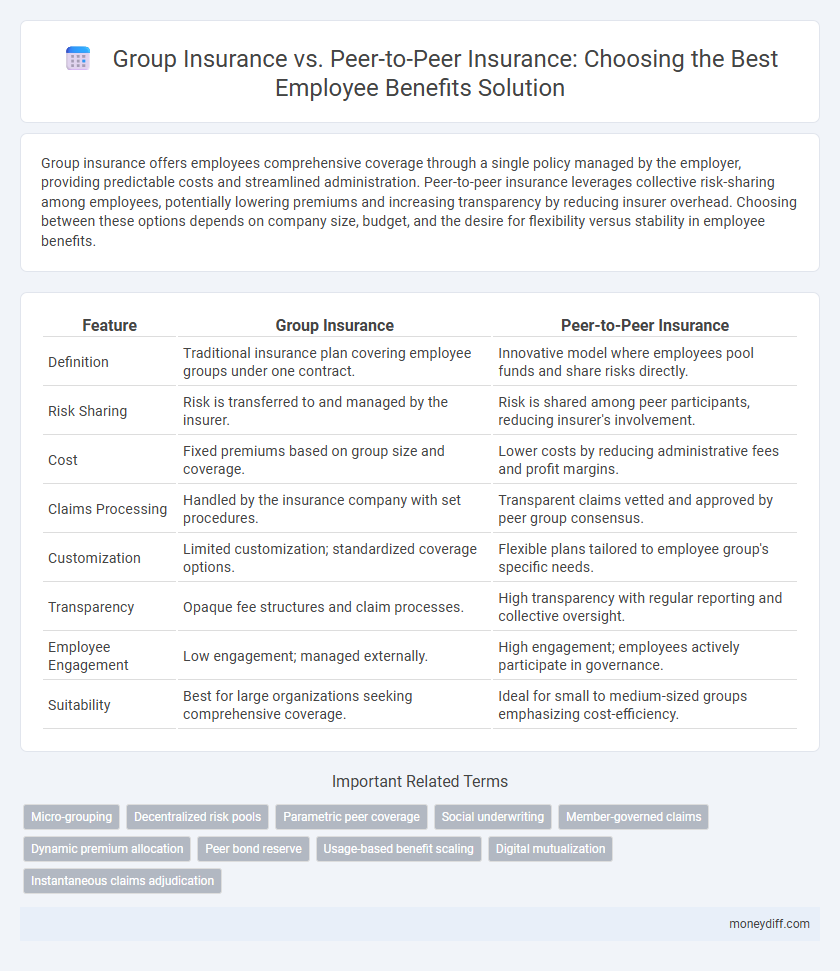

Group insurance offers employees comprehensive coverage through a single policy managed by the employer, providing predictable costs and streamlined administration. Peer-to-peer insurance leverages collective risk-sharing among employees, potentially lowering premiums and increasing transparency by reducing insurer overhead. Choosing between these options depends on company size, budget, and the desire for flexibility versus stability in employee benefits.

Table of Comparison

| Feature | Group Insurance | Peer-to-Peer Insurance |

|---|---|---|

| Definition | Traditional insurance plan covering employee groups under one contract. | Innovative model where employees pool funds and share risks directly. |

| Risk Sharing | Risk is transferred to and managed by the insurer. | Risk is shared among peer participants, reducing insurer's involvement. |

| Cost | Fixed premiums based on group size and coverage. | Lower costs by reducing administrative fees and profit margins. |

| Claims Processing | Handled by the insurance company with set procedures. | Transparent claims vetted and approved by peer group consensus. |

| Customization | Limited customization; standardized coverage options. | Flexible plans tailored to employee group's specific needs. |

| Transparency | Opaque fee structures and claim processes. | High transparency with regular reporting and collective oversight. |

| Employee Engagement | Low engagement; managed externally. | High engagement; employees actively participate in governance. |

| Suitability | Best for large organizations seeking comprehensive coverage. | Ideal for small to medium-sized groups emphasizing cost-efficiency. |

Introduction to Employee Benefits Insurance Options

Group insurance offers employees comprehensive coverage through a single policy managed by the employer, facilitating cost-efficiency and simplified administration. Peer-to-peer insurance leverages a decentralized model where employees pool funds directly, promoting transparency and potential savings by reducing traditional insurer margins. Understanding these distinct frameworks is crucial for selecting optimal employee benefits insurance that aligns with organizational goals and workforce preferences.

