Whole life insurance offers guaranteed lifelong protection with fixed premiums and a cash value that grows at a predetermined rate, providing stability and predictability. Indexed universal life insurance combines flexible premiums and adjustable death benefits with cash value growth linked to a stock market index, offering potential for higher returns but with more risk. Choosing between these depends on your preference for consistent growth versus market-linked growth and flexibility in premium payments.

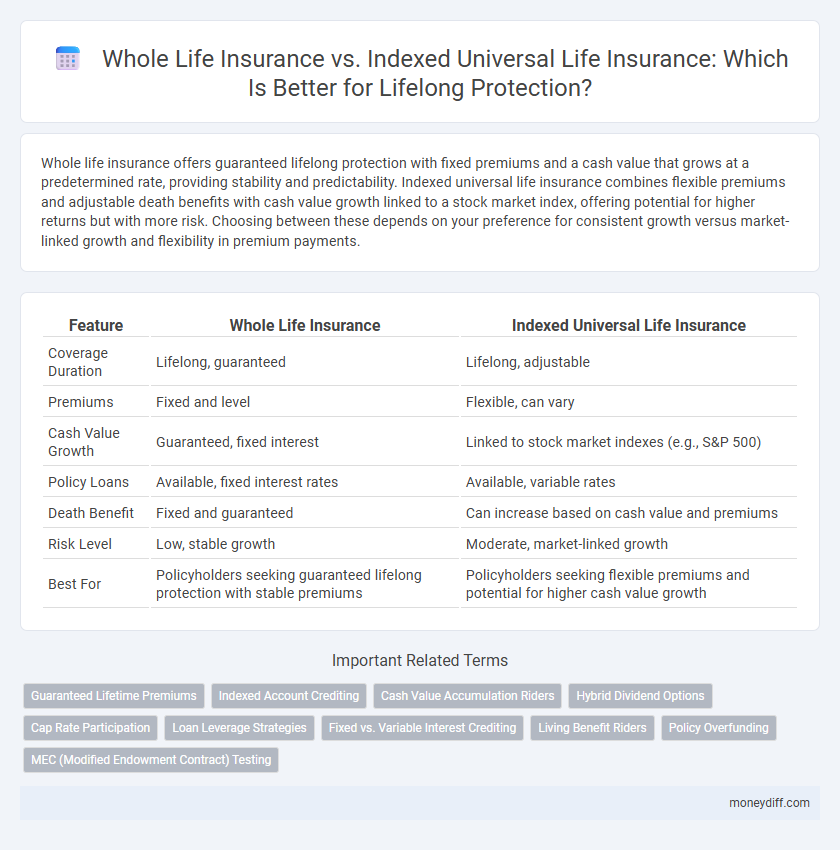

Table of Comparison

| Feature | Whole Life Insurance | Indexed Universal Life Insurance |

|---|---|---|

| Coverage Duration | Lifelong, guaranteed | Lifelong, adjustable |

| Premiums | Fixed and level | Flexible, can vary |

| Cash Value Growth | Guaranteed, fixed interest | Linked to stock market indexes (e.g., S&P 500) |

| Policy Loans | Available, fixed interest rates | Available, variable rates |

| Death Benefit | Fixed and guaranteed | Can increase based on cash value and premiums |

| Risk Level | Low, stable growth | Moderate, market-linked growth |

| Best For | Policyholders seeking guaranteed lifelong protection with stable premiums | Policyholders seeking flexible premiums and potential for higher cash value growth |

Understanding Whole Life Insurance: An Overview

Whole life insurance offers guaranteed lifelong coverage with fixed premiums and a guaranteed cash value accumulation, making it a reliable choice for policyholders seeking stability and predictability. Indexed universal life insurance combines permanent coverage with flexible premiums and potential cash value growth tied to stock market indexes, providing opportunities for higher returns while maintaining downside protection. Choosing between these policies depends on the need for guaranteed benefits versus growth potential and premium flexibility within a lifelong insurance strategy.

