Long-term care (LTC) insurance offers dedicated coverage specifically for extended care services, providing predictable benefits for nursing home, home health, or assisted living expenses. Hybrid life-LTC policies combine life insurance with long-term care benefits, allowing policyholders to access LTC funds while providing a death benefit if care is not needed. Choosing between traditional LTC insurance and hybrid policies depends on factors such as premium costs, benefit flexibility, and the desire for a death benefit alongside care coverage.

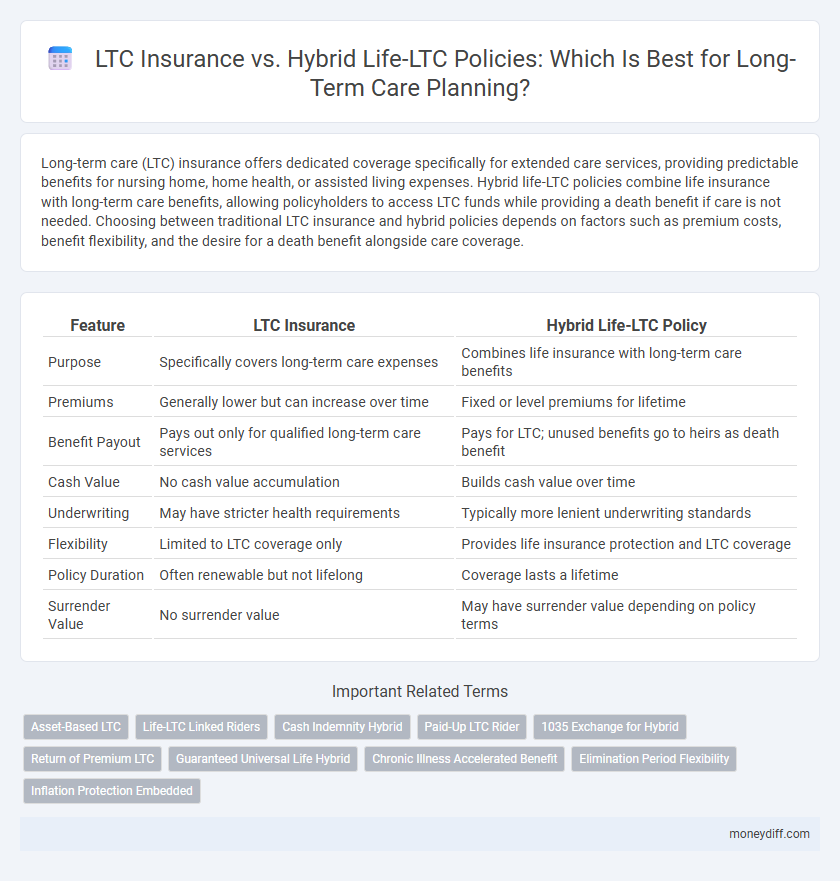

Table of Comparison

| Feature | LTC Insurance | Hybrid Life-LTC Policy |

|---|---|---|

| Purpose | Specifically covers long-term care expenses | Combines life insurance with long-term care benefits |

| Premiums | Generally lower but can increase over time | Fixed or level premiums for lifetime |

| Benefit Payout | Pays out only for qualified long-term care services | Pays for LTC; unused benefits go to heirs as death benefit |

| Cash Value | No cash value accumulation | Builds cash value over time |

| Underwriting | May have stricter health requirements | Typically more lenient underwriting standards |

| Flexibility | Limited to LTC coverage only | Provides life insurance protection and LTC coverage |

| Policy Duration | Often renewable but not lifelong | Coverage lasts a lifetime |

| Surrender Value | No surrender value | May have surrender value depending on policy terms |

Understanding LTC Insurance: Key Features and Benefits

Long-term care (LTC) insurance provides dedicated coverage for expenses related to nursing homes, assisted living, and in-home care, helping protect savings from high care costs. Hybrid life-LTC policies combine life insurance with LTC benefits, offering a death benefit if care is not needed, while accelerating benefits if long-term care services are required. Choosing between these options depends on factors such as premium affordability, coverage flexibility, and the desire for a guaranteed death benefit.

