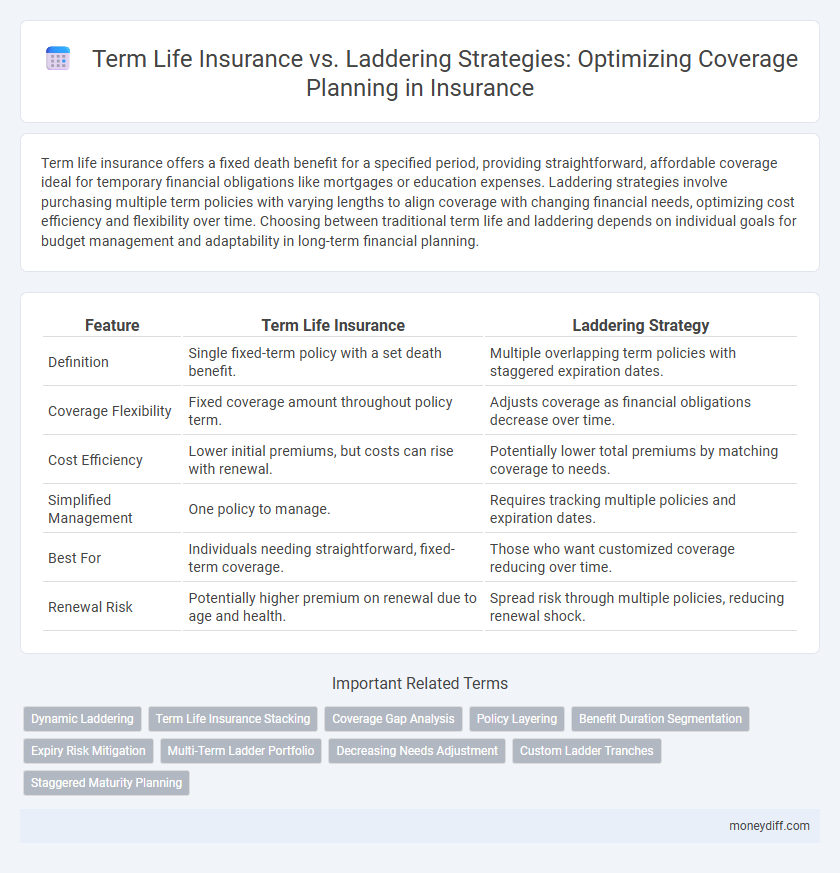

Term life insurance offers a fixed death benefit for a specified period, providing straightforward, affordable coverage ideal for temporary financial obligations like mortgages or education expenses. Laddering strategies involve purchasing multiple term policies with varying lengths to align coverage with changing financial needs, optimizing cost efficiency and flexibility over time. Choosing between traditional term life and laddering depends on individual goals for budget management and adaptability in long-term financial planning.

Table of Comparison

| Feature | Term Life Insurance | Laddering Strategy |

|---|---|---|

| Definition | Single fixed-term policy with a set death benefit. | Multiple overlapping term policies with staggered expiration dates. |

| Coverage Flexibility | Fixed coverage amount throughout policy term. | Adjusts coverage as financial obligations decrease over time. |

| Cost Efficiency | Lower initial premiums, but costs can rise with renewal. | Potentially lower total premiums by matching coverage to needs. |

| Simplified Management | One policy to manage. | Requires tracking multiple policies and expiration dates. |

| Best For | Individuals needing straightforward, fixed-term coverage. | Those who want customized coverage reducing over time. |

| Renewal Risk | Potentially higher premium on renewal due to age and health. | Spread risk through multiple policies, reducing renewal shock. |

Understanding Term Life Insurance: A Comprehensive Overview

Term life insurance provides a fixed death benefit for a specified period, making it a straightforward and cost-effective option for temporary coverage needs. Laddering strategies involve purchasing multiple term policies with varying durations to match changing financial obligations over time, optimizing affordability and coverage. Understanding the nuances of term life insurance policies and laddering can enhance protection by aligning coverage with life stages and financial goals.

What Is Laddering in Life Insurance Coverage?

Laddering in life insurance coverage involves purchasing multiple term life insurance policies with varying coverage amounts and expiration dates to align with different financial obligations over time. This strategy allows policyholders to reduce premiums as their coverage needs decrease, such as paying off a mortgage or funding children's education. By staggering policy terms, laddering offers a flexible and cost-effective approach compared to a single large term life insurance policy.

Key Differences: Term Life Insurance vs Laddering Strategies

Term Life Insurance offers a fixed death benefit amount and premium for a specified period, providing straightforward, predictable coverage suitable for income replacement or debt protection. Laddering Strategies involve purchasing multiple term policies with varying coverage amounts and expiration dates, allowing coverage to decrease over time in line with changing financial obligations. This approach enhances flexibility and cost efficiency by aligning insurance protection with evolving needs such as mortgage payoff or children's education expenses.

Benefits of Term Life Insurance for Long-Term Planning

Term life insurance offers predictable, fixed premiums and guaranteed coverage for a specified period, making it a cost-effective solution for long-term financial planning. It provides substantial death benefits to protect beneficiaries from economic hardships, supporting mortgage payments, education costs, and income replacement. Laddering strategies, while flexible, often result in higher overall premiums, whereas term life insurance delivers consistent protection aligned with stable financial goals.

How Laddering Life Insurance Policies Works

Laddering life insurance policies involves purchasing multiple term life insurance policies with varying coverage amounts and expiration dates to match changing financial needs over time. This strategy provides cost efficiency by allowing coverage to decrease as debts are paid off and income replacement needs decline. It enhances flexibility in coverage planning compared to a single level-term policy by aligning insurance protection directly with evolving financial obligations.

