Employer-provided insurance benefits offer essential coverage with premiums often partially or fully paid by the employer, enhancing employee retention and financial security. Voluntary benefits allow employees to tailor their insurance plans by choosing additional coverage based on personal needs, typically paid through payroll deductions at group rates. Combining both options creates a comprehensive benefits package that maximizes protection while controlling costs.

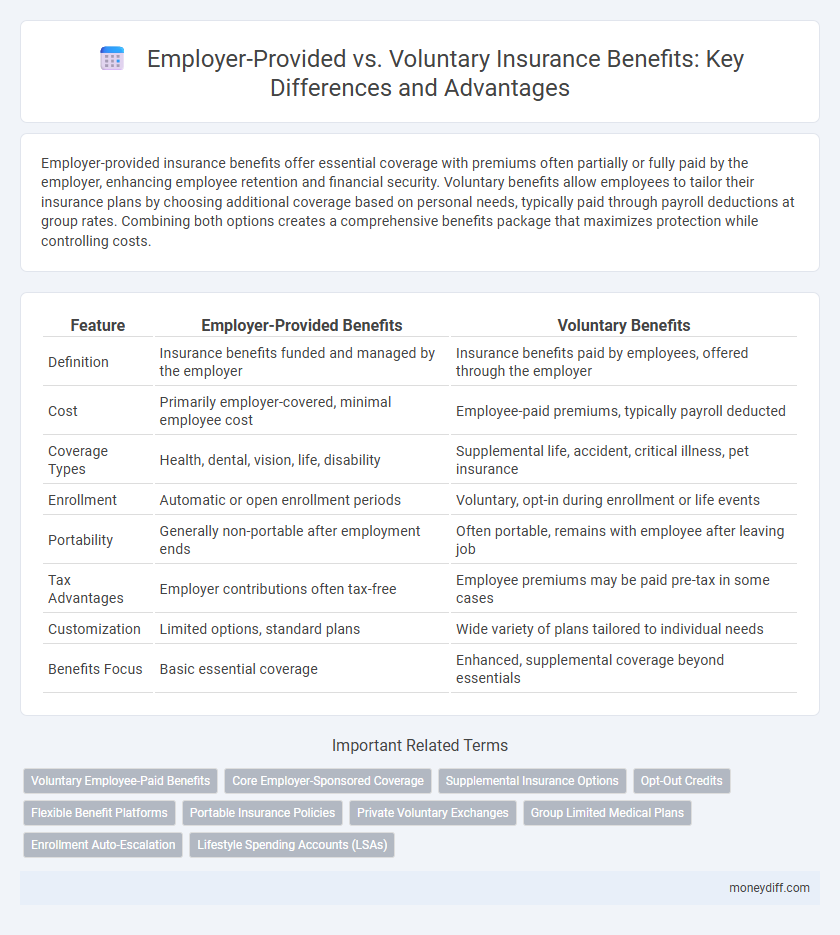

Table of Comparison

| Feature | Employer-Provided Benefits | Voluntary Benefits |

|---|---|---|

| Definition | Insurance benefits funded and managed by the employer | Insurance benefits paid by employees, offered through the employer |

| Cost | Primarily employer-covered, minimal employee cost | Employee-paid premiums, typically payroll deducted |

| Coverage Types | Health, dental, vision, life, disability | Supplemental life, accident, critical illness, pet insurance |

| Enrollment | Automatic or open enrollment periods | Voluntary, opt-in during enrollment or life events |

| Portability | Generally non-portable after employment ends | Often portable, remains with employee after leaving job |

| Tax Advantages | Employer contributions often tax-free | Employee premiums may be paid pre-tax in some cases |

| Customization | Limited options, standard plans | Wide variety of plans tailored to individual needs |

| Benefits Focus | Basic essential coverage | Enhanced, supplemental coverage beyond essentials |

Understanding Employer-Provided Insurance Benefits

Employer-provided insurance benefits typically include health, dental, vision, and life coverage negotiated as part of an employee compensation package, often offering lower premiums due to group rates. These benefits provide financial protection and access to essential healthcare services, promoting employee well-being and retention. Understanding eligibility requirements, coverage limits, and plan options is essential for maximizing the value of employer-provided insurance.

