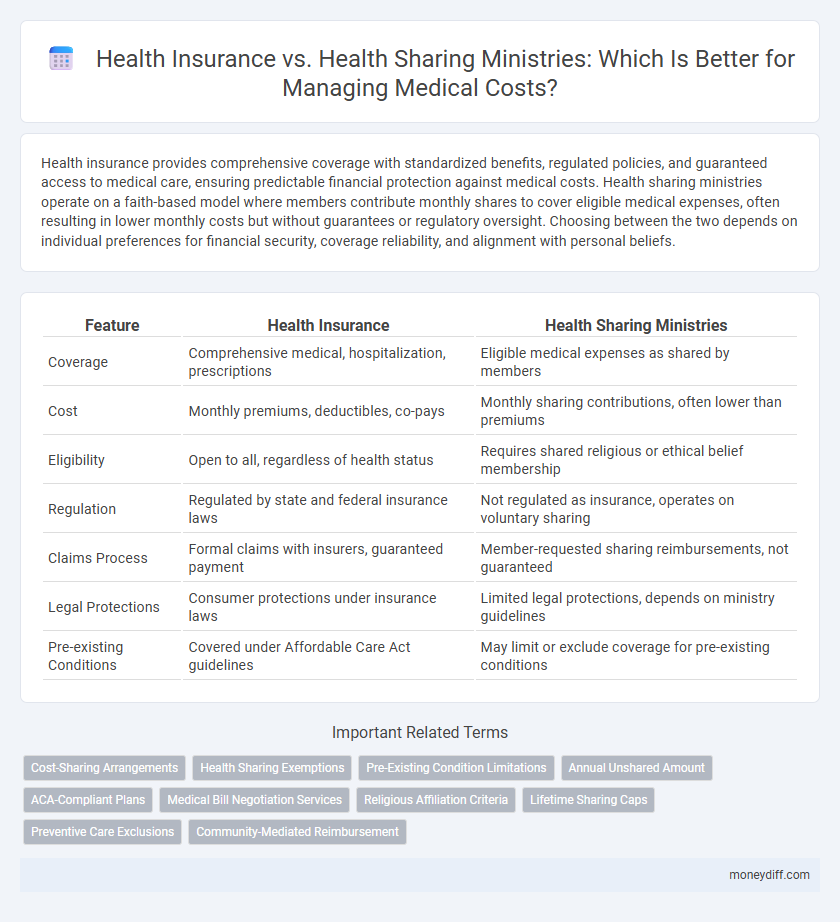

Health insurance provides comprehensive coverage with standardized benefits, regulated policies, and guaranteed access to medical care, ensuring predictable financial protection against medical costs. Health sharing ministries operate on a faith-based model where members contribute monthly shares to cover eligible medical expenses, often resulting in lower monthly costs but without guarantees or regulatory oversight. Choosing between the two depends on individual preferences for financial security, coverage reliability, and alignment with personal beliefs.

Table of Comparison

| Feature | Health Insurance | Health Sharing Ministries |

|---|---|---|

| Coverage | Comprehensive medical, hospitalization, prescriptions | Eligible medical expenses as shared by members |

| Cost | Monthly premiums, deductibles, co-pays | Monthly sharing contributions, often lower than premiums |

| Eligibility | Open to all, regardless of health status | Requires shared religious or ethical belief membership |

| Regulation | Regulated by state and federal insurance laws | Not regulated as insurance, operates on voluntary sharing |

| Claims Process | Formal claims with insurers, guaranteed payment | Member-requested sharing reimbursements, not guaranteed |

| Legal Protections | Consumer protections under insurance laws | Limited legal protections, depends on ministry guidelines |

| Pre-existing Conditions | Covered under Affordable Care Act guidelines | May limit or exclude coverage for pre-existing conditions |

Understanding Health Insurance: Key Features

Health insurance provides comprehensive coverage for medical expenses, including doctor visits, hospital stays, prescription drugs, and preventive care, with premiums, deductibles, copayments, and coinsurance shaping out-of-pocket costs. Plans typically comply with the Affordable Care Act, guaranteeing essential health benefits and protections against pre-existing condition exclusions. Health insurance networks and provider choices directly impact access to care and overall cost efficiency for policyholders.

