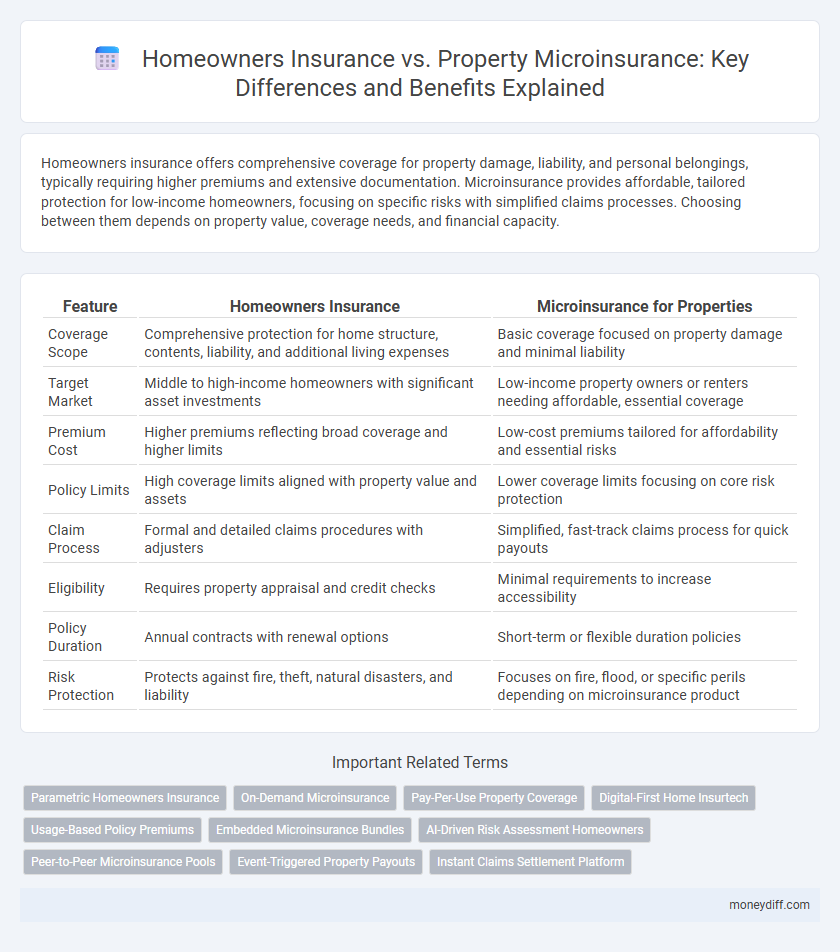

Homeowners insurance offers comprehensive coverage for property damage, liability, and personal belongings, typically requiring higher premiums and extensive documentation. Microinsurance provides affordable, tailored protection for low-income homeowners, focusing on specific risks with simplified claims processes. Choosing between them depends on property value, coverage needs, and financial capacity.

Table of Comparison

| Feature | Homeowners Insurance | Microinsurance for Properties |

|---|---|---|

| Coverage Scope | Comprehensive protection for home structure, contents, liability, and additional living expenses | Basic coverage focused on property damage and minimal liability |

| Target Market | Middle to high-income homeowners with significant asset investments | Low-income property owners or renters needing affordable, essential coverage |

| Premium Cost | Higher premiums reflecting broad coverage and higher limits | Low-cost premiums tailored for affordability and essential risks |

| Policy Limits | High coverage limits aligned with property value and assets | Lower coverage limits focusing on core risk protection |

| Claim Process | Formal and detailed claims procedures with adjusters | Simplified, fast-track claims process for quick payouts |

| Eligibility | Requires property appraisal and credit checks | Minimal requirements to increase accessibility |

| Policy Duration | Annual contracts with renewal options | Short-term or flexible duration policies |

| Risk Protection | Protects against fire, theft, natural disasters, and liability | Focuses on fire, flood, or specific perils depending on microinsurance product |

Understanding Homeowners Insurance: Key Features

Homeowners insurance provides comprehensive coverage for property damage, personal belongings, and liability protection, often including additional living expenses if a home becomes uninhabitable. Policies typically cover risks such as fire, theft, natural disasters, and vandalism, while offering financial security against costly repairs or legal claims. Key features also include dwelling protection, personal property coverage, and liability limits tailored to the homeowner's risk profile and property value.

