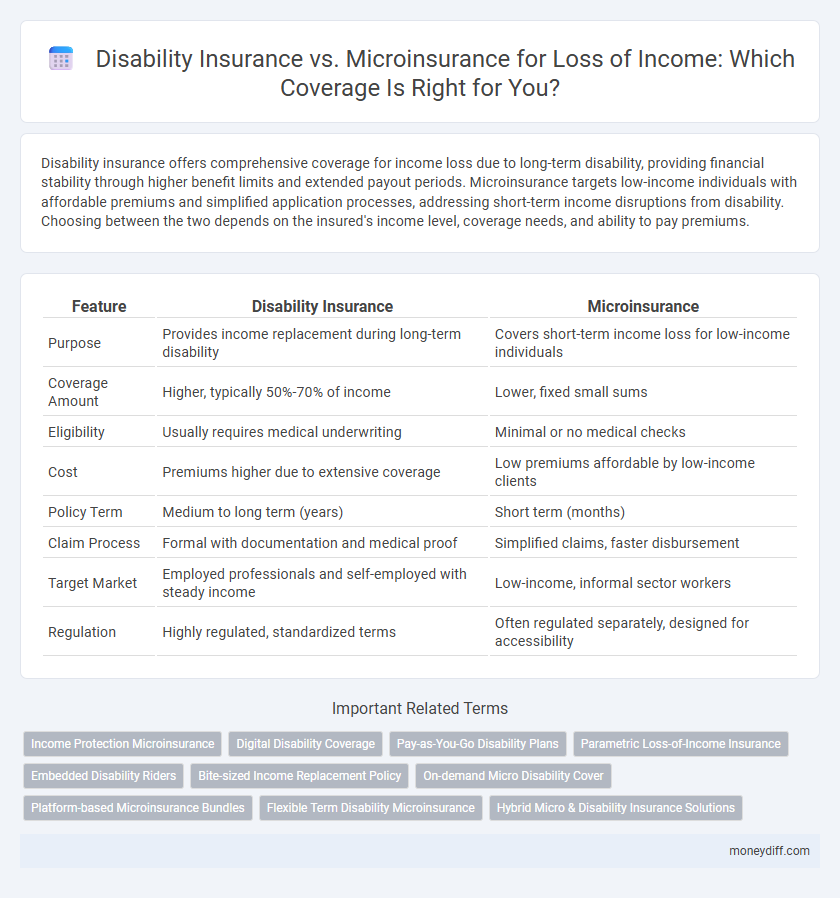

Disability insurance offers comprehensive coverage for income loss due to long-term disability, providing financial stability through higher benefit limits and extended payout periods. Microinsurance targets low-income individuals with affordable premiums and simplified application processes, addressing short-term income disruptions from disability. Choosing between the two depends on the insured's income level, coverage needs, and ability to pay premiums.

Table of Comparison

| Feature | Disability Insurance | Microinsurance |

|---|---|---|

| Purpose | Provides income replacement during long-term disability | Covers short-term income loss for low-income individuals |

| Coverage Amount | Higher, typically 50%-70% of income | Lower, fixed small sums |

| Eligibility | Usually requires medical underwriting | Minimal or no medical checks |

| Cost | Premiums higher due to extensive coverage | Low premiums affordable by low-income clients |

| Policy Term | Medium to long term (years) | Short term (months) |

| Claim Process | Formal with documentation and medical proof | Simplified claims, faster disbursement |

| Target Market | Employed professionals and self-employed with steady income | Low-income, informal sector workers |

| Regulation | Highly regulated, standardized terms | Often regulated separately, designed for accessibility |

Understanding Disability Insurance and Microinsurance

Disability insurance provides comprehensive financial protection by replacing a portion of lost income due to long-term or permanent disabilities, typically offered through employers or private insurers with higher coverage limits and premiums. Microinsurance targets low-income individuals, offering affordable, limited coverage for short-term income loss caused by disability, often facilitated through community organizations or microfinance institutions. Understanding the key differences in coverage scope, eligibility, and premium costs helps individuals choose appropriate protection based on income levels and risk exposure.