What Is Indexed Universal Life Insurance?

Indexed Universal Life (IUL) insurance is a type of permanent life insurance that combines a death benefit with a cash value component tied to a stock market index, such as the S&P 500, offering potential for growth without direct market risk. Policyholders benefit from flexible premiums and the ability to adjust death benefits, making IUL a versatile option for lifelong protection. Unlike traditional whole life insurance, IUL policies allow for cash value accumulation based on index performance, potentially increasing policy value over time while providing downside protection.

Key Differences Between Whole Life and Indexed Universal Life Insurance

Whole life insurance offers fixed premiums, guaranteed death benefits, and a cash value component that grows at a guaranteed rate, providing stable lifelong protection. Indexed universal life insurance features flexible premiums and death benefits, with cash value growth tied to a stock market index, offering potential for higher returns but with more risk. The choice depends on the need for predictability and guaranteed growth versus flexibility and the opportunity for greater cash value accumulation.

Lifetime Protection: How Both Policies Secure Your Future

Whole life insurance guarantees lifelong protection through fixed premiums and a guaranteed death benefit, ensuring financial security for beneficiaries. Indexed universal life insurance offers flexible premiums and an adjustable death benefit, with potential cash value growth tied to market indexes, enhancing long-term value. Both policies provide permanent coverage that safeguards your financial future and supports wealth transfer strategies.

Premium Structure: Level vs Flexible Payments

Whole life insurance offers a level premium structure, providing consistent and predictable payments throughout the policyholder's life, ensuring stable budgeting and guaranteed lifelong protection. Indexed universal life insurance features flexible premium payments, allowing policyholders to adjust contributions based on financial circumstances while linking cash value growth to market indices for potential higher returns. Understanding these premium structures helps individuals choose between stable costs and adaptable payments in their lifelong insurance strategy.

Cash Value Growth: Guaranteed vs Indexed Returns

Whole life insurance offers guaranteed cash value growth with fixed interest rates, ensuring steady accumulation over time. Indexed universal life insurance links cash value growth to the performance of market indices, providing potential for higher returns without direct market risk exposure. Policyholders seeking predictable accumulation may prefer whole life, while those aiming for variable growth tied to market gains might opt for indexed universal life insurance.

Policy Loans and Withdrawals: Accessing Your Cash Value

Whole life insurance offers guaranteed policy loans and fixed interest rates, ensuring predictable access to cash value without reducing the death benefit if managed properly. Indexed universal life insurance allows flexible withdrawals and loans tied to market index performance, providing potential for higher cash value growth but with variability in available funds. Both policies enable lifelong protection while offering different strategies for accessing accumulated cash value.

Costs and Fees: What to Expect with Each Policy

Whole life insurance typically features fixed premiums and guaranteed cash value growth, with fees often embedded in the cost, making it more predictable for long-term budgeting. Indexed universal life insurance offers flexible premiums and potential for cash value growth linked to market indexes, but policyholders may encounter higher fees, including cost of insurance charges, administrative fees, and cap rates that can reduce returns. Understanding these cost structures is crucial for selecting a policy that aligns with your financial goals and risk tolerance over a lifetime.

Suitability: Who Should Choose Whole Life or Indexed Universal Life?

Whole life insurance suits individuals seeking guaranteed lifelong coverage with fixed premiums and predictable cash value growth, ideal for conservative planners valuing stability. Indexed universal life insurance appeals to policyholders desiring flexible premiums and death benefits, along with cash value linked to a market index, suitable for those comfortable with investment risk and aiming for potential higher returns. Choosing between these depends on risk tolerance, financial goals, and the need for policy customization versus guaranteed predictability.

