Long-term care insurance offers dedicated coverage for nursing home, assisted living, and home care expenses, providing financial protection exclusively for elder care needs. Hybrid life-long-term care insurance combines life insurance with long-term care benefits, allowing policyholders to access the death benefit for care costs or leave a legacy if care is not needed. Choosing between these options depends on budget, flexibility preferences, and the desire for potential inheritance alongside coverage for chronic illness or disability care.

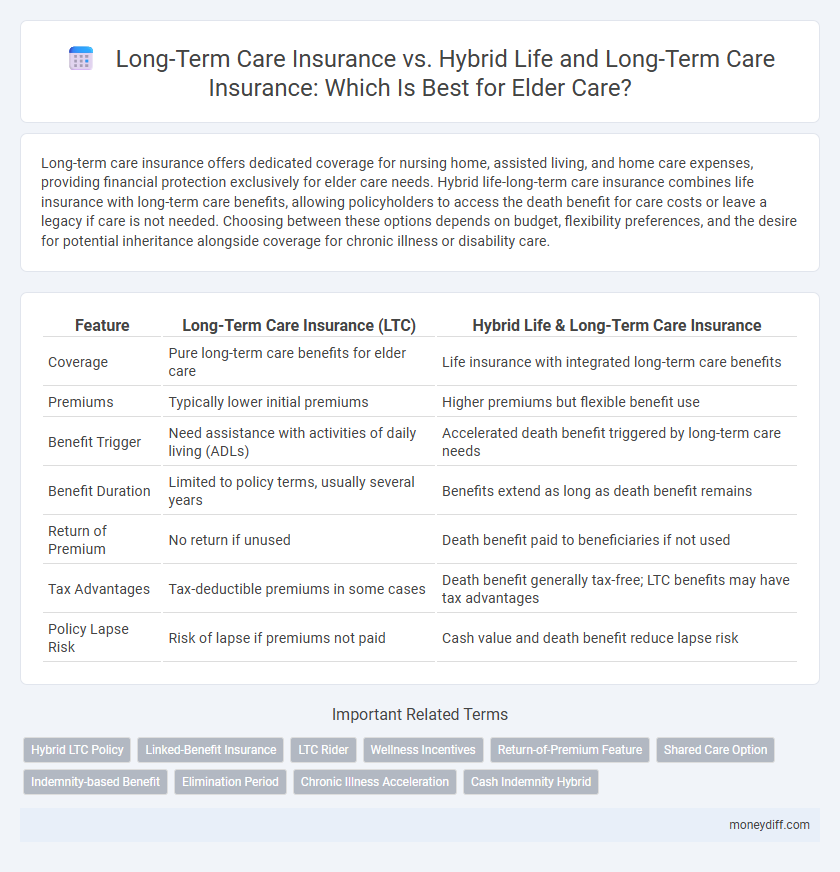

Table of Comparison

| Feature | Long-Term Care Insurance (LTC) | Hybrid Life & Long-Term Care Insurance |

|---|---|---|

| Coverage | Pure long-term care benefits for elder care | Life insurance with integrated long-term care benefits |

| Premiums | Typically lower initial premiums | Higher premiums but flexible benefit use |

| Benefit Trigger | Need assistance with activities of daily living (ADLs) | Accelerated death benefit triggered by long-term care needs |

| Benefit Duration | Limited to policy terms, usually several years | Benefits extend as long as death benefit remains |

| Return of Premium | No return if unused | Death benefit paid to beneficiaries if not used |

| Tax Advantages | Tax-deductible premiums in some cases | Death benefit generally tax-free; LTC benefits may have tax advantages |

| Policy Lapse Risk | Risk of lapse if premiums not paid | Cash value and death benefit reduce lapse risk |

Understanding Long-Term Care Insurance

Long-term care insurance provides financial coverage for extended elder care services, including nursing home care, assisted living, and home health aides, helping to protect savings from costly medical expenses. In contrast, hybrid life-long-term care insurance combines life insurance benefits with long-term care coverage, offering policyholders a death benefit if care services are not used. Understanding the differences in premium costs, payout structures, and coverage options allows seniors to make informed decisions based on their health needs and financial goals.

