Homeowners insurance offers comprehensive protection backed by established insurers, covering property damage, liability, and personal belongings with standardized policies. Peer-to-peer home insurance leverages a community-based model where groups pool premiums to cover claims, often resulting in lower costs and increased transparency. Choosing between the two depends on risk tolerance, desire for personalized service, and preference for traditional versus innovative coverage structures.

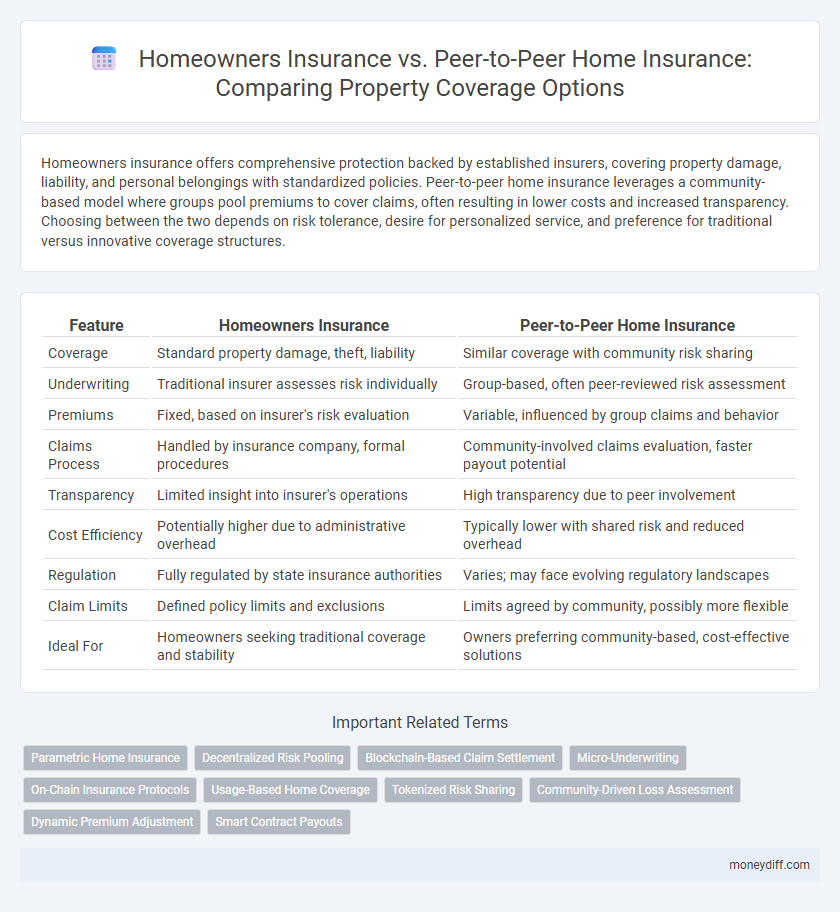

Table of Comparison

| Feature | Homeowners Insurance | Peer-to-Peer Home Insurance |

|---|---|---|

| Coverage | Standard property damage, theft, liability | Similar coverage with community risk sharing |

| Underwriting | Traditional insurer assesses risk individually | Group-based, often peer-reviewed risk assessment |

| Premiums | Fixed, based on insurer's risk evaluation | Variable, influenced by group claims and behavior |

| Claims Process | Handled by insurance company, formal procedures | Community-involved claims evaluation, faster payout potential |

| Transparency | Limited insight into insurer's operations | High transparency due to peer involvement |

| Cost Efficiency | Potentially higher due to administrative overhead | Typically lower with shared risk and reduced overhead |

| Regulation | Fully regulated by state insurance authorities | Varies; may face evolving regulatory landscapes |

| Claim Limits | Defined policy limits and exclusions | Limits agreed by community, possibly more flexible |

| Ideal For | Homeowners seeking traditional coverage and stability | Owners preferring community-based, cost-effective solutions |

Understanding Homeowners Insurance: Traditional Models

Traditional homeowners insurance provides a comprehensive policy backed by established insurance companies, offering coverage for property damage, theft, and liability risks. These policies involve fixed premiums, underwriting processes, and claims handled by licensed insurers, ensuring regulatory compliance and financial stability. Homeowners benefit from standardized protection with established claims procedures, though often at higher costs compared to alternative models.