Key Differences Between Disability Insurance and Microinsurance

Disability insurance provides comprehensive income replacement with higher coverage limits, often targeting long-term or permanent disabilities, while microinsurance offers affordable, limited benefit plans designed for low-income individuals facing temporary income loss. Disability insurance policies typically require medical underwriting and have longer waiting periods before payouts, whereas microinsurance features simplified claim processes and shorter waiting times to ensure quick financial support. The key differences lie in coverage scope, eligibility criteria, premium costs, and the target demographic's financial resilience.

Coverage Scope: What Each Insurance Type Offers

Disability insurance provides comprehensive income replacement tailored for long-term disabilities, often covering a substantial portion of lost wages with options for partial and total disability claims. Microinsurance targets low-income individuals, offering limited but essential coverage with lower premiums and simplified claim processes, primarily focusing on critical events causing short-term income disruption. The scope of disability insurance is broader with customizable benefits, whereas microinsurance emphasizes accessibility and affordability for underserved populations.

Eligibility Criteria for Disability Insurance vs Microinsurance

Disability insurance typically requires applicants to meet strict eligibility criteria including medical underwriting, employment status, and income verification, targeting individuals with stable jobs and higher incomes. Microinsurance, designed for low-income populations, often features simplified eligibility with minimal documentation and no medical exams to provide easier access for informal workers and vulnerable groups. These differences in eligibility reflect the distinct target markets and affordability considerations between traditional disability insurance and microinsurance products.

Premium Costs: Affordability Comparison

Disability insurance typically involves higher premium costs due to comprehensive coverage and longer benefit periods, making it less affordable for low-income individuals. Microinsurance offers a cost-effective alternative with significantly lower premiums tailored for short-term income loss, enhancing accessibility for underserved populations. Premium affordability in microinsurance supports wider adoption among those who cannot sustain the financial burden of traditional disability insurance.

Claims Process: Ease and Speed of Accessing Benefits

Disability insurance typically involves a more detailed claims process, requiring extensive medical documentation and waiting periods, which can delay benefit access. Microinsurance offers a simplified claims procedure with faster approval and payout times, designed to accommodate lower-income individuals needing immediate financial support. The streamlined process of microinsurance enhances ease and speed, making it more accessible for quick loss of income recovery.

Income Protection: How Each Policy Supports Policyholders

Disability insurance provides comprehensive income protection by offering substantial monthly benefits to policyholders unable to work due to illness or injury, often with longer benefit periods to ensure financial stability. Microinsurance, designed for low-income individuals, supports policyholders with affordable, limited coverage focused on short-term income loss, making it accessible but less comprehensive. Both policies aim to secure income, yet disability insurance delivers robust, sustained support while microinsurance offers essential, immediate relief for marginalized populations.

Ideal Candidates for Disability Insurance and Microinsurance

Disability insurance is ideal for individuals with stable employment and higher income levels who require comprehensive coverage against long-term income loss due to disabling conditions. Microinsurance suits low-income earners and informal sector workers seeking affordable, limited-protection plans for short-term disability or income interruption. Employers, freelancers, and self-employed professionals often benefit more from disability insurance, whereas microinsurance addresses the financial vulnerability of underserved communities.

Limitations and Exclusions to Consider

Disability insurance typically offers comprehensive coverage for loss of income but often excludes pre-existing conditions, self-inflicted injuries, and short-term disabilities under a certain duration. Microinsurance provides affordable, accessible protection primarily for low-income individuals but usually comes with limited benefit amounts and narrower coverage scopes. Both products require careful review of policy limitations, waiting periods, and claim exclusions to ensure adequate financial protection during income loss.