What Is Hybrid Life-Long-Term Care Insurance?

Hybrid life-long-term care insurance combines life insurance benefits with long-term care coverage, providing a death benefit if care is not needed and funds to cover elder care expenses if it is. This type of insurance offers a flexible solution for seniors by ensuring financial protection for long-term care while preserving value for beneficiaries. It typically requires a single or limited premium payment, making it a cost-effective option compared to traditional long-term care insurance policies.

Key Differences Between LTC Insurance and Hybrid Policies

Long-Term Care (LTC) Insurance and Hybrid Life-Long-Term Care Insurance policies differ primarily in structure and benefits; traditional LTC insurance offers standalone coverage focused solely on long-term care expenses, while hybrid policies combine life insurance with LTC benefits, providing a death benefit if long-term care is not utilized. LTC insurance typically requires ongoing premium payments and may have inflation protection options, whereas hybrid policies often involve a single premium or limited payments, offering more predictable costs. Hybrid plans can be advantageous for individuals seeking both legacy planning and long-term care coverage without the risk of losing premiums if care is never needed.

Coverage Scope: What Each Policy Offers Elders

Long-Term Care Insurance primarily covers expenses related to nursing home stays, assisted living, and home health care tailored for elder care needs. Hybrid Life-Long-Term Care Insurance combines life insurance benefits with long-term care coverage, providing elders with death benefits if long-term care is not utilized. Hybrid policies often offer more comprehensive financial flexibility by integrating elder care coverage with asset protection and potential cash value growth.

Cost Comparison: Premiums and Long-Term Value

Long-Term Care Insurance typically involves higher premiums with the primary focus on covering extended elder care expenses, whereas Hybrid Life-Long-Term Care Insurance combines life insurance benefits with long-term care coverage, often resulting in more predictable premiums and potential cash value accumulation. Hybrid policies may offer better long-term value through death benefits if long-term care services are not utilized, making them cost-effective for individuals seeking both protection and estate planning advantages. Evaluating cost comparison requires analyzing premium affordability against potential benefits, considering factors like inflation protection, policy duration, and individual health status.

Flexibility and Access to Benefits

Long-term care insurance offers dedicated coverage for elder care expenses, providing policyholders with access to benefits specifically for assisted living, nursing home care, or in-home support. Hybrid life-long-term care insurance combines life insurance with long-term care benefits, allowing greater flexibility by enabling benefits to be accessed either for care needs or as a death benefit to beneficiaries. This hybrid option enhances liquidity, ensuring policyholders can adapt coverage based on evolving care needs while preserving financial value for heirs.

Policy Payouts: How and When You Receive Funds

Long-term care insurance typically provides policy payouts based on eligible care expenses incurred, with monthly or daily benefit limits paid directly to care providers or reimbursed to policyholders after claim approval. Hybrid life-long-term care insurance combines life insurance with long-term care benefits, allowing policyholders to access a portion of the death benefit for qualifying care expenses, often through accelerated payouts that reduce the death benefit accordingly. Payout timing and structure vary, with traditional policies requiring proof of care needs before disbursement, while hybrid policies offer more flexible access to funds, supporting elder care costs without forfeiting all life insurance benefits.

Pros and Cons of Traditional LTC Insurance

Traditional Long-Term Care (LTC) insurance provides dedicated coverage for nursing home, home health care, and assisted living expenses, offering comprehensive financial protection tailored specifically for elder care needs. However, it often comes with higher premiums that can increase over time and the risk of losing coverage if premiums are not maintained. Policyholders benefit from clear, defined benefits but may face strict eligibility requirements and less flexibility compared to hybrid life-long-term care insurance options.

Pros and Cons of Hybrid Life-Long-Term Care Insurance

Hybrid Life-Long-Term Care Insurance combines life insurance with long-term care benefits, offering a death benefit if care is not needed and funds for care if it is. Pros include guaranteed lifetime coverage, potential cash value accumulation, and no separate underwriting for care claims, reducing risk of denial. Cons involve higher premiums compared to traditional long-term care policies and limited flexibility in benefit use, which may not cover all elder care expenses comprehensively.