What is Peer-to-Peer (P2P) Home Insurance?

Peer-to-Peer (P2P) Home Insurance is a decentralized insurance model where a group of homeowners pool their premiums to cover property damage collectively, reducing reliance on traditional insurance companies. This approach often results in lower costs and increased transparency, as claims are reviewed and paid out within the member community. P2P insurance emphasizes trust and shared responsibility, leveraging technology platforms to manage policies and expedite claims processing efficiently.

Key Differences Between Traditional and P2P Home Insurance

Traditional homeowners insurance relies on centralized insurance companies that pool premiums to cover claims, whereas peer-to-peer (P2P) home insurance utilizes a community-based model where policyholders share risks and claims directly. Traditional policies often include standardized coverage with set premiums and regulatory oversight, while P2P models typically offer more flexible, transparent terms and potential cost savings through reduced administrative fees. Claims processing in traditional insurance can involve longer wait times due to intermediary processes, whereas P2P insurance tends to expedite claims through collective decision-making and technology-driven platforms.

Coverage Comparison: Standard Policies vs P2P Options

Standard homeowners insurance policies typically provide comprehensive coverage including dwelling protection, personal property, liability, and additional living expenses, with set premiums and claim processes managed by established insurers. Peer-to-peer home insurance offers a decentralized model where policyholders pool funds for claims, potentially lowering costs and increasing transparency but often with limited coverage options and higher variability in claim settlements. Comparing both, traditional policies ensure predictable protection and regulatory oversight, while P2P models may appeal to risk-tolerant homeowners seeking community-driven solutions with flexible terms.

Cost Analysis: Premiums, Deductibles, and Fees

Homeowners insurance typically involves fixed premiums, standardized deductibles, and administrative fees set by insurers, resulting in predictable but sometimes higher overall costs. Peer-to-peer home insurance models often lower premiums and fees by pooling risks among members and reducing insurer overhead, though deductibles may vary based on group claims experience. Cost analysis reveals that P2P insurance can offer savings for low-risk properties but may expose homeowners to higher out-of-pocket expenses during high-claim periods.

Claim Processes: Traditional Insurers vs P2P Platforms

Traditional homeowners insurance claim processes typically involve formal assessments, extensive paperwork, and longer wait times due to regulatory compliance and third-party adjuster involvement. Peer-to-peer (P2P) home insurance platforms streamline claims by leveraging blockchain technology and community voting, resulting in faster payouts and enhanced transparency. Data shows that P2P claims can be resolved up to 30% quicker than conventional insurers, reducing customer friction and improving overall satisfaction.

Community Trust and Risk Sharing in P2P Insurance

Peer-to-peer (P2P) home insurance leverages community trust by pooling policyholders to share risks and claims, reducing reliance on traditional insurers. This model incentivizes responsible behavior, as members collectively manage and monitor risks, fostering transparency and mutual accountability. By distributing losses within the community, P2P insurance can lower premiums and offer tailored coverage aligned with the specific needs of homeowners.

Regulatory Considerations and Consumer Protections

Homeowners insurance operates under established regulatory frameworks that mandate minimum coverage standards, consumer protections, and claims handling processes enforced by state insurance departments. Peer-to-peer home insurance platforms often face varied regulations depending on jurisdiction, which can impact their licensing requirements and the extent of consumer safeguards such as dispute resolution mechanisms and financial solvency oversight. Consumers should evaluate regulatory compliance and protection features carefully when choosing between traditional homeowners insurance and peer-to-peer models to ensure adequate coverage and legal recourse.

Pros and Cons of Homeowners Insurance vs P2P Insurance

Homeowners insurance provides comprehensive coverage backed by established insurance companies, ensuring guaranteed claim payouts and financial stability but often comes with higher premiums and less personalization. Peer-to-peer (P2P) home insurance offers lower costs and increased transparency through collective risk-sharing among policyholders, though it may face challenges with liquidity and claim payment reliability during large-scale events. Choosing between traditional homeowners insurance and P2P models depends on priorities like cost-efficiency, claim security, and personalized coverage options.

