Term Life insurance offers affordable coverage for a specified period, providing a death benefit if the insured passes away during the term, with no payout if the policy expires. Return of Premium (ROP) Term Life insurance refunds all paid premiums at the end of the term if the insured outlives the policy, combining protection with a savings component. Choosing between Term Life and ROP depends on budget preferences and whether policyholders value potential premium recovery or purely economical coverage.

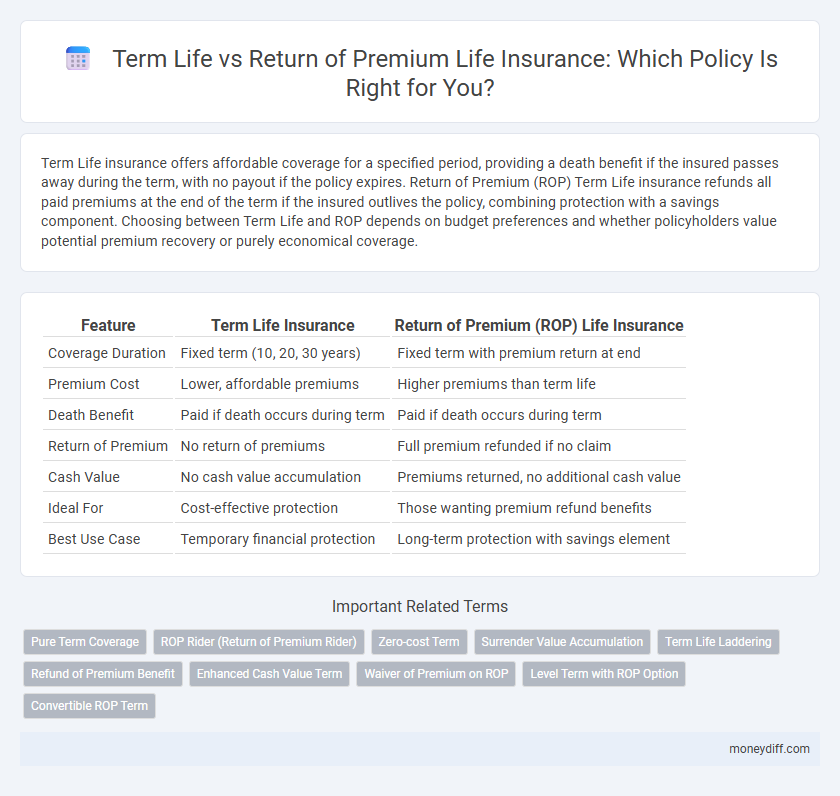

Table of Comparison

| Feature | Term Life Insurance | Return of Premium (ROP) Life Insurance |

|---|---|---|

| Coverage Duration | Fixed term (10, 20, 30 years) | Fixed term with premium return at end |

| Premium Cost | Lower, affordable premiums | Higher premiums than term life |

| Death Benefit | Paid if death occurs during term | Paid if death occurs during term |

| Return of Premium | No return of premiums | Full premium refunded if no claim |

| Cash Value | No cash value accumulation | Premiums returned, no additional cash value |

| Ideal For | Cost-effective protection | Those wanting premium refund benefits |

| Best Use Case | Temporary financial protection | Long-term protection with savings element |

Understanding Term Life Insurance

Term life insurance provides coverage for a specified period, typically 10, 20, or 30 years, offering a death benefit to beneficiaries if the insured passes away during the term. It is generally more affordable than other life insurance types because it does not accumulate cash value, focusing solely on pure protection. Policyholders seeking straightforward, cost-effective coverage often prefer term life insurance due to its simplicity and ability to secure a fixed premium for the term duration.

What is Return of Premium (ROP) Life Insurance?

Return of Premium (ROP) Life Insurance is a type of term life policy that refunds the total premiums paid if the insured outlives the coverage period, combining life insurance protection with a savings component. Unlike traditional term life insurance, which provides a death benefit only, ROP policies offer financial recovery of paid premiums, making them appealing for policyholders seeking both security and the potential to recapture costs. ROP life insurance usually comes with higher premiums compared to standard term life policies due to its refund feature and limited investment returns.

Key Differences: Term Life vs ROP Life Insurance

Term Life Insurance offers coverage for a specified period with lower premiums but no payout if the insured outlives the term, whereas Return of Premium (ROP) Life Insurance refunds all paid premiums if the policyholder survives the term. ROP policies combine life coverage with a savings component, resulting in higher premiums compared to standard Term Life plans. Choosing between Term Life and ROP Life insurance depends on budget, risk tolerance, and long-term financial goals.

Cost Comparison: Premiums and Affordability

Term life insurance typically offers lower premiums compared to return of premium (ROP) life insurance, making it a more affordable choice for budget-conscious individuals seeking coverage. ROP policies require higher premiums since they refund the total amount paid if the policyholder outlives the term, combining insurance with a savings component. Evaluating affordability involves balancing the higher upfront cost of ROP premiums against the potential return, while term life premiums provide cost-effective protection without any payout if the insured survives.

Coverage Duration and Flexibility

Term Life Insurance provides coverage for a specific period, typically 10 to 30 years, offering affordability and straightforward protection without cash value accumulation. Return of Premium (ROP) Life Insurance combines term coverage with a refund of premiums paid if the insured outlives the policy term, providing added financial security but at higher initial costs. ROP policies may offer less flexibility in coverage adjustments compared to standard term life plans, which can often be converted or renewed at the end of the term.