Choosing the Right Insurance: Factors for Elder Care Needs

Long-term care insurance covers extended services for chronic illness or disability, providing daily living assistance without impacting life insurance benefits. Hybrid life-long-term care insurance combines life insurance with long-term care benefits, offering flexibility and potential cash value for beneficiaries. Factors such as anticipated care duration, premium affordability, inheritance goals, and health status are critical in selecting the right insurance for elder care needs.

Related Important Terms

Hybrid LTC Policy

Hybrid life-long-term care insurance combines life insurance benefits with long-term care coverage, offering policyholders a death benefit if long-term care is not needed, unlike traditional long-term care insurance that solely focuses on care expenses. This integrated approach provides financial flexibility and potential cost savings by pooling premiums for both care and legacy protection, making it a strategic option for elder care planning.

Linked-Benefit Insurance

Linked-benefit insurance combines life insurance with long-term care coverage, providing a dual-purpose policy that pays death benefits if long-term care services are not needed, optimizing value for elder care planning. Compared to traditional long-term care insurance, hybrid policies offer more flexible benefits and potential cash value accumulation, often making them a more cost-effective and comprehensive solution for seniors seeking protection against extended care expenses.

LTC Rider

Long-term care insurance (LTC) provides dedicated coverage for elder care expenses such as nursing home stays and home health care, while hybrid life-long-term care insurance combines life insurance benefits with an LTC rider that accelerates death benefits to cover care costs. The LTC rider on hybrid policies offers flexibility by integrating care benefits with a death benefit payout, often resulting in lower premiums and guaranteed benefits compared to standalone LTC insurance.

Wellness Incentives

Long-term care insurance offers dedicated coverage for extended elder care needs with built-in wellness incentives such as premium discounts for healthy behaviors and regular health assessments. Hybrid life-long-term care insurance combines life insurance benefits with long-term care coverage, providing wellness rewards through cash value accumulation linked to proactive health management.

Return-of-Premium Feature

Long-term care insurance policies with a return-of-premium feature refund some or all of the premiums paid if benefits are not used, providing a financial safety net for elder care expenses. Hybrid life-long-term care insurance combines life insurance with long-term care benefits, often including a return-of-premium option that enhances value by offering a death benefit or premium refunds if long-term care services are unnecessary.

Shared Care Option

The Shared Care Option in Hybrid Life-Long-Term Care Insurance allows spouses to pool benefits, providing a flexible and cost-effective approach to elder care by maximizing available long-term care funds. Long-Term Care Insurance typically offers individual coverage limits without benefit sharing, which may result in higher costs and less adaptability for couples managing care needs together.

Indemnity-based Benefit

Long-term care insurance with indemnity-based benefits reimburses policyholders for actual expenses incurred, offering flexibility in elder care spending, while hybrid life-long-term care insurance combines these benefits with a life insurance policy, providing a death benefit if long-term care services are not used. Choosing between these options depends on the need for comprehensive elder care coverage and potential financial legacy for beneficiaries.

Elimination Period

Long-term care insurance typically features an elimination period ranging from 30 to 90 days, during which policyholders must pay out-of-pocket before benefits commence. Hybrid life-long-term care insurance combines life insurance with long-term care benefits and often offers shorter or waived elimination periods, enhancing immediate access to care funds for elder care needs.

Chronic Illness Acceleration

Long-Term Care Insurance provides dedicated coverage for elder care needs, activating benefits specifically for chronic illness acceleration that requires extended support services. Hybrid Life-Long-Term Care Insurance combines life insurance with chronic illness acceleration riders, offering both death benefits and accelerated access to funds for long-term care expenses, enhancing financial flexibility for elder care planning.

Cash Indemnity Hybrid

Cash Indemnity Hybrid Life-Long-Term Care Insurance combines life insurance with a cash indemnity long-term care benefit, offering flexible payout options that can cover a wide range of elder care expenses without requiring strict expense documentation. Unlike traditional long-term care insurance, this hybrid policy provides a death benefit if long-term care is not needed, ensuring financial value for policyholders and their beneficiaries.

Long-Term Care Insurance vs Hybrid Life-Long-Term Care Insurance for elder care. Infographic