What Are Voluntary Insurance Benefits?

Voluntary insurance benefits refer to optional coverage plans offered by employers that employees can choose to purchase at their own expense, supplementing core employer-provided benefits. Common voluntary benefits include supplemental life insurance, disability insurance, critical illness coverage, and accident insurance, allowing employees to tailor protections to their individual needs. These benefits often come with group rates and payroll deductions, providing cost-effective options beyond basic employer-sponsored insurance.

Key Differences Between Employer-Provided and Voluntary Insurance

Employer-provided insurance typically offers comprehensive coverage funded wholly or partially by the employer, ensuring lower premiums and streamlined enrollment for employees. Voluntary insurance allows employees to select additional benefits tailored to individual needs, often paid entirely by the employee through payroll deductions, providing flexible and customizable protection. Key differences include cost-sharing, coverage scope, and enrollment processes, with employer-provided plans emphasizing group coverage advantages and voluntary plans focusing on personal choice and supplemental options.

Cost Comparison: Employer-Provided vs Voluntary Benefits

Employer-provided insurance benefits often feature lower premiums due to group rates negotiated by employers, reducing overall employee costs compared to voluntary benefits. Voluntary benefits typically carry higher out-of-pocket expenses because they are individually elected and risk-rated, leading to increased premiums without employer subsidies. Evaluating both options requires analyzing total cost of coverage, including premiums, deductibles, and potential tax advantages linked to employer-provided plans.

Coverage Flexibility: Which Is More Customizable?

Employer-provided insurance benefits typically offer standardized coverage packages designed to meet general workforce needs, limiting individual customization options. Voluntary benefits allow employees to tailor insurance plans more precisely to their personal circumstances, such as selecting specific coverage limits, riders, or additional protections like critical illness and accident insurance. This flexibility in voluntary benefits enhances employee satisfaction by addressing unique health risks and financial goals beyond the scope of employer plans.

Enrollment Processes: Employer-Provided vs Voluntary Insurance

Employer-provided insurance typically features automated enrollment through payroll systems, ensuring streamlined access with minimal employee effort. Voluntary insurance requires active employee enrollment, often involving separate applications and customized plan selections, which can lead to lower participation rates. Efficient communication and user-friendly digital platforms are crucial to increase voluntary benefits uptake during open enrollment periods.

Impact on Payroll and Taxes

Employer-provided benefits reduce taxable income by allowing premiums to be paid pre-tax, lowering payroll tax liabilities for both employers and employees. Voluntary benefits, often paid after-tax, increase payroll tax obligations since these premiums are not deducted pre-tax. Employers must carefully balance the tax advantages of employer-provided plans against the flexibility offered by voluntary benefits when designing compensation packages.

Employee Perspectives: Satisfaction and Utilization Rates

Employees typically report higher satisfaction and utilization rates with employer-provided insurance benefits due to lower premiums and automatic enrollment. Voluntary benefits often see lower participation because employees must actively opt in and cover full costs, leading to underutilization despite offering valuable coverage options. Understanding these patterns helps employers tailor benefit packages that maximize employee engagement and overall retention.

Employer Considerations in Offering Insurance Benefits

Employers must assess cost efficiency, employee preferences, and regulatory compliance when deciding between employer-provided and voluntary insurance benefits. Offering a blend of core employer-paid coverage with voluntary supplemental options can enhance workforce satisfaction while managing budget constraints. Effective communication about benefit choices helps optimize participation rates and ensures alignment with corporate wellness goals.

