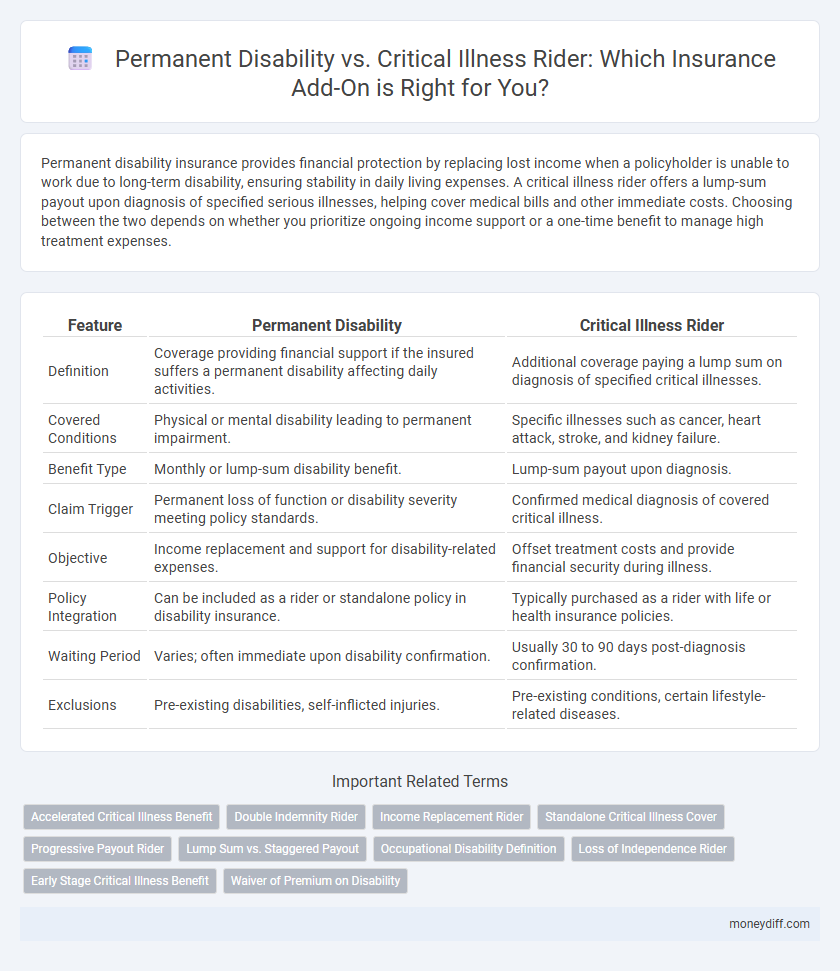

Permanent disability insurance provides financial protection by replacing lost income when a policyholder is unable to work due to long-term disability, ensuring stability in daily living expenses. A critical illness rider offers a lump-sum payout upon diagnosis of specified serious illnesses, helping cover medical bills and other immediate costs. Choosing between the two depends on whether you prioritize ongoing income support or a one-time benefit to manage high treatment expenses.

Table of Comparison

| Feature | Permanent Disability | Critical Illness Rider |

|---|---|---|

| Definition | Coverage providing financial support if the insured suffers a permanent disability affecting daily activities. | Additional coverage paying a lump sum on diagnosis of specified critical illnesses. |

| Covered Conditions | Physical or mental disability leading to permanent impairment. | Specific illnesses such as cancer, heart attack, stroke, and kidney failure. |

| Benefit Type | Monthly or lump-sum disability benefit. | Lump-sum payout upon diagnosis. |

| Claim Trigger | Permanent loss of function or disability severity meeting policy standards. | Confirmed medical diagnosis of covered critical illness. |

| Objective | Income replacement and support for disability-related expenses. | Offset treatment costs and provide financial security during illness. |

| Policy Integration | Can be included as a rider or standalone policy in disability insurance. | Typically purchased as a rider with life or health insurance policies. |

| Waiting Period | Varies; often immediate upon disability confirmation. | Usually 30 to 90 days post-diagnosis confirmation. |

| Exclusions | Pre-existing disabilities, self-inflicted injuries. | Pre-existing conditions, certain lifestyle-related diseases. |

Understanding Permanent Disability and Critical Illness Riders

Permanent Disability riders provide financial protection by offering a lump sum or regular payments if the insured suffers a disability that limits their ability to work permanently. Critical Illness riders cover specific serious illnesses such as cancer, stroke, or heart attack, paying out a benefit upon diagnosis to help with medical and living expenses. Understanding the coverage, exclusions, and claim conditions of each rider is essential for choosing the right policy to meet individual health and financial needs.

