Umbrella insurance offers comprehensive, high-limit liability coverage that protects assets beyond the limits of standard policies, making it ideal for safeguarding wealth against major claims or lawsuits. Usage-based insurance calculates premiums based on actual driving behavior, providing cost-effective coverage tailored to low-mileage or safe drivers, but it primarily focuses on vehicle-related risks. Combining umbrella insurance with usage-based policies can optimize asset protection by balancing broad liability coverage with personalized, usage-sensitive vehicle insurance.

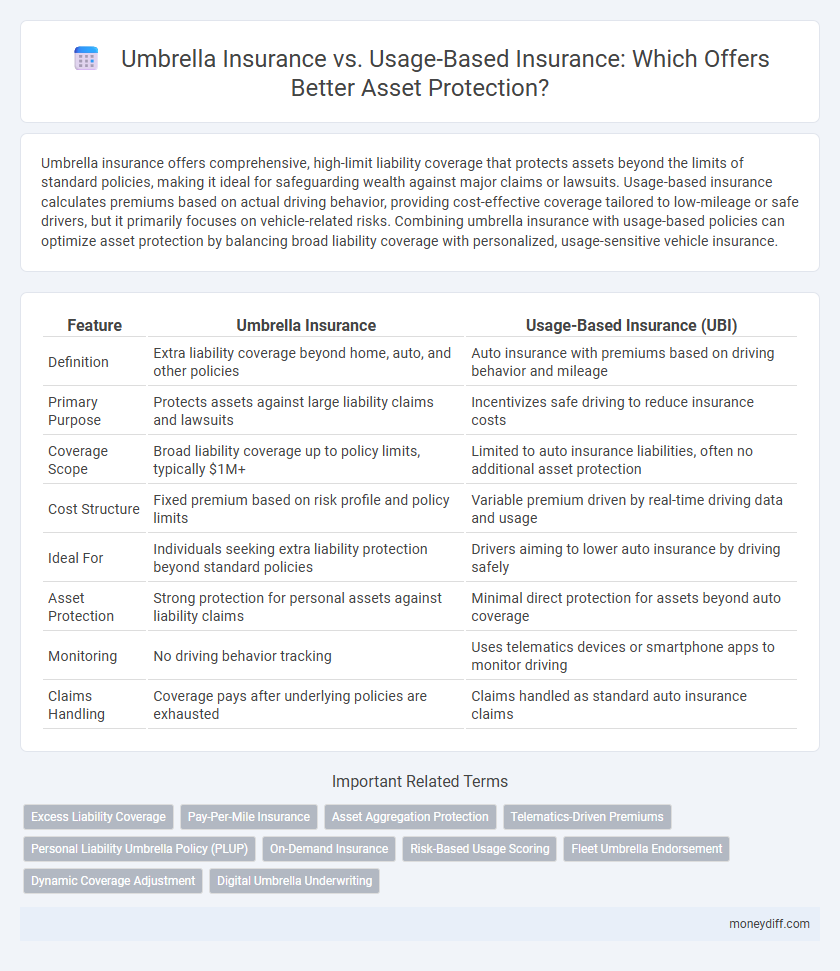

Table of Comparison

| Feature | Umbrella Insurance | Usage-Based Insurance (UBI) |

|---|---|---|

| Definition | Extra liability coverage beyond home, auto, and other policies | Auto insurance with premiums based on driving behavior and mileage |

| Primary Purpose | Protects assets against large liability claims and lawsuits | Incentivizes safe driving to reduce insurance costs |

| Coverage Scope | Broad liability coverage up to policy limits, typically $1M+ | Limited to auto insurance liabilities, often no additional asset protection |

| Cost Structure | Fixed premium based on risk profile and policy limits | Variable premium driven by real-time driving data and usage |

| Ideal For | Individuals seeking extra liability protection beyond standard policies | Drivers aiming to lower auto insurance by driving safely |

| Asset Protection | Strong protection for personal assets against liability claims | Minimal direct protection for assets beyond auto coverage |

| Monitoring | No driving behavior tracking | Uses telematics devices or smartphone apps to monitor driving |

| Claims Handling | Coverage pays after underlying policies are exhausted | Claims handled as standard auto insurance claims |

Understanding Umbrella Insurance: Broad-Spectrum Asset Protection

Umbrella insurance provides extensive liability coverage that extends beyond the limits of standard home, auto, or watercraft insurance policies, protecting your assets against large, unexpected claims or lawsuits. This type of insurance is ideal for safeguarding diverse assets by covering legal fees, medical expenses, and damages that exceed primary policy limits, offering a broad spectrum of financial security. Its comprehensive nature makes umbrella insurance a critical component for individuals seeking robust protection against high-value liability risks.