What is Group Insurance?

Group insurance is a single policy covering a defined group of employees, typically provided and funded by the employer to offer health, life, or disability benefits. It leverages collective risk pooling, resulting in lower premiums and standardized coverage across the workforce. This approach ensures consistent employee benefits and simplifies administration compared to individual insurance plans.

Understanding Peer-to-Peer Insurance

Peer-to-peer insurance for employee benefits operates by pooling resources among employees to share risks directly, reducing reliance on traditional insurers and often lowering costs. This model fosters transparency and trust, as claim payouts are collectively managed, creating incentives for reduced fraudulent claims and greater accountability. Understanding peer-to-peer insurance helps employers evaluate alternative group insurance solutions that emphasize collaboration and cost efficiency within employee benefits programs.

Key Differences Between Group and Peer-to-Peer Insurance

Group insurance offers coverage through a centralized policy purchased by an employer, providing uniform benefits and risk pooling across employees, while peer-to-peer insurance leverages decentralized risk sharing among employees themselves, often using technology platforms to manage claims and premiums. Group insurance typically results in predictable premiums and comprehensive coverage but may involve administrative complexities, whereas peer-to-peer insurance emphasizes transparency, potential cost savings, and community-based trust with varied risk exposure. Key differentiators include the centralized underwriting model of group insurance versus the distributed risk model in peer-to-peer schemes, impacting cost structures, claim processes, and employee engagement in benefit management.

Cost Comparison: Group vs Peer-to-Peer Insurance

Group insurance typically offers lower premiums per employee due to risk pooling across a larger population, reducing individual costs. Peer-to-peer insurance can lower expenses further by minimizing administrative fees and redistributing unclaimed premiums among members, enhancing cost efficiency. Employers should evaluate both options based on company size, claims history, and potential savings from reduced overhead.

Coverage and Flexibility: Which Offers More?

Group insurance typically provides broader coverage with standardized benefits tailored for diverse employee needs, ensuring consistent protection across the workforce. Peer-to-peer insurance offers enhanced flexibility by allowing participants to customize coverage and share risk within smaller, trust-based groups, often resulting in cost savings and personalized plans. While group insurance excels in comprehensive, uniform benefits, peer-to-peer models empower employees with adaptable, community-driven options better suited for specific or evolving coverage preferences.

Claims Process: Ease and Transparency

Group insurance offers a streamlined claims process managed by established insurance providers, ensuring clear documentation requirements and faster approvals for employee benefits. Peer-to-peer insurance leverages blockchain technology to enhance transparency and reduce administrative overhead, allowing employees to track claim statuses in real time. Both models prioritize ease of access, but peer-to-peer often provides increased visibility into claim handling compared to traditional group insurance systems.

Employee Experience and Engagement

Group insurance provides employees with standardized coverage and predictable benefits, enhancing their sense of security and trust in the employer's commitment to well-being. Peer-to-peer insurance fosters a community-driven approach, encouraging employee engagement through shared risk and collective decision-making, which can lead to increased collaboration and satisfaction. Both models influence employee experience differently, with group insurance emphasizing stability and peer-to-peer insurance promoting active participation and a stronger sense of ownership.

Risk Sharing and Financial Stability

Group insurance pools risk across a large number of employees, providing financial stability through diversified risk and predictable premium costs. Peer-to-peer insurance enables smaller groups of employees to share risk directly, reducing administrative costs and incentivizing loss prevention but may face challenges in maintaining consistent financial resilience. Both models aim to optimize employee benefits by balancing risk sharing with financial sustainability.