What Is Microinsurance for Properties?

Microinsurance for properties offers affordable, low-premium coverage designed to protect low-income homeowners against risks such as fire, theft, and natural disasters. Unlike traditional homeowners insurance, microinsurance provides simplified policies with lower coverage limits and streamlined claims processes tailored for economically vulnerable populations. This targeted insurance solution increases accessibility and financial protection for property owners who may otherwise lack adequate insurance options.

Coverage Comparison: Homeowners Insurance vs Microinsurance

Homeowners insurance typically offers comprehensive coverage, including dwelling protection, personal property, liability, and additional living expenses, while microinsurance provides limited protection tailored for low-income property owners with basic coverage for structural damage and fire. Homeowners policies often include higher coverage limits and broader perils, whereas microinsurance policies focus on affordability and essential risks, frequently with lower premiums and deductibles. Choosing between them depends on property value, risk exposure, and financial capacity to ensure adequate protection against potential losses.

Cost Differences: Premiums and Affordability

Homeowners insurance typically involves higher premiums reflecting comprehensive coverage for property damage, liability, and personal belongings, while microinsurance offers lower-cost premiums tailored to essential property protection and limited risks. The affordability of microinsurance makes it accessible for low-income homeowners or renters who cannot afford traditional policies, enabling broader financial inclusion in property insurance markets. Cost differences primarily arise from the scope of coverage and administrative efficiencies, with microinsurance optimizing affordability through simplified underwriting and smaller coverage limits.

Eligibility and Accessibility for Different Property Owners

Homeowners insurance typically requires comprehensive property documentation and credit verification, making eligibility stringent for traditional homeowners with standard residential properties. Microinsurance targets low-income or informal property owners by offering simplified enrollment processes and minimal documentation, enhancing accessibility for renters, small landlords, or owners of informal housing structures. Coverage options in microinsurance are often more flexible and affordable, addressing the needs of diverse property owners who might not qualify for conventional homeowners insurance.

Claims Process: Traditional vs Microinsurance

Homeowners insurance claims involve extensive paperwork, detailed damage assessments, and longer processing times, often requiring in-person inspections by adjusters to validate losses. Microinsurance for properties streamlines claims with digital submissions, automated damage evaluations, and faster payouts, leveraging mobile technology and data analytics to reduce claim settlement duration. This efficiency in microinsurance addresses the needs of low-income property owners by providing accessible and prompt financial protection.

Flexibility of Policy Terms and Customization

Homeowners insurance typically offers comprehensive coverage with standardized policy terms suitable for full-value properties, while microinsurance provides more flexible and customizable options tailored to low-income or small-scale property owners. Microinsurance policies often allow adjustments in coverage limits, premiums, and specific risk protections to better match individual needs and budget constraints. The customization capabilities in microinsurance enhance accessibility and affordability, addressing gaps left by traditional homeowners insurance in underserved markets.

Risk Protection: Which Offers Better Security?

Homeowners insurance provides comprehensive coverage against risks such as fire, theft, and natural disasters, offering higher policy limits and extensive protection for property values. Microinsurance, designed for low-income households, offers limited coverage with lower premiums but often excludes major perils and has strict payout caps. For robust risk protection, homeowners insurance generally delivers better security due to broader coverage and higher financial safeguards.

Target Audience: Who Should Choose Which?

Homeowners insurance is ideal for property owners seeking comprehensive coverage, including protection against fire, theft, liability, and natural disasters, typically suited for middle to upper-income families with significant assets. Microinsurance targets low-income homeowners or renters in vulnerable regions, offering affordable, basic protection against specific risks such as floods or earthquakes, helping to mitigate financial losses from disasters. Those with limited budgets and high exposure to localized hazards should consider microinsurance, whereas those needing extensive coverage and asset protection should opt for traditional homeowners insurance.