Key Differences Between Permanent Disability and Critical Illness Riders

Permanent disability riders provide coverage when a policyholder suffers long-term impairment affecting their ability to work, offering financial support proportional to the disability severity. Critical illness riders pay a lump sum upon diagnosis of specified serious illnesses such as cancer, heart attack, or stroke, enabling policyholders to manage medical expenses and other financial burdens. The main difference lies in the trigger event: permanent disability riders focus on functional impairment and loss of earning capacity, while critical illness riders are based on the diagnosis of specific life-threatening conditions.

Coverage Scope: Disability vs Critical Illness

Permanent Disability riders primarily provide coverage for long-term or total loss of physical or mental functions resulting from an accident or illness, ensuring financial support when the insured cannot work. Critical Illness riders cover a specific list of serious medical conditions such as cancer, stroke, or heart attack, offering a lump sum payout upon diagnosis to help manage treatment costs. The key difference lies in the coverage scope: Permanent Disability focuses on functional impairment impacting earning capacity, while Critical Illness addresses early financial relief for defined severe diseases.

Eligibility Criteria for Each Rider

Permanent disability riders typically require the insured to have a documented permanent loss of function or impairment affecting daily activities, as defined by medical assessments and insurer-specific guidelines. Critical illness riders usually demand a confirmed diagnosis of a covered critical condition such as cancer, stroke, or heart attack, with eligibility varying based on the severity and stage of the illness. Both riders require policyholders to meet age limits and health screening criteria established by the insurer to qualify for coverage.

Payout Structures and Claim Processes

Permanent Disability riders typically offer structured payouts based on the severity and classification of the disability, often disbursed as lump sums or scheduled installments tied to medical assessments. Critical Illness riders provide lump sum payments upon diagnosis of covered illnesses, with claim approval relying heavily on documented medical proofs and specified disease criteria. Understanding the differing claim processes and payout triggers ensures better alignment with individual financial protection needs in insurance planning.

Cost Comparison: Premiums and Affordability

Permanent disability riders generally have higher premiums due to the broad coverage they provide, including loss of limbs, paralysis, and total disability. Critical illness riders tend to be more affordable as they cover specific illnesses like cancer, stroke, and heart attack, limiting payout scenarios. Premium costs for both riders vary by age, health status, and coverage amount, with critical illness riders often preferred for budget-conscious policyholders seeking targeted protection.

Pros and Cons of Permanent Disability Rider

Permanent Disability Riders offer comprehensive coverage for individuals unable to work due to long-term disability, ensuring consistent income replacement and financial stability. However, these riders often come with higher premiums and may have strict definitions of disability, limiting eligibility for benefits. Despite these drawbacks, they provide critical protection against loss of earning capacity that critical illness riders may not fully address.

Advantages and Limitations of Critical Illness Rider

The Critical Illness Rider provides a lump sum benefit upon diagnosis of specified severe illnesses, offering immediate financial support for treatment and recovery expenses. It covers conditions such as cancer, heart attack, and stroke, enabling policyholders to manage high medical costs and loss of income more effectively. However, the rider's limitations include a predefined list of covered illnesses, potential exclusions, and waiting periods before benefits become payable, which may restrict its applicability compared to broader disability coverage.

Choosing the Right Rider for Your Financial Needs

Choosing the right insurance rider depends on your specific financial goals and risk tolerance. Permanent Disability riders provide coverage for long-term or total disability that impairs your ability to work, offering sustained financial support. Critical Illness riders deliver a lump-sum payment upon diagnosis of specified illnesses, helping cover immediate medical expenses and recovery costs.