What Are Health Sharing Ministries?

Health Sharing Ministries are organizations where members share medical expenses based on common religious or ethical beliefs, rather than traditional insurance models. These ministries facilitate voluntary contributions from members to cover each other's eligible healthcare costs, often excluding coverage for pre-existing conditions or certain medical procedures. Unlike conventional health insurance regulated by government standards, Health Sharing Ministries operate under a faith-based agreement without guaranteeing payment, making them a distinct alternative for medical cost-sharing.

Cost Comparison: Premiums, Sharing, and Out-of-Pocket Expenses

Health insurance typically involves monthly premiums averaging $456 per person, along with copayments, deductibles, and coinsurance that vary based on plan type and coverage level. Health sharing ministries often require lower monthly contributions, ranging from $100 to $300, but members share medical costs directly within the community, which may lead to unpredictable out-of-pocket expenses. While health insurance offers more predictable costs and broader provider access, health sharing ministries can reduce upfront costs but carry higher financial risk during major medical events.

Coverage Differences: Services and Exclusions

Health insurance typically offers comprehensive coverage including preventive care, emergency services, prescription drugs, and specialist visits, with clearly defined exclusions and regulatory protections. Health Sharing Ministries often exclude coverage for pre-existing conditions, mental health services, and reproductive health, relying on member contributions rather than guaranteed payments. Understanding these coverage differences is crucial for selecting a plan that aligns with individual medical needs and financial expectations.

Eligibility Requirements and Membership Criteria

Health insurance typically requires applicants to meet standardized eligibility criteria such as residency, age, and sometimes employment status, with coverage available regardless of pre-existing conditions. Health Sharing Ministries often require members to adhere to specific religious beliefs or lifestyles and enforce moral or behavioral guidelines as part of their membership criteria. While health insurance is regulated by government agencies ensuring compliance and consumer protections, Health Sharing Ministries operate on voluntary participation without guaranteed coverage, making eligibility and membership significantly more restrictive.

Claims Process: How Payments and Reimbursements Work

Health insurance involves a structured claims process where policyholders submit medical bills to their insurer for direct payment or reimbursement based on covered services and deductible fulfillment. Health Sharing Ministries operate on a peer-to-peer model where members share medical expenses directly, often requiring upfront payment by the patient before submitting documentation for sharing contributions from the community. Insurance claims typically guarantee payment according to policy terms, while Health Sharing Ministries depend on member contributions and may have limits or exclusions impacting reimbursement reliability.

Legal Protections and Regulatory Oversight

Health insurance offers comprehensive legal protections and is regulated by state and federal agencies such as the Affordable Care Act, ensuring consumer rights and coverage standards. Health Sharing Ministries operate on a faith-based model without the same regulatory oversight, lacking guarantees for cost-sharing and minimal legal recourse if payments are denied. Consumers choosing Health Sharing Ministries face greater risk due to limited consumer protection laws and absent insurance mandates.

Tax Implications of Health Insurance vs Health Sharing

Health insurance premiums are often tax-deductible when meeting IRS requirements, providing a direct financial benefit, whereas contributions to Health Sharing Ministries typically lack tax-deductible status, classifying them as personal expenses. Medical expenses paid through Health Sharing Ministries generally do not qualify for tax deductions, unlike qualified medical expenses incurred under traditional health insurance plans. Understanding the tax treatment of premiums and medical payments is essential for optimizing healthcare cost management and compliance with IRS regulations.

Flexibility and Portability: Switching or Canceling Plans

Health insurance offers greater flexibility and portability, allowing policyholders to switch plans or cancel coverage without significant penalties, facilitating adaptation to changing healthcare needs or relocation. Health Sharing Ministries often have restrictive membership rules and limited portability, potentially complicating plan changes or discontinuation due to faith-based requirements and group-specific agreements. Understanding the flexibility and portability differences is essential for individuals seeking customizable and transferable medical cost solutions.

Assessing Risk: Which Option Suits Your Financial Goals?