Choosing the Right Insurance Model for Your Organization

Group insurance provides organizations with comprehensive coverage plans negotiated for employees, offering predictable premiums and broad risk pooling. Peer-to-peer insurance leverages social networks to create cost-efficient, transparent coverage, often resulting in lower administrative fees and enhanced member engagement. Evaluating your organization's size, risk tolerance, and cultural fit ensures the optimal benefits model that balances cost, coverage, and employee satisfaction.

Related Important Terms

Micro-grouping

Micro-grouping in employee benefits enhances personalization by creating smaller, more homogeneous insurance pools within group insurance frameworks, which improves risk assessment and premium accuracy. Peer-to-peer insurance leverages micro-groups to foster trust and reduce administrative costs, aligning with employee interests through collective claims management and shared incentives.

Decentralized risk pools

Group insurance leverages centralized risk pools managed by insurers to distribute employee benefits costs broadly, while peer-to-peer insurance utilizes decentralized risk pools where members share risks directly, enhancing transparency and potentially lowering premiums through collective self-management. Decentralized risk pools in peer-to-peer insurance foster greater employee engagement and trust by aligning incentives and reducing dependence on traditional insurers.

Parametric peer coverage

Group insurance typically offers standardized employee benefits with fixed coverage limits, while parametric peer-to-peer insurance provides flexible, data-driven payouts based on predefined parameters such as biometric data or event triggers. This parametric approach enhances transparency and speed in claims processing by automatically disbursing funds when specific conditions are met, improving overall employee satisfaction and cost efficiency.

Social underwriting

Group insurance leverages traditional underwriting based on collective risk pools and employer-sponsored plans, providing stable premiums and coverage guarantees for employees. Peer-to-peer insurance innovates with social underwriting by assessing risk through social networks and community behavior, promoting transparency and potentially lowering costs through shared accountability.

Member-governed claims

Group insurance provides a traditional employer-managed structure with claims administered by insurers, while peer-to-peer insurance allows employees to govern claims collectively, enhancing transparency and reducing fraud. Member-governed claims in peer-to-peer models foster trust and align benefits with actual group needs, often resulting in lower costs and faster reimbursements.

Dynamic premium allocation

Group insurance typically features fixed premium rates based on collective risk assessment, offering predictable costs for employee benefits, while peer-to-peer insurance employs dynamic premium allocation, adjusting rates in real-time according to individual claim behavior and group performance, enhancing cost efficiency and transparency. This dynamic approach aligns incentives among employees, reducing moral hazard and potentially lowering overall insurance expenses by rewarding lower-risk groups.

Peer bond reserve

Peer-to-peer insurance leverages a peer bond reserve, which pools member contributions to create a transparent and self-managed fund that reduces reliance on traditional insurer reserves, potentially lowering costs and enhancing trust among employees. This reserve system contrasts with group insurance, where premiums are paid to an insurer who manages risk and claims without direct employee involvement in fund governance.

Usage-based benefit scaling

Group insurance provides standardized employee benefits with fixed premiums based on collective risk assessment, while peer-to-peer insurance enables usage-based benefit scaling by allowing employees to share risk and adjust coverage dynamically according to actual usage or claims. This usage-based model in peer-to-peer insurance promotes cost efficiency and personalized benefits, contrasting with the rigid structure of traditional group insurance plans.

Digital mutualization

Group insurance leverages collective risk pooling through traditional insurers, providing standardized employee benefits with predictable premiums, while peer-to-peer insurance utilizes digital mutualization platforms to directly connect employees, reducing administrative costs and enhancing transparency by sharing claims within smaller, trust-based communities. Digital mutualization in peer-to-peer insurance fosters increased engagement, faster claim processing, and personalized coverage options, challenging conventional group insurance models with innovative, cost-effective employee benefit solutions.

Instantaneous claims adjudication

Group insurance streamlines employee benefits by offering centralized risk pooling and standardized coverage, whereas peer-to-peer insurance leverages decentralized networks for more transparent risk sharing. Instantaneous claims adjudication is significantly enhanced in peer-to-peer models through blockchain technology and smart contracts, reducing processing time from days to seconds compared to traditional group insurance systems.

Group insurance vs Peer-to-peer insurance for employee benefits. Infographic