Expert Tips for Integrating Riders into Your Insurance Plan

Consult with a licensed insurance advisor to assess your specific health risks and financial needs when choosing between a Permanent Disability and a Critical Illness Rider. Prioritize riders that complement your base policy by covering significant gaps without overlapping benefits, ensuring comprehensive protection. Regularly review and update your insurance plan to incorporate riders that adapt to changes in medical advancements and your personal circumstances.

Related Important Terms

Accelerated Critical Illness Benefit

The Accelerated Critical Illness Benefit allows policyholders to receive a portion of their life insurance payout upon diagnosis of a covered critical illness, providing immediate financial support without waiting for permanent disability confirmation. This rider contrasts with Permanent Disability coverage, which typically disburses benefits only after long-term disability assessment, making the Accelerated Critical Illness Benefit ideal for managing urgent medical expenses and recovery costs.

Double Indemnity Rider

The Double Indemnity Rider enhances permanent disability and critical illness coverage by providing twice the benefit in cases of accidental death or disability, significantly increasing financial protection for policyholders. This rider is especially valuable for individuals seeking comprehensive risk management beyond standard disability and illness benefits within their insurance plans.

Income Replacement Rider

A Permanent Disability Rider provides long-term income replacement if a policyholder suffers a disabling injury or condition that limits their ability to work permanently. In contrast, a Critical Illness Rider offers a lump-sum payment upon diagnosis of specified serious illnesses, which may supplement income but does not guarantee ongoing income replacement.

Standalone Critical Illness Cover

Standalone Critical Illness cover provides targeted financial protection by paying a lump sum upon diagnosis of specified serious illnesses, whereas Permanent Disability rider offers benefits only when disability results in total and permanent loss of earning capacity. Choosing Standalone Critical Illness insurance ensures broader coverage for multiple critical conditions without relying on disability occurrence, optimizing policyholder security.

Progressive Payout Rider

A Progressive Payout Rider enhances insurance coverage by providing incremental benefits over time for policyholders with Permanent Disability or Critical Illness, ensuring sustained financial support as conditions evolve. This rider differs from lump-sum payments by offering scheduled payouts linked to recovery stages or worsening health, optimizing long-term financial stability.

Lump Sum vs. Staggered Payout

Permanent Disability insurance provides a lump sum payout upon confirmation of disability, offering immediate financial support to cover long-term care and living expenses. Critical Illness riders typically deliver staggered payouts based on diagnosis severity and treatment milestones, enabling ongoing assistance aligned with recovery phases and medical costs.

Occupational Disability Definition

Occupational disability in insurance refers to the insured's inability to perform the essential duties of their specific occupation due to injury or illness, impacting the claim eligibility under a permanent disability or critical illness rider. Permanent disability riders typically cover long-term or permanent loss of occupational function, while critical illness riders provide benefits upon diagnosis of specified severe conditions, regardless of occupational impact.

Loss of Independence Rider

The Loss of Independence Rider in insurance policies provides financial support when a policyholder can no longer perform daily activities independently due to permanent disability, ensuring coverage tailored to long-term care needs. Unlike Critical Illness Riders, which pay out upon diagnosis of specific illnesses, the Loss of Independence Rider focuses on the sustained impact on quality of life and autonomy.

Early Stage Critical Illness Benefit

Early Stage Critical Illness Benefit in insurance provides financial support soon after diagnosis of specified illnesses, offering quicker access to funds compared to Permanent Disability coverage. This rider enhances policies by covering conditions at an initial stage, helping policyholders manage medical expenses before disabilities become permanent.

Waiver of Premium on Disability

A Waiver of Premium rider in insurance automatically suspends premium payments if the policyholder becomes permanently disabled, ensuring coverage continuity without financial burden. Unlike Critical Illness riders that pay a lump sum after diagnosis, this rider specifically protects against the inability to pay premiums due to long-term disability, maintaining policy benefits uninterrupted.

Permanent Disability vs Critical Illness Rider for insurance. Infographic