Making the Right Choice for Your Long-Term Financial Goals

Whole life insurance offers guaranteed lifelong coverage with fixed premiums and a cash value component that grows at a guaranteed rate, providing financial stability and predictability. Indexed universal life insurance combines lifelong protection with flexible premiums and the potential for cash value growth linked to stock market indexes, allowing for higher returns but with increased risk. Choosing between these policies requires evaluating your risk tolerance, financial goals, and need for flexibility to ensure the best fit for your long-term wealth accumulation and legacy planning.

Related Important Terms

Guaranteed Lifetime Premiums

Whole life insurance offers guaranteed lifetime premiums, ensuring stable costs throughout the policyholder's life, while indexed universal life insurance premiums can vary based on market performance and policy adjustments. Choosing whole life insurance provides predictability and financial security for lifelong protection without premium increases.

Indexed Account Crediting

Indexed universal life insurance offers lifelong protection with cash value growth linked to a stock market index, providing potential for higher returns compared to whole life insurance's fixed interest. The indexed account crediting method utilizes market performance to increase cash value while protecting principal from downside risk, enhancing policyholder's flexibility and growth potential.

Cash Value Accumulation Riders

Whole life insurance offers guaranteed cash value accumulation with fixed premiums and stable growth, while indexed universal life insurance provides the potential for higher cash value growth through market-linked indexes coupled with flexible premiums. Cash value accumulation riders in indexed universal life policies optimize lifelong protection by enhancing cash value growth using credited interest tied to index performance without the risk of market losses.

Hybrid Dividend Options

Whole life insurance offers stable premiums and guaranteed dividends, providing predictable lifelong protection with potential cash value growth. Indexed universal life insurance combines flexible premiums with the opportunity to earn interest linked to stock market indexes, allowing hybrid dividend options that can enhance cash value accumulation while managing risk.

Cap Rate Participation

Whole life insurance offers guaranteed cash value growth with fixed premiums, while indexed universal life insurance provides the opportunity for higher returns through market-linked cap rate participation without direct market risk. The cap rate in indexed universal life policies limits the maximum interest credited, balancing growth potential and risk for lifelong protection.

Loan Leverage Strategies

Whole life insurance offers guaranteed cash value accumulation with fixed loan interest rates, providing predictable loan leverage for lifelong protection, while indexed universal life insurance allows policyholders to leverage cash value linked to market indexes, potentially increasing borrowing capacity with flexible loan terms. Utilizing loan leverage strategies in indexed universal life can enhance liquidity during market upswings, contrasted with whole life's stable, conservative loan borrowing advantages.

Fixed vs. Variable Interest Crediting

Whole life insurance offers fixed interest crediting with guaranteed cash value growth, providing stable lifelong protection, while indexed universal life insurance credits interest based on the performance of a market index, allowing for variable growth potential with downside protection. The fixed nature of whole life ensures steady accumulation, whereas indexed universal life balances risk and reward through interest linked to index gains without direct market investment.

Living Benefit Riders

Whole life insurance offers guaranteed lifelong protection with fixed premiums and a cash value component, while indexed universal life insurance provides flexible premiums and potential cash value growth tied to market indexes. Living benefit riders in both policies enhance financial security by allowing access to funds for critical, chronic, or terminal illnesses, supporting policyholders during health emergencies without surrendering their coverage.

Policy Overfunding

Whole life insurance offers guaranteed cash value growth and fixed premiums, making it a stable choice for policy overfunding to maximize lifelong protection benefits. Indexed universal life insurance allows flexible premiums and ties cash value growth to market indexes, providing potential for higher returns while enabling strategic overfunding to enhance death benefits and cash accumulation.

MEC (Modified Endowment Contract) Testing

Whole life insurance offers guaranteed cash value growth and fixed premiums, avoiding Modified Endowment Contract (MEC) status due to its structured premium limits, ensuring tax-advantaged lifelong protection. Indexed universal life insurance features flexible premiums and potential cash value tied to market indexes but requires careful MEC testing to prevent adverse tax consequences on policy withdrawals and loans.

Whole life insurance vs Indexed universal life insurance for lifelong protection. Infographic