Cost Comparison: Term Life Insurance vs Laddering Coverage

Term life insurance offers predictable, fixed premiums for a specific coverage period, making it cost-effective for straightforward protection needs. Laddering coverage involves multiple term policies with staggered expiration dates and varied face amounts, which can optimize premium costs by aligning coverage with changing financial responsibilities over time. Comparing costs, laddering strategies often reduce overall premiums for long-term planning, while single term policies provide simplicity and initial affordability.

Flexibility and Customization with Laddered Strategies

Laddering strategies in term life insurance provide enhanced flexibility by allowing policyholders to stagger coverage amounts and expiration dates, aligning protection with changing financial needs over time. This customization helps optimize premiums and ensures coverage adjusts to milestones such as mortgage payoff or child-rearing expenses. Compared to single-term policies, laddered insurance offers a tailored approach that adapts to evolving risk profiles and financial goals.

Risk Management: Minimizing Gaps in Coverage

Term life insurance offers a defined protection period with fixed coverage amounts, ensuring predictable premiums and straightforward policy management. Laddering strategies involve purchasing multiple term policies with staggered expiration dates and varied coverage levels, aligning insurance protection with changing financial obligations over time. Employing laddering minimizes gaps in coverage by providing tailored risk management that adapts to evolving needs such as mortgage payoff, college expenses, and income replacement.

Who Should Consider Laddering Over Traditional Term Insurance?

Laddering strategies suit individuals seeking flexible coverage that adapts to changing financial obligations, such as growing families or fluctuating debts. Those with varying income streams or planned large expenses benefit from adjusting insurance amounts over time, optimizing premium costs. Policyholders aiming to align coverage with specific life stages avoid paying for unnecessary protection inherent in traditional term life insurance.

Choosing the Right Coverage Approach for Your Financial Goals

Term life insurance provides a fixed coverage amount for a set period, ideal for covering specific financial obligations like mortgages or education expenses. Laddering strategies involve purchasing multiple term policies with varying maturities, allowing coverage to decrease as financial responsibilities diminish over time. Selecting between these approaches depends on aligning the insurance plan with long-term financial goals, risk tolerance, and changing coverage needs.

Related Important Terms

Dynamic Laddering

Dynamic laddering in term life insurance optimizes coverage by adjusting policy amounts and durations to match changing financial responsibilities, providing flexible protection that decreases as debts and dependents diminish. This strategy enhances cost-efficiency and ensures continuous, tailored risk management compared to static term policies, aligning insurance coverage with evolving life stages and financial goals.

Term Life Insurance Stacking

Term life insurance stacking involves purchasing multiple term life policies with overlapping terms to maximize coverage while managing premiums effectively, offering flexibility as financial needs evolve. This strategy contrasts with traditional laddering, which staggers policy expirations to align coverage amounts with decreasing liabilities over time, potentially resulting in gaps or increased costs.

Coverage Gap Analysis

Term life insurance provides a fixed death benefit for a specified period, often resulting in coverage gaps as needs change over time. Laddering strategies mitigate these gaps by aligning multiple policies with decreasing coverage amounts, ensuring continuous protection tailored to evolving financial obligations and minimizing periods without sufficient coverage.

Policy Layering

Policy layering in term life insurance involves using multiple policies with varying coverage amounts and durations to optimize protection and cost-efficiency, aligning coverage with changing financial needs over time. Laddering strategies apply this concept by sequentially reducing coverage as obligations decrease, providing tailored support through different life stages while minimizing premiums.

Benefit Duration Segmentation

Term life insurance offers fixed coverage for a specified period, providing a straightforward benefit duration ideal for covering financial obligations like mortgages or education costs. Laddering strategies segment coverage into multiple policy terms with staggered expiration dates, optimizing benefit duration by aligning insurance protection with evolving financial responsibilities.

Expiry Risk Mitigation

Term life insurance provides a fixed coverage amount for a specified period, exposing policyholders to expiry risk if their needs outlast the term. Laddering strategies mitigate expiry risk by staggering multiple term policies with overlapping terms, ensuring continuous coverage tailored to changing financial obligations over time.

Multi-Term Ladder Portfolio

A Multi-Term Ladder Portfolio leverages multiple term life insurance policies with staggered expiration dates to optimize coverage and manage premium costs over time. This laddering strategy enhances financial flexibility by aligning insurance protection with evolving life stages and financial obligations, reducing the risk of coverage gaps compared to single-term policies.

Decreasing Needs Adjustment

Term life insurance offers a fixed coverage amount for a specified period, making it suitable for covering temporary financial obligations, while laddering strategies involve purchasing multiple policies with staggered maturity dates to match decreasing needs over time. This decreasing needs adjustment aligns insurance coverage with the gradual reduction of debt and financial responsibilities, optimizing premium costs and ensuring adequate protection throughout different life stages.

Custom Ladder Tranches

Custom ladder tranches in term life insurance enable tailored coverage periods that align with specific financial obligations and life stages, optimizing premium costs and benefits. This strategy enhances flexibility by dividing term coverage into multiple, staggered segments, ensuring protection adapts as needs decrease or shift over time.

Staggered Maturity Planning

Term life insurance with laddering strategies enables staggered maturity planning by purchasing multiple policies with different expiration dates, ensuring coverage aligns with changing financial needs over time while potentially reducing overall premiums. This approach provides flexibility and targeted protection during key life stages such as mortgage payoff, child-rearing expenses, and retirement planning.

Term Life Insurance vs Laddering Strategies for coverage planning. Infographic