Health insurance offers predictable premium payments and regulated coverage, reducing financial risk by covering a broad range of medical expenses, including emergencies and chronic conditions. Health sharing ministries, while often more affordable, involve variable monthly contributions and lack guaranteed coverage, potentially exposing members to higher out-of-pocket costs during major medical events. Evaluating personal risk tolerance, medical needs, and financial stability helps determine whether the structured security of health insurance or the cost-sharing flexibility of ministries aligns better with long-term financial goals.

Related Important Terms

Cost-Sharing Arrangements

Health insurance requires monthly premiums and cost-sharing through deductibles, copayments, and coinsurance, providing regulated financial protection and guarantees coverage for pre-existing conditions. Health Sharing Ministries operate on voluntary cost-sharing arrangements among members to cover medical expenses, often resulting in lower upfront costs but lacking guarantees, standardized benefits, and legal protections found in traditional health insurance.

Health Sharing Exemptions

Health Sharing Ministries offer a cost-effective alternative to traditional health insurance by allowing members to share medical expenses through a faith-based community, often qualifying for Health Sharing Exemptions under the Affordable Care Act. These exemptions protect members from the individual mandate penalty while providing access to healthcare cost-sharing programs aligned with their religious beliefs.

Pre-Existing Condition Limitations

Health insurance plans typically cover pre-existing conditions without limitations after a waiting period mandated by the Affordable Care Act, ensuring comprehensive protection regardless of medical history. Health sharing ministries often exclude or limit coverage for pre-existing conditions, requiring members to meet specific criteria or waiting periods before eligible medical expenses related to these conditions are shared.

Annual Unshared Amount

Health insurance typically requires an annual deductible or out-of-pocket maximum, while health sharing ministries often have an Annual Unshared Amount, a fixed sum members pay before eligible medical costs are shared among the community. Understanding the specific Annual Unshared Amount is crucial for comparing potential expenses, as it directly impacts how much individuals will pay before assistance with medical bills begins.

ACA-Compliant Plans

ACA-compliant health insurance plans are regulated under the Affordable Care Act, providing guaranteed coverage for pre-existing conditions, essential health benefits, and access to subsidies based on income. Health Sharing Ministries, while offering a faith-based alternative to traditional insurance, are not ACA-compliant and typically lack coverage guarantees, comprehensive benefits, and consumer protections mandated by federal law.

Medical Bill Negotiation Services

Health insurance rarely includes dedicated medical bill negotiation services, often leaving patients to handle costly bills independently, while many health sharing ministries actively negotiate medical expenses as part of their cost-saving approach. These ministries leverage collective member contributions to reduce out-of-pocket costs through direct bill negotiations, offering an alternative that can significantly lower medical costs compared to traditional insurance.

Religious Affiliation Criteria

Health insurance provides coverage regardless of religious beliefs, while Health Sharing Ministries require members to adhere to specific religious affiliations and lifestyle guidelines to participate in shared medical cost programs. These ministries operate on the principle of faith-based community financial support, limiting membership to those aligned with their doctrinal standards.

Lifetime Sharing Caps

Health Insurance policies typically offer unlimited lifetime coverage, ensuring continuous protection against medical costs, whereas Health Sharing Ministries impose lifetime sharing caps that restrict the total amount members can share, potentially leaving significant expenses uncovered. Understanding these caps is crucial for individuals comparing long-term financial security and medical cost responsibility between these two healthcare funding options.

Preventive Care Exclusions

Health insurance plans generally cover a wide range of preventive care services such as vaccinations, screenings, and annual check-ups, aligning with Affordable Care Act mandates. In contrast, Health Sharing Ministries often exclude preventive care from their shared expenses, focusing primarily on acute medical bills rather than routine health maintenance.

Community-Mediated Reimbursement

Health Sharing Ministries facilitate community-mediated reimbursement by pooling member contributions to cover medical expenses, differing from traditional health insurance which relies on risk pooling and regulatory frameworks. These ministries often emphasize shared beliefs and voluntary contributions, offering an alternative approach for managing healthcare costs without the legal obligations of insurance policies.

Health Insurance vs Health Sharing Ministries for medical costs. Infographic