Making the Right Choice: Evaluating Your Insurance Options

Evaluating employer-provided versus voluntary benefits requires analyzing coverage scope, cost-sharing, and customization options to align with personal risk tolerance and financial goals. Employer-provided benefits typically offer standardized plans with group rates and partial premiums paid by the employer, enhancing affordability but limiting flexibility. Voluntary benefits allow tailored coverage beyond the core package, enabling employees to address specific needs such as supplemental life, disability, or accident insurance at employer-negotiated group rates but fully funded by the employee.

Related Important Terms

Voluntary Employee-Paid Benefits

Voluntary employee-paid benefits, such as supplemental life insurance, critical illness coverage, and accident protection, offer workers customizable financial security options that complement core employer-provided insurance plans. These benefits enable employees to tailor coverage based on personal needs, often with premium costs deducted directly from payroll, enhancing overall workforce satisfaction and financial well-being.

Core Employer-Sponsored Coverage

Core employer-sponsored coverage typically includes essential insurance benefits such as health, dental, and life insurance, provided directly by the employer and often partially subsidized. Voluntary benefits, in contrast, allow employees to customize their insurance with additional policies like disability or accident coverage, usually paid entirely by the employee through payroll deductions.

Supplemental Insurance Options

Employer-provided insurance benefits often include basic health, dental, and life coverage, while voluntary benefits offer supplemental insurance options such as critical illness, accident, and disability policies that employees can elect to tailor their protection. Supplemental insurance enhances overall financial security by covering out-of-pocket expenses and gaps left by primary employer-sponsored plans.

Opt-Out Credits

Opt-out credits incentivize employees to decline employer-provided insurance by offering a cash benefit, reducing overall company healthcare expenses. These credits enhance the attractiveness of voluntary benefits by providing flexibility and financial advantages tailored to individual employee needs.

Flexible Benefit Platforms

Flexible benefit platforms integrate both employer-provided and voluntary insurance benefits, allowing employees to customize coverage according to their individual needs while optimizing employer cost management. These platforms enhance employee satisfaction by enabling seamless selection of options such as health, dental, vision, and disability insurance within a unified digital interface.

Portable Insurance Policies

Employer-provided insurance policies typically offer limited portability, remaining active only while the employee stays with the company, whereas voluntary insurance benefits allow individuals to maintain coverage independently after leaving their employer. Portable insurance policies enhance long-term financial security by enabling employees to retain essential benefits such as life, disability, or health coverage regardless of job changes.

Private Voluntary Exchanges

Private voluntary exchanges enable employees to customize insurance benefits by choosing from a range of employer-offered and individual plans, enhancing flexibility beyond traditional employer-provided coverage. These platforms increase employee engagement and cost transparency while allowing employers to manage benefits budgets more effectively.

Group Limited Medical Plans

Group Limited Medical Plans offered as employer-provided benefits ensure predictable healthcare coverage with fixed costs and streamlined administration, enhancing financial security for employees. Voluntary benefits supplement these plans by allowing workers to customize additional coverage options, often at lower premiums, giving greater flexibility and personalized protection.

Enrollment Auto-Escalation

Enrollment auto-escalation in employer-provided insurance benefits ensures seamless premium adjustments aligned with plan upgrades, enhancing employee coverage without manual intervention. Voluntary benefits typically lack automatic enrollment features, requiring employees to actively opt-in, which may limit participation and overall utilization.

Lifestyle Spending Accounts (LSAs)

Employer-provided and voluntary benefits both play crucial roles in employee insurance coverage, with Lifestyle Spending Accounts (LSAs) emerging as a flexible option that allows employees to allocate funds toward personalized wellness and lifestyle expenses not typically covered by standard insurance plans. LSAs enable organizations to enhance employee satisfaction by offering tax-advantaged spending on activities such as fitness, mental health support, and family care, bridging gaps between traditional employer benefits and voluntary add-ons.

Employer-Provided vs Voluntary Benefits for insurance. Infographic