Choosing the Right Insurance for Loss of Income

Disability insurance offers comprehensive coverage for long-term income loss due to illness or injury, typically suited for individuals seeking substantial financial protection. Microinsurance provides affordable, targeted benefits with simplified claims processes, ideal for low-income earners or those in informal employment sectors. Selecting the right insurance depends on factors such as coverage needs, premium affordability, and claim accessibility to ensure optimal income protection during disability.

Related Important Terms

Income Protection Microinsurance

Income Protection Microinsurance offers affordable, tailored coverage for low-income individuals facing temporary or permanent disability, ensuring consistent income replacement and financial stability. Compared to traditional Disability Insurance, microinsurance provides accessible premiums, simplified enrollment, and rapid claim processes, making it ideal for vulnerable populations with limited financial resources.

Digital Disability Coverage

Digital disability coverage offers streamlined claims processing and real-time policy management, making it an efficient solution compared to traditional microinsurance for loss of income, which typically provides limited benefits and slower payout times. Leveraging advanced analytics and mobile platforms, digital disability insurance enhances accessibility and personalized protection for working professionals facing income disruption due to disability.

Pay-as-You-Go Disability Plans

Pay-as-You-Go Disability Plans offer flexible premium payments based on actual income, making them a practical alternative to traditional Disability Insurance for workers with irregular earnings. Microinsurance tailored for loss of income provides affordable, accessible coverage with lower sums assured, catering specifically to low-income individuals who need short-term financial protection.

Parametric Loss-of-Income Insurance

Parametric loss-of-income insurance offers predefined payout triggers based on measurable events, providing faster claims processing and transparency compared to traditional disability insurance. Microinsurance targets low-income individuals with affordable premiums and limited coverage, while parametric solutions enhance these benefits by reducing administrative costs and offering more precise risk assessments.

Embedded Disability Riders

Embedded disability riders in traditional disability insurance offer comprehensive income protection with higher coverage limits and longer benefit periods, suited for individuals needing substantial financial security. Microinsurance for loss of income provides affordable, simplified coverage with lower premiums and benefits, targeting low-income populations but often lacks embedded riders for seamless integration.

Bite-sized Income Replacement Policy

Disability insurance provides comprehensive income protection for long-term disabilities, while microinsurance offers affordable, bite-sized income replacement policies designed for short-term or minimal loss scenarios, making it accessible for lower-income individuals. Bite-sized income replacement policies focus on quick payouts and simplified coverage to ensure financial stability during brief income interruptions without the complexity of traditional disability plans.

On-demand Micro Disability Cover

On-demand micro disability insurance offers flexible, affordable coverage tailored for short-term income loss, making it ideal for gig workers and freelancers who need instant protection without long-term commitments. Unlike traditional disability insurance, this microinsurance product provides quick claim settlements and customizable coverage periods, ensuring seamless financial support during unexpected work disruptions.

Platform-based Microinsurance Bundles

Platform-based microinsurance bundles offer tailored disability insurance solutions that provide affordable, accessible income protection for low-income individuals, leveraging digital platforms for seamless policy management and claims processing. These bundles typically feature simplified underwriting and flexible premium payments, making them an efficient alternative to traditional disability insurance by reducing administrative costs and enhancing customer reach.

Flexible Term Disability Microinsurance

Flexible Term Disability Microinsurance offers tailored coverage for short-term income loss, providing affordable protection specifically designed for low-income individuals or informal workers. Unlike traditional disability insurance, it features adjustable benefit periods and premium options, ensuring accessible financial security during temporary disability without long-term commitment.

Hybrid Micro & Disability Insurance Solutions

Hybrid micro and disability insurance solutions combine the affordability and accessibility of microinsurance with the comprehensive coverage of traditional disability insurance, effectively addressing income loss for low-to-middle income earners. These innovative products leverage digital platforms and tailored underwriting to provide immediate financial support and long-term protection, bridging gaps in conventional insurance markets.

Disability Insurance vs Microinsurance for loss of income. Infographic