Making the Right Choice: Factors to Consider

Evaluating homeowners insurance versus microinsurance requires careful consideration of coverage limits, premium costs, and property value to ensure adequate protection. Homeowners insurance typically offers comprehensive coverage suitable for higher-value properties, while microinsurance provides affordable, tailored policies ideal for lower-value homes or renters. Assessing risk factors, financial capacity, and specific needs helps determine which option delivers the best balance of security and affordability.

Related Important Terms

Parametric Homeowners Insurance

Parametric homeowners insurance offers a streamlined alternative to traditional homeowners policies by triggering payouts based on predefined weather or disaster parameters, reducing claims processing time and increasing transparency. This contrasts with microinsurance, which provides low-cost, limited coverage often targeting low-income property owners, but may involve slower claim settlements due to traditional verification requirements.

On-Demand Microinsurance

On-demand microinsurance for properties offers flexible, low-cost coverage tailored to specific homeowner needs, contrasting with traditional comprehensive homeowners insurance that requires long-term commitments and higher premiums. This model enables instant, usage-based protection ideal for renters or occasional property users seeking affordable financial security against risks like fire, theft, or natural disasters.

Pay-Per-Use Property Coverage

Pay-Per-Use Property Coverage in homeowners insurance offers flexible premiums based on actual property usage and risk exposure, whereas microinsurance provides affordable, limited-scope protection primarily tailored for low-income homeowners with essential asset coverage. This usage-based model enhances cost-efficiency and accessibility, making it ideal for sporadically occupied or rental properties in emerging markets.

Digital-First Home Insurtech

Digital-first home insurtech platforms revolutionize property protection by offering streamlined homeowners insurance with comprehensive coverage, while microinsurance targets affordable, flexible protection for low-value properties or short-term needs. Leveraging AI and data analytics, these digital solutions optimize underwriting, claims processing, and customer engagement, enabling personalized policies and enhancing risk management in diverse housing markets.

Usage-Based Policy Premiums

Usage-based policy premiums in homeowners insurance leverage extensive property data, risk assessments, and historical claims to set fixed rates, while microinsurance employs real-time usage metrics and localized risk factors to offer flexible, affordable coverage tailored to low-income property owners. This innovative approach in microinsurance enhances accessibility by adjusting premiums dynamically based on property usage patterns and environmental conditions.

Embedded Microinsurance Bundles

Embedded microinsurance bundles integrate affordable, tailored coverage within property purchases, offering homeowners insurance solutions that address low-income households' specific risks. This approach enhances accessibility and financial protection by embedding microinsurance policies directly into mortgage or property sale agreements, reducing barriers typical of traditional homeowners insurance.

AI-Driven Risk Assessment Homeowners

AI-driven risk assessment in homeowners insurance leverages advanced algorithms and big data to accurately evaluate property risks, enabling tailored coverage and premium pricing. Microinsurance for properties utilizes similar AI technologies but focuses on offering affordable, scalable protection for lower-value homes or renters, addressing underserved markets with efficient, data-driven underwriting processes.

Peer-to-Peer Microinsurance Pools

Peer-to-peer microinsurance pools for homeowners provide affordable, community-based coverage by pooling risks among local property owners, reducing premiums compared to traditional homeowners insurance. These decentralized models enhance claim transparency and faster payouts, especially benefiting low-income households with limited access to conventional insurance markets.

Event-Triggered Property Payouts

Homeowners insurance typically offers comprehensive coverage with higher premiums and deductibles, providing payouts based on specific property damage events such as fire or theft, while microinsurance delivers affordable, event-triggered property payouts designed for low-income households with simplified claim processes and limited coverage scopes. Event-triggered microinsurance policies activate payouts immediately after predefined events like floods or earthquakes, ensuring timely financial support without extensive loss assessments common in traditional homeowners insurance.

Instant Claims Settlement Platform

Homeowners insurance typically offers comprehensive coverage with longer claim processing times, whereas microinsurance for properties leverages an instant claims settlement platform to enable rapid, on-the-spot claim approvals and payouts. This platform utilizes digital verification and automated workflows to minimize delays, enhancing customer satisfaction and financial security for low-income property owners.

Homeowners Insurance vs Microinsurance for properties. Infographic