditional home insurance that relies on itemized loss assessments and claims processing. Usage-based home insurance leverages data from smart home devices to customize premiums and coverage, optimizing risk management and potentially lowering costs compared to standard fixed-rate policies.

On-Demand Home Insurance

On-Demand Home Insurance offers flexible, pay-as-you-go coverage tailored to specific timeframes or events, providing property protection when traditional Home Insurance policies may be overly broad or costly. Usage-based models leverage real-time data and user behavior to optimize premiums, ensuring homeowners only pay for coverage aligned with their actual needs and risk exposure.

Smart Home Telematics

Smart Home Telematics enhances traditional home insurance by providing real-time data on property conditions, enabling usage-based home insurance policies that offer personalized premiums and proactive risk management. This technology leverages sensors and IoT devices to monitor security, fire hazards, and environmental factors, improving claim accuracy and reducing potential damages through early detection.

Micro-duration Coverage

Micro-duration coverage in usage-based home insurance offers tailored protection for short, specific timeframes, ideal for renters or temporary stays, contrasting traditional home insurance which typically requires annual commitments; this innovative approach leverages real-time data to adjust premiums and coverage dynamically, enhancing flexibility and cost-efficiency in property protection.

IoT-based Risk Assessment

IoT-based risk assessment in usage-based home insurance leverages connected devices such as smart sensors and security systems to monitor real-time hazards, enabling more accurate premium pricing and proactive loss prevention compared to traditional home insurance that relies on static risk factors. This dynamic approach enhances property protection by continuously analyzing data on environmental conditions and homeowner behavior, reducing claims frequency and severity through early detection of potential risks.

Pay-How-You-Live Home Insurance

Pay-How-You-Live home insurance offers personalized property protection by adjusting premiums based on real-time lifestyle data, unlike traditional home insurance which relies on static risk factors and property evaluations. This usage-based model enhances cost efficiency and coverage accuracy by incorporating factors such as occupancy patterns, home automation usage, and security system activity.

Dynamic Premium Adjustment

Home insurance offers fixed premiums based on property value and risk assessments, while usage-based home insurance dynamically adjusts premiums according to real-time data such as occupancy patterns, security system usage, and environmental factors. Dynamic premium adjustment in usage-based policies enhances cost-efficiency and personalized coverage by reflecting actual property usage and risk levels.

Behavioral Underwriting

Home insurance relies on traditional risk factors like property location and structure, whereas usage-based home insurance incorporates Behavioral Underwriting by analyzing real-time data such as household occupancy patterns and daily activities to tailor premiums more accurately. This approach enables insurers to offer personalized coverage and discounts based on actual property use, enhancing risk assessment and potentially lowering costs for responsible homeowners.

Event-Triggered Payouts

Home insurance provides fixed coverage based on policy terms, while usage-based home insurance offers event-triggered payouts that activate immediately after specific incidents such as water leaks or fire alarms, ensuring faster claims processing and tailored protection. This model leverages IoT sensors and real-time data to minimize damage and reduce claim disputes by automatically assessing event severity.

Usage-Based Endorsements

Usage-based endorsements in home insurance offer personalized premiums by analyzing real-time data on property usage and risk factors, enhancing cost efficiency and tailored coverage. This dynamic approach contrasts traditional fixed-rate home insurance by adapting to homeowners' actual behavior, reducing unnecessary expenses while maintaining comprehensive property protection.

Home insurance vs Usage-based home insurance for property protection. Infographic