What is Usage-Based Insurance? Personalized Coverage Explained

Usage-Based Insurance (UBI) offers personalized coverage by using telematics technology to monitor driving behavior, such as speed, braking, and mileage. This data-driven approach allows insurers to adjust premiums based on actual risk levels, providing cost-efficient protection tailored to individual driving habits. Unlike traditional umbrella insurance that extends broad liability coverage, UBI focuses on customizing auto insurance policies for optimized asset protection.

Key Differences: Umbrella Insurance vs Usage-Based Insurance

Umbrella insurance provides extensive liability coverage beyond standard policy limits, safeguarding assets against large claims and lawsuits, while usage-based insurance calculates premiums based on actual driving behavior, offering personalized rates primarily for auto insurance. Umbrella insurance protects a broad range of assets and risks, including home and auto liabilities, whereas usage-based insurance specifically targets risk assessment related to vehicle use and mileage. Choosing between the two depends on whether the goal is comprehensive liability protection with asset preservation or customized premium savings based on driving patterns.

Coverage Scope: Which Offers More Comprehensive Asset Protection?

Umbrella insurance provides broader asset protection by extending liability coverage beyond typical policy limits, safeguarding against major claims and lawsuits that could threaten personal assets. Usage-based insurance focuses primarily on auto coverage, adjusting premiums based on driving behavior, which limits its scope to vehicle-related risks. For comprehensive asset protection, umbrella insurance offers more extensive coverage across various liability exposures compared to the narrower, behavior-driven scope of usage-based insurance.

Cost Comparison: Premiums and Savings Potential

Umbrella insurance typically offers broader liability coverage at a higher premium, providing extensive protection beyond standard policies. Usage-based insurance (UBI) adjusts premiums based on driving behavior, often resulting in significant savings for low-mileage, safe drivers. Comparing costs, UBI can reduce expenses substantially for individual policyholders, while umbrella insurance remains a cost-effective choice for comprehensive asset protection against large claims.

Scenarios Where Umbrella Insurance Excels

Umbrella insurance provides superior asset protection in scenarios involving high liability risks such as serious car accidents, significant property damage, or costly legal claims that exceed the limits of underlying policies. It offers extended coverage beyond standard auto and homeowner's insurance, safeguarding personal assets including savings, investments, and real estate from lawsuits or large settlements. In contrast to usage-based insurance, which adjusts premiums based on driving behavior, umbrella insurance excels in protecting against catastrophic liability exposures unrelated to mileage or usage patterns.

When to Choose Usage-Based Insurance for Asset Protection

Usage-based insurance (UBI) is ideal when precise driving behavior and mileage data can directly influence premium costs, making it cost-effective for low-mileage or safe drivers seeking customized asset protection. UBI leverages telematics to monitor real-time driving habits, providing personalized risk assessment that enhances protection while potentially lowering expenses. Opt for usage-based insurance when asset protection benefits from dynamic premium adjustments tied to actual usage patterns rather than static coverage limits.

Impact on Liability: Protecting Against Unexpected Claims

Umbrella insurance offers broad liability coverage that extends beyond standard policies, providing protection against high-cost or unexpected claims that could threaten your assets. Usage-based insurance (UBI) adjusts premiums based on driving behavior, potentially lowering costs but offering limited impact on liability protection for non-driving-related claims. Selecting umbrella insurance enhances overall asset protection by covering gaps in liability, while usage-based insurance primarily focuses on fair pricing for vehicle-related risks.

Assessing Your Asset Protection Needs: Which Policy Fits Best?

Assessing your asset protection needs requires comparing Umbrella Insurance and Usage-Based Insurance based on coverage scope and risk factors. Umbrella Insurance offers high-limit liability protection beyond standard policies, ideal for safeguarding diverse assets against significant claims. Usage-Based Insurance customizes premiums and coverage based on driving behavior, providing cost efficiency for vehicle-related risks but limited protection for broader assets.