How to Choose the Right Property Coverage for Your Needs

Selecting the right property coverage requires evaluating the extent of protection offered by homeowners insurance versus peer-to-peer home insurance, focusing on policy limits, premium costs, and claim processes. Homeowners insurance typically provides comprehensive coverage backed by established insurers and standardized claims support, while peer-to-peer models may offer competitive pricing and a community-driven approach to risk sharing. Assessing factors such as the value of your property, potential risks, and preferred customer service experience will help determine the optimal insurance solution tailored to your specific needs.

Related Important Terms

Parametric Home Insurance

Parametric home insurance offers a streamlined alternative to traditional homeowners insurance by providing fixed payouts based on predefined parameters such as wind speed or earthquake magnitude, reducing claim processing time and enhancing transparency. Unlike peer-to-peer home insurance, which pools member funds to cover losses, parametric policies rely on objective data triggers, delivering faster financial relief without the need for individual claim assessments.

Decentralized Risk Pooling

Decentralized risk pooling in peer-to-peer home insurance redistributes property coverage costs among a network of insured individuals, reducing reliance on traditional insurers and potentially lowering premiums. This model leverages blockchain technology to increase transparency and trust, contrasting with the centralized underwriting and claims process of conventional homeowners insurance.

Blockchain-Based Claim Settlement

Homeowners insurance typically relies on centralized processes for claim settlement, while peer-to-peer home insurance leverages blockchain technology to enable transparent, automated, and faster claim verification and payouts. Blockchain-based claim settlement reduces fraud, enhances trust among policyholders, and lowers administrative costs by using smart contracts for efficient property coverage management.

Micro-Underwriting

Micro-underwriting in homeowners insurance tailors risk assessment to individual properties and behaviors, enabling more precise premium calculations and personalized coverage. Peer-to-peer home insurance leverages micro-underwriting by pooling similar risk profiles, reducing administrative costs and potentially lowering premiums compared to traditional homeowners insurance.

On-Chain Insurance Protocols

On-chain insurance protocols revolutionize homeowners insurance by leveraging blockchain technology to enable peer-to-peer home insurance, eliminating traditional intermediaries and enhancing transparency, security, and claims processing efficiency. These decentralized platforms use smart contracts to automate coverage terms and payouts, providing cost-effective, customizable property protection compared to conventional insurance policies managed by centralized companies.

Usage-Based Home Coverage

Usage-based home coverage in homeowners insurance leverages data from smart home devices to tailor premiums and enhance risk assessment, while peer-to-peer home insurance pools premiums among policyholders, promoting transparency and potential cost savings through community-driven claims management. Both models utilize technology to optimize property protection, but usage-based insurance primarily focuses on individual behavior and risk, whereas peer-to-peer insurance emphasizes collective responsibility and shared benefits.

Tokenized Risk Sharing

Homeowners insurance typically involves traditional risk pools managed by large insurers, while peer-to-peer home insurance leverages blockchain technology for tokenized risk sharing, enabling policyholders to directly share and transfer risk via digital tokens. This decentralized model increases transparency, reduces administrative costs, and allows more personalized coverage by securely distributing claims and premiums among verified members.

Community-Driven Loss Assessment

Peer-to-peer home insurance leverages community-driven loss assessment, allowing policyholders to collectively evaluate claims, potentially reducing fraud and improving transparency compared to traditional homeowners insurance. This model fosters trust and faster claim resolutions by involving members directly in the decision-making process for property coverage disputes.

Dynamic Premium Adjustment

Homeowners insurance typically features fixed premiums based on initial risk assessments, while peer-to-peer home insurance employs dynamic premium adjustment by leveraging real-time data and group claims experience to lower costs and enhance transparency for policyholders. This adaptive pricing model helps mitigate fraud and aligns premiums more closely with actual risk, providing a more personalized and potentially cost-effective property coverage solution.

Smart Contract Payouts

Smart contract payouts in peer-to-peer home insurance automate claim settlements by executing predefined conditions on blockchain, reducing processing time and minimizing disputes compared to traditional homeowners insurance. This technology enhances transparency and efficiency by directly linking property coverage triggers to instant, trustless financial compensation.

Homeowners Insurance vs Peer-to-Peer Home Insurance for property coverage. Infographic