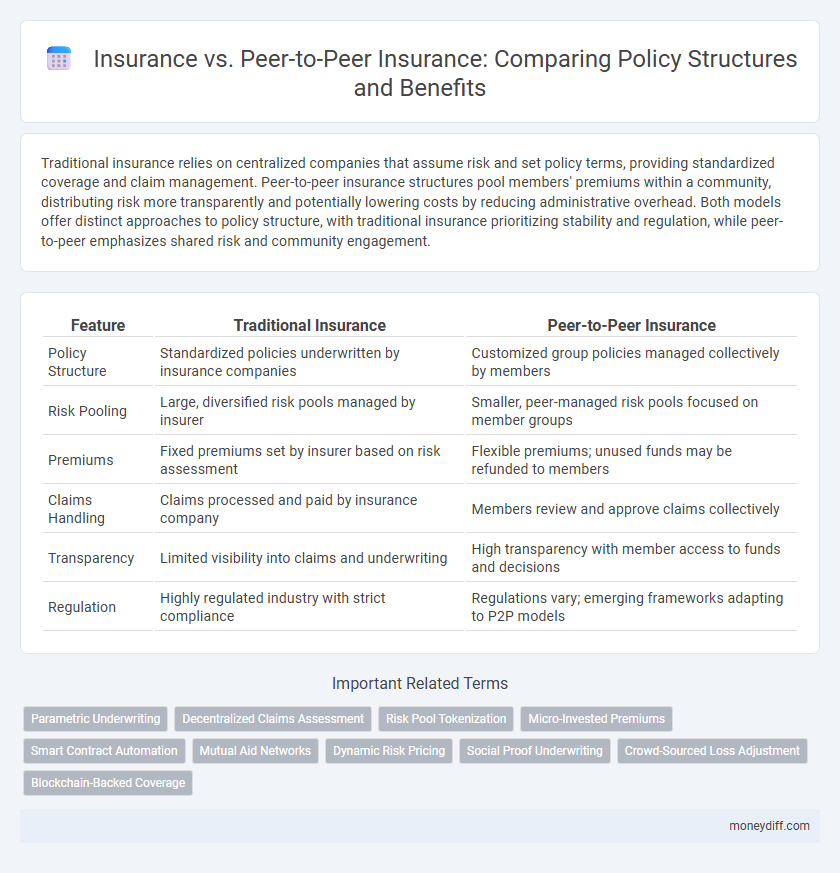

Traditional insurance relies on centralized companies that assume risk and set policy terms, providing standardized coverage and claim management. Peer-to-peer insurance structures pool members' premiums within a community, distributing risk more transparently and potentially lowering costs by reducing administrative overhead. Both models offer distinct approaches to policy structure, with traditional insurance prioritizing stability and regulation, while peer-to-peer emphasizes shared risk and community engagement.

Table of Comparison

| Feature | Traditional Insurance | Peer-to-Peer Insurance |

|---|---|---|

| Policy Structure | Standardized policies underwritten by insurance companies | Customized group policies managed collectively by members |

| Risk Pooling | Large, diversified risk pools managed by insurer | Smaller, peer-managed risk pools focused on member groups |

| Premiums | Fixed premiums set by insurer based on risk assessment | Flexible premiums; unused funds may be refunded to members |

| Claims Handling | Claims processed and paid by insurance company | Members review and approve claims collectively |

| Transparency | Limited visibility into claims and underwriting | High transparency with member access to funds and decisions |

| Regulation | Highly regulated industry with strict compliance | Regulations vary; emerging frameworks adapting to P2P models |

Introduction to Traditional Insurance and Peer-to-Peer Insurance

Traditional insurance typically involves a centralized company that pools premiums from policyholders to cover claims, providing structured risk management through underwriting and actuarial analysis. Peer-to-peer insurance, by contrast, decentralizes risk by grouping individuals with similar profiles who collectively fund claims, often leveraging technology platforms to enhance transparency and reduce costs. Both models offer distinct policy structures that influence coverage, premiums, and claims processing.