What Is a Hybrid Life-LTC Policy?

A hybrid life-LTC policy combines permanent life insurance with long-term care benefits, allowing policyholders to access a portion of the death benefit to cover LTC expenses. This integrated approach provides financial protection by ensuring funds are available for care without depleting separate assets. Hybrid policies often include guaranteed premiums and cash value accumulation, making them a versatile option for comprehensive long-term care planning.

Cost Comparison: LTC Insurance vs. Hybrid Policies

Traditional long-term care (LTC) insurance typically features lower initial premiums but can become costly over time due to inflation and premium hikes, whereas hybrid life-LTC policies have higher upfront costs combined with life insurance benefits and more stable premiums. Hybrid policies offer the advantage of a death benefit if long-term care is not needed, providing greater value and financial security compared to standalone LTC insurance. When evaluating long-term care planning, hybrid policies often present a more predictable expense with dual-purpose coverage, reducing the risk of out-of-pocket expenses linked to LTC insurance premium increases.

Coverage Flexibility: Standalone vs. Hybrid Options

LTC insurance offers dedicated long-term care coverage with customizable benefits tailored specifically for care needs, providing clear separation between life insurance and LTC benefits. Hybrid life-LTC policies combine life insurance with LTC coverage, allowing policyholders to flexibly access death benefits or LTC funds depending on their health status, often resulting in cash value accumulation. The choice between standalone LTC and hybrid policies depends on desired coverage flexibility, budget considerations, and the prioritization of either pure LTC protection or integrated life and care benefits.

Premium Stability and Rate Increases

Premium stability in traditional LTC insurance can be unpredictable, often subject to significant rate increases due to rising healthcare costs and longer life expectancies. Hybrid life-LTC policies typically offer more predictable premium structures by combining life insurance benefits with long-term care coverage, reducing the risk of unexpected rate hikes. Policyholders benefit from the dual-purpose value of hybrid plans, as premiums contribute toward both death benefits and LTC funding, enhancing overall cost efficiency and financial planning stability.

Benefit Triggers: How Claims Are Accessed

Benefit triggers for LTC insurance typically require medical necessity criteria such as the inability to perform two or more Activities of Daily Living (ADLs) or severe cognitive impairment to access claims. Hybrid life-LTC policies combine life insurance with LTC benefits, often allowing claim access through similar ADL triggers but may also offer cash value access or accelerated death benefits linked to long-term care needs. Understanding the specific benefit triggers in each policy is crucial for effective long-term care planning and ensuring timely claim payments.

Tax Advantages: LTC Insurance vs. Hybrid Solutions

Long-term care (LTC) insurance offers tax-deductible premiums and tax-free benefits when used for qualified care expenses, providing clear tax advantages under IRS Section 213(d). Hybrid life-LTC policies combine life insurance with LTC benefits, allowing tax-deferred cash value growth and tax-free LTC reimbursements up to policy limits, effectively merging estate planning with long-term care coverage. Choosing between traditional LTC insurance and hybrid solutions depends on individual financial goals, risk tolerance, and the desire to maximize tax-efficient asset protection.

Inheritance and Death Benefit Considerations

Hybrid life-LTC policies combine long-term care coverage with a guaranteed death benefit, ensuring that heirs receive an inheritance even if long-term care benefits are used. In contrast, traditional LTC insurance offers no death benefit or inheritance value, as premiums solely cover care expenses. Choosing a hybrid policy can provide financial protection for beneficiaries while addressing potential long-term care needs.

Suitability: Who Should Choose Which Policy?

Individuals seeking dedicated, comprehensive long-term care coverage with predictable benefits often find traditional LTC insurance more suitable due to its specialized focus. Those desiring a combination of life insurance protection alongside flexible long-term care benefits may benefit from hybrid life-LTC policies, which integrate death benefits with care coverage. Hybrid policies are typically ideal for people wanting guaranteed cash value and legacy options, while traditional LTC insurance suits those prioritizing robust, standalone long-term care planning.