Benefits and Drawbacks of Term Life

Term life insurance offers affordable coverage for a specified period, providing significant death benefits with lower premiums compared to other policies, making it ideal for budget-conscious individuals seeking temporary protection. The drawback lies in the lack of cash value accumulation, and if the insured outlives the term, no benefits or premiums are returned, potentially leading to lost investment value. Term life is best suited for covering financial obligations like mortgages or education expenses during peak earning years without long-term commitment or higher costs.

Pros and Cons of ROP Life Insurance

Return of Premium (ROP) life insurance offers the advantage of refunding the total premiums paid if the policyholder outlives the term, providing a savings-like benefit. This policy tends to have higher premiums compared to traditional term life insurance, making it less affordable for budget-conscious individuals. While ROP policies eliminate the risk of lost premiums, the increased cost may not justify the benefit for those primarily seeking pure life insurance protection.

Suitability: Who Should Choose Which Option?

Term Life insurance is ideal for individuals seeking affordable coverage for a specific period, such as parents with dependents or those with temporary financial obligations. Return of Premium Life insurance suits policyholders who prefer a no-loss option, often appealing to risk-averse clients willing to pay higher premiums in exchange for premium refunds if no claim is made. Evaluating financial goals, budget constraints, and risk tolerance is crucial to determine the most appropriate life insurance product.

Financial Implications and Long-term Value

Term Life Insurance offers lower premiums compared to Return of Premium (ROP) policies, making it cost-effective for budget-conscious individuals seeking substantial coverage during a specific period. Return of Premium insurance requires higher payments but refunds all premiums if the insured outlives the term, creating a forced savings mechanism with long-term financial value. Evaluating the total cost over the policy duration against potential refunds is essential for understanding the long-term financial implications of each option.

Making the Best Choice for Your Money Management

Term Life Insurance offers affordable coverage for a specified period, providing a death benefit without accumulating cash value, making it cost-effective for budget-conscious individuals. Return of Premium Life Insurance refunds the total premiums paid if the insured outlives the policy term, combining protection with potential savings but at higher initial costs. Evaluating your financial goals, risk tolerance, and long-term money management strategy is crucial when selecting between cost-efficiency and premium recovery in life insurance options.

Related Important Terms

Pure Term Coverage

Pure Term Life insurance offers affordable, straightforward coverage for a specified period without accumulating cash value, providing maximum death benefit protection. Return of Premium Life insurance refunds the total premiums paid if the insured outlives the term, typically resulting in higher costs but a potential return on investment.

ROP Rider (Return of Premium Rider)

The Return of Premium (ROP) rider on a term life insurance policy allows policyholders to receive a refund of all paid premiums if they outlive the term, enhancing the policy's value compared to traditional term life insurance that only provides a death benefit. This rider effectively combines the affordability of term life with a savings component, making it an attractive option for those seeking financial protection with potential premium recovery.

Zero-cost Term

Term Life insurance offers affordable coverage for a specific period without a savings component, while Return of Premium (ROP) Life insurance refunds all premiums paid if you outlive the policy, creating a zero-cost term option by effectively recovering your payments. Zero-cost Term Life provides temporary protection with the potential for a full premium return, blending cost-efficiency and financial security.

Surrender Value Accumulation

Term Life insurance typically has no surrender value as it only provides coverage for a specified period without accumulating cash value, whereas Return of Premium Life insurance accumulates surrender value by refunding premiums paid if the policyholder outlives the term, offering a financial benefit beyond death coverage. The surrender value accumulation in Return of Premium Life can serve as a forced savings mechanism, making it a more attractive option for policyholders seeking both protection and potential return on premiums.

Term Life Laddering

Term Life Laddering maximizes coverage efficiency by purchasing multiple term life policies with staggered expiration dates, providing tailored protection aligned with specific financial obligations over time. Compared to Return of Premium Life insurance, which offers premium refunds if no claim is made, Term Life Laddering delivers cost-effective coverage without the higher premiums associated with return guarantees, optimizing long-term financial planning and risk management.

Refund of Premium Benefit

Return of Premium Life insurance offers a unique Refund of Premium Benefit, reimbursing policyholders with the total amount of premiums paid if they outlive the policy term, unlike traditional Term Life which provides no such refund. This benefit enhances cash value potential and acts as a forced savings mechanism, appealing to individuals seeking both coverage and premium recovery.

Enhanced Cash Value Term

Enhanced Cash Value Term life insurance offers a unique blend of affordable term coverage with a cash value component that accumulates over time, distinguishing it from traditional Term Life policies which do not build cash value. Return of Premium Life insurance refunds the total premiums paid if the insured outlives the term, but Enhanced Cash Value Term provides added financial flexibility by allowing policyholders to access accumulated cash value during the term.

Waiver of Premium on ROP

Return of Premium (ROP) Life Insurance includes a Waiver of Premium rider that exempts policyholders from paying premiums if they become disabled, ensuring continuous coverage without financial burden. This feature enhances the ROP policy's value over traditional Term Life Insurance by combining the benefit of premium return with disability protection.

Level Term with ROP Option

Level Term Life Insurance with a Return of Premium (ROP) option provides a fixed premium and coverage amount for the policy term, while refunding all premiums paid if the insured outlives the term, making it a cost-effective choice for risk-averse individuals seeking financial security. This option combines the affordability of traditional level term policies with an investment-like benefit, enhancing long-term value by returning premiums without interest at the end of the coverage period.

Convertible ROP Term

Convertible Return of Premium (ROP) Term Life Insurance offers policyholders the flexibility to convert their term coverage into a permanent life insurance policy without additional medical underwriting, combining the affordability of term life with the long-term benefits of whole life. This type of policy returns the total premiums paid if the insured outlives the term, enhancing financial security while maintaining the option for lifelong coverage.

Term Life vs Return of Premium Life for life insurance. Infographic