Key Differences in Policy Structures

Traditional insurance operates on a risk pooling system managed by centralized insurers who set policy terms, premiums, and claims processes, while peer-to-peer insurance relies on decentralized groups of members sharing risk directly and collaboratively. In peer-to-peer models, policies often feature transparent premium allocation and potential refunds when claims are low, contrasting with the fixed premium and claim settlements of traditional insurance. Policy structures in peer-to-peer insurance emphasize member governance and community risk sharing, whereas traditional policies enforce strict contractual obligations between insurer and insured.

Premium Collection and Distribution Mechanisms

Traditional insurance collects premiums centrally from policyholders, pooling funds into a large risk pool managed by the insurer, which redistributes claims payments based on individual losses backed by regulatory capital reserves. Peer-to-peer insurance structures premiums within smaller, decentralized groups, where members contribute funds that are directly used to pay claims within the group, often leveraging smart contracts or blockchain technology for transparent distribution. Premium collection in peer-to-peer models reduces administrative overhead and aligns incentives by returning unused funds to participants, contrasting with the fixed premium and claim payout system in traditional insurance.

Risk Pooling: Centralized vs Decentralized Models

Traditional insurance relies on a centralized risk pooling model where a single insurer pools premiums to cover claims, ensuring financial stability and regulatory oversight. Peer-to-peer insurance employs a decentralized model, grouping members with similar risk profiles to share losses directly, often reducing costs and increasing transparency. This shift in risk pooling impacts claim processing efficiency, premium pricing, and overall trust dynamics between insured parties.

Claims Process: Traditional vs Peer-to-Peer Approaches

Traditional insurance claims processes involve a centralized authority evaluating and approving claims, often leading to longer processing times and less transparency. Peer-to-peer insurance leverages decentralized groups where members collectively manage and validate claims, resulting in faster settlements and enhanced trust through shared responsibility. This shift in claims management optimizes cost-efficiency and reduces fraud risks by fostering community-based oversight.

Transparency and Policyholder Involvement

Traditional insurance relies on centralized policy structures where transparency is limited by complex contracts and opaque claims processes. Peer-to-peer insurance enhances transparency by allowing policyholders direct access to the pooling and claims data, promoting trust through collective decision-making. This model increases policyholder involvement by enabling members to participate in underwriting and claim approvals, aligning incentives and reducing conflicts of interest.

Policy Customization Options

Traditional insurance policies offer limited customization options, often providing standardized coverage plans that may not fully align with individual risk profiles. Peer-to-peer insurance leverages group dynamics to create more flexible and tailored policies by allowing members to select coverage levels and share risk among peers. This model enhances personalization by aligning policy terms directly with the specific needs and preferences of a smaller, more homogenous community.

Regulatory Frameworks and Compliance

Traditional insurance operates under strict regulatory frameworks designed to protect policyholders through standardized compliance requirements, including solvency margins and consumer protection laws. Peer-to-peer insurance models challenge these frameworks by decentralizing risk sharing among members, often navigating complex or evolving regulatory landscapes that lack clear guidelines. Compliance in peer-to-peer insurance requires innovative legal approaches to balance regulatory oversight with the benefits of community-based risk pooling.

Cost Implications for Policyholders

Traditional insurance typically involves fixed premiums paid to an insurer who assumes the risk, often leading to higher administrative costs and profit margins reflected in policyholder expenses. Peer-to-peer insurance pools premiums directly among members, reducing overhead and potentially lowering costs by minimizing middleman involvement. Cost implications for policyholders in peer-to-peer models include variable premiums based on group claims performance, which can result in savings but also exposure to fluctuating expenses.

Choosing the Right Insurance Policy Structure

Traditional insurance policies involve a central insurer underwriting risk and managing claims, offering stability through professional risk assessment and regulatory oversight. Peer-to-peer insurance organizes policyholders into groups that collectively share risks, reducing administrative costs and potentially lowering premiums by eliminating intermediaries. Selecting the right policy structure depends on individual risk tolerance, preference for community-based risk sharing, and the need for guaranteed claims payout versus cost efficiency.