Making an Informed Long-Term Care Planning Decision

Long-term care (LTC) insurance provides dedicated coverage for extended care needs, offering predictable benefits and premiums tailored specifically for nursing home, assisted living, or home care services. Hybrid life-LTC policies combine permanent life insurance with long-term care benefits, enabling policyholders to access death benefits or LTC funds, providing flexibility and potential estate value. Evaluating individual health, financial goals, and risk tolerance is essential for making an informed decision between standalone LTC insurance and hybrid life-LTC options for comprehensive long-term care planning.

Related Important Terms

Asset-Based LTC

Asset-based long-term care (LTC) insurance combines life insurance with LTC benefits, allowing policyholders to access a portion of their death benefit for care expenses, providing financial flexibility and estate protection. Traditional LTC insurance requires separate premium payments and offers coverage solely for care needs, which may result in higher overall costs compared to the integrated hybrid life-LTC policy.

Life-LTC Linked Riders

Life-LTC linked riders combine life insurance protection with long-term care benefits, allowing policyholders to access a portion of the death benefit for qualifying care expenses, offering more flexibility compared to traditional LTC insurance that strictly covers long-term care costs. These hybrid policies typically have lower premiums over time and eliminate the risk of losing coverage if long-term care is not needed, providing both financial security and care planning advantages.

Cash Indemnity Hybrid

Cash indemnity hybrid life-LTC policies provide flexible long-term care benefits by paying a predetermined cash amount regardless of actual care expenses, combining life insurance coverage with LTC protection in a single contract. These policies offer guaranteed death benefits alongside tax-advantaged cash payouts for qualified long-term care services, enhancing financial security and simplifying long-term care planning compared to traditional standalone LTC insurance.

Paid-Up LTC Rider

A Paid-Up LTC Rider in a Hybrid Life-LTC policy offers the advantage of fully funding long-term care benefits without additional premium payments, contrasting with standalone LTC insurance that may require ongoing premiums and separate underwriting. This rider enhances financial predictability and ensures continuous LTC coverage by integrating life insurance death benefits with long-term care funding.

1035 Exchange for Hybrid

A 1035 Exchange enables policyholders to transfer funds from a traditional long-term care (LTC) insurance policy to a Hybrid life-LTC insurance policy without incurring immediate tax consequences, optimizing benefits under a single contract. Hybrid life-LTC policies combine death benefits with LTC coverage, offering more flexible financial planning and potential cash value accumulation compared to standalone LTC insurance.

Return of Premium LTC

Return of Premium long-term care (LTC) insurance offers a traditional standalone policy that refunds premiums if no long-term care benefits are used, providing financial security and flexibility. Hybrid life-LTC policies combine life insurance with LTC coverage, allowing policyholders to use the death benefit for care expenses or pass it on to beneficiaries, optimizing asset protection and legacy planning.

Guaranteed Universal Life Hybrid

Guaranteed Universal Life Hybrid policies combine permanent life insurance protection with long-term care benefits, offering a tax-advantaged solution that provides lifelong coverage while funding future care needs. These policies typically feature fixed premiums and guaranteed death benefits, making them more predictable and often more cost-effective compared to standalone LTC insurance.

Chronic Illness Accelerated Benefit

Chronic Illness Accelerated Benefit in hybrid life-LTC policies offers a streamlined way to access long-term care funds as part of the life insurance death benefit, enhancing liquidity and flexibility compared to standalone LTC insurance. These hybrid policies often provide lock-in value and premium stability, making them a strategic option for long-term care planning with built-in chronic illness protection.

Elimination Period Flexibility

Long-term care (LTC) insurance offers elimination period flexibility, allowing policyholders to choose a waiting period before benefits begin, which can tailor premium costs to individual financial strategies. Hybrid life-LTC policies combine life insurance with LTC coverage but often have fixed elimination periods, potentially limiting adaptability in long-term care planning compared to standalone LTC insurance.

Inflation Protection Embedded

LTC insurance typically offers standalone coverage for long-term care services but may require separate riders for inflation protection, increasing overall premiums. Hybrid life-LTC policies embed inflation protection directly within the death benefit and long-term care coverage, ensuring that benefits keep pace with rising care costs without additional premium adjustments.

LTC insurance vs Hybrid life-LTC policy for long-term care planning. Infographic