Making the Right Choice: Factors to Consider for Financial Security

Umbrella insurance provides extended liability coverage beyond standard policies, offering robust financial protection against major claims and lawsuits. Usage-based insurance calculates premiums based on driving behavior, potentially lowering costs for safe drivers but offering less comprehensive asset protection. Evaluating personal risk exposure, driving habits, and coverage needs is crucial to making an informed choice for asset protection and long-term financial security.

Related Important Terms

Excess Liability Coverage

Umbrella insurance provides excess liability coverage that extends beyond the limits of standard home, auto, or boat insurance policies, offering an extra layer of financial protection against large claims or lawsuits. Usage-based insurance, while primarily focused on adjusting premiums based on driving behavior, typically does not offer additional excess liability coverage, making umbrella insurance essential for comprehensive asset protection.

Pay-Per-Mile Insurance

Umbrella insurance offers broad liability coverage beyond the limits of standard policies, protecting assets from significant claims and lawsuits. Pay-Per-Mile insurance, a usage-based model, lowers premiums by charging policyholders based on actual miles driven, providing cost-effective protection for low-mileage vehicles.

Asset Aggregation Protection

Umbrella insurance offers broad liability coverage beyond standard policy limits, providing enhanced asset aggregation protection by covering multiple liabilities under a single plan. Usage-based insurance adjusts premiums based on driving behavior, primarily protecting auto assets without extending to overall personal asset aggregation.

Telematics-Driven Premiums

Umbrella insurance provides broad liability coverage beyond standard policies, offering extensive asset protection against large claims, while usage-based insurance leverages telematics-driven premiums to tailor costs based on real-time driving behavior and mileage, enhancing personalized risk assessment. Telematics technology collects detailed data on driving patterns, enabling insurers to optimize pricing models and incentivize safer driving habits, making usage-based insurance a dynamic option for cost-conscious policyholders.

Personal Liability Umbrella Policy (PLUP)

Personal Liability Umbrella Policy (PLUP) offers extended asset protection by providing high-limit liability coverage beyond standard insurance policies, addressing claims such as bodily injury or property damage. Usage-Based Insurance (UBI) primarily adjusts premiums based on driving behavior but does not offer the broad liability protection essential for safeguarding personal assets against large lawsuits.

On-Demand Insurance

Umbrella insurance provides broad, extra liability coverage beyond standard policies, protecting assets from large claims or lawsuits, while usage-based insurance offers flexible, on-demand premiums tied to actual driving behavior and usage, optimizing cost efficiency for low-mileage drivers. On-demand insurance leverages telematics data to deliver personalized coverage, making it an ideal choice for dynamic asset protection aligned with real-time risk assessment.

Risk-Based Usage Scoring

Umbrella insurance provides broad liability coverage that extends beyond standard policy limits to protect assets from major claims or lawsuits. Risk-based usage scoring in usage-based insurance evaluates driving behavior to adjust premiums, offering personalized rates that align with individual risk profiles for more precise asset protection.

Fleet Umbrella Endorsement

Fleet Umbrella Endorsement enhances Umbrella Insurance by providing extra liability coverage specifically tailored for commercial vehicle fleets, offering protection beyond the limits of underlying policies. Usage-Based Insurance leverages telematics data to customize premiums based on actual driving behavior, optimizing cost efficiency but typically lacking the broad, high-limit liability protection that fleet umbrella policies provide.

Dynamic Coverage Adjustment

Umbrella insurance provides a fixed, high-limit liability coverage that protects assets beyond standard policy limits, while usage-based insurance dynamically adjusts premiums and coverage based on real-time driving behavior and mileage. Dynamic coverage adjustment in usage-based insurance offers tailored protection and cost efficiency, whereas umbrella insurance ensures consistent, broad liability protection regardless of usage patterns.

Digital Umbrella Underwriting

Digital Umbrella Underwriting leverages real-time data analytics and telematics to enhance risk assessment accuracy for Umbrella Insurance, providing broader liability coverage beyond standard auto or home policies. Usage-Based Insurance focuses primarily on driving behavior but lacks the comprehensive asset protection umbrella policies offer, making digital underwriting a critical advancement for holistic asset safeguarding.

Umbrella Insurance vs Usage-Based Insurance for asset protection. Infographic