Related Important Terms

Parametric Underwriting

Parametric underwriting in traditional insurance relies on predefined metrics and data triggers to streamline claim processing, whereas peer-to-peer insurance structures combine collective risk-sharing with parametric triggers to enhance transparency and reduce administrative costs. This model leverages blockchain and smart contracts to automate payouts based on real-time parameter conditions, optimizing efficiency and trust among policyholders.

Decentralized Claims Assessment

Decentralized claims assessment in peer-to-peer insurance leverages blockchain technology to enable transparent, community-driven evaluation processes, reducing fraud and increasing trust among members. Traditional insurance relies on centralized underwriters and adjusters, which can lead to slower claim resolutions and potential biases in decision-making.

Risk Pool Tokenization

Insurance traditionally relies on centralized risk pools managed by insurers, while peer-to-peer insurance uses blockchain technology to tokenize risk pools, enabling policyholders to directly share and trade risk exposure through digital tokens. Risk pool tokenization enhances transparency, reduces administrative costs, and aligns incentives by allowing participants to have ownership stakes and governance rights within decentralized insurance structures.

Micro-Invested Premiums

Traditional insurance pools premiums into large reserves managed by insurers, while peer-to-peer insurance structures micro-invested premiums within small, transparent groups, enhancing policyholder control and risk-sharing. This micro-investment approach promotes efficient capital allocation and incentivizes loss prevention by aligning individual interests with the collective financial outcome.

Smart Contract Automation

Traditional insurance relies on centralized policy structures managed by insurers, while peer-to-peer insurance utilizes decentralized groups with smart contract automation to streamline claims processing and premium distribution. Smart contracts enable automatic execution of policy terms, reducing administrative costs and enhancing transparency in peer-to-peer insurance models.

Mutual Aid Networks

Traditional insurance relies on centralized policy structures managed by corporations with fixed premiums and risk pools, while peer-to-peer insurance leverages mutual aid networks where members collectively share risks and reimburse claims directly. This decentralized model reduces administrative costs, fosters transparency, and enhances member control through blockchain-based smart contracts and community-driven decision-making.

Dynamic Risk Pricing

Traditional insurance relies on static risk pricing determined by actuaries, whereas peer-to-peer insurance implements dynamic risk pricing through real-time data and community risk pooling, enabling personalized premiums and more flexible policy structures. Dynamic risk pricing in peer-to-peer models enhances transparency and incentivizes risk reduction by aligning individual policyholder behavior with collective risk profiles.

Social Proof Underwriting

Traditional insurance relies on actuarial data and risk pools to structure policies, while peer-to-peer insurance leverages social proof underwriting by evaluating risk based on the reputation and behavior of individuals within a community. This approach enhances transparency and accountability, potentially reducing fraud and aligning premiums more closely with actual risk profiles.

Crowd-Sourced Loss Adjustment

Traditional insurance relies on centralized loss adjustment conducted by professional adjusters, whereas peer-to-peer insurance utilizes crowd-sourced loss adjustment, leveraging the collective judgment of policyholders to assess claims more transparently and reduce costs. Crowd-sourced loss adjustment enhances trust and efficiency by distributing claim validation responsibilities among group members, minimizing fraud and administrative expenses.

Blockchain-Backed Coverage

Blockchain-backed coverage in traditional insurance utilizes centralized policies managed by insurers, providing standardized risk assessment and claims processing, whereas peer-to-peer insurance leverages decentralized blockchain platforms to enable direct risk sharing among members, enhancing transparency and reducing administrative costs through smart contracts. The immutable ledger and automated claim verification inherent in blockchain strengthen trust and efficiency in both models but allow peer-to-peer structures to offer more flexible and community-driven policy customization.

Insurance vs Peer-to-Peer Insurance for policy structure. Infographic