Homeowners insurance provides traditional coverage through established insurers, offering financial protection against property damage, theft, and liability claims with standardized policies and regulated underwriting. Peer-to-peer insurance leverages community-based risk sharing, enabling policyholders to pool resources and reduce premiums by minimizing administrative costs and promoting transparency. Choosing between the two depends on preferences for reliability, cost-efficiency, and control over claims management in property safeguarding.

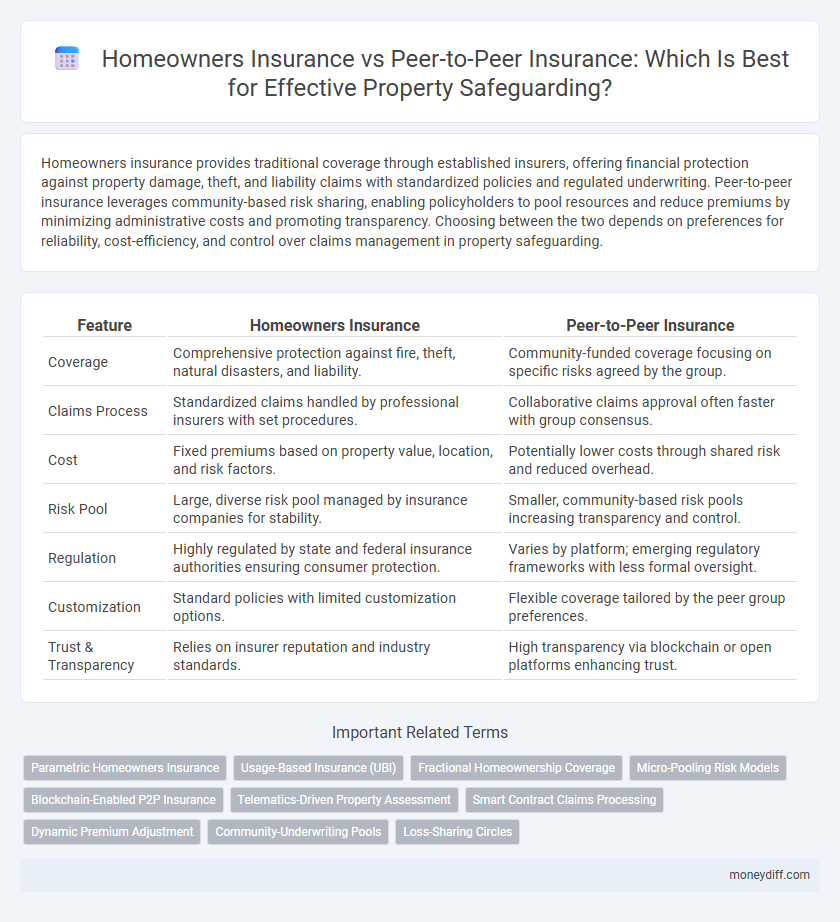

Table of Comparison

| Feature | Homeowners Insurance | Peer-to-Peer Insurance |

|---|---|---|

| Coverage | Comprehensive protection against fire, theft, natural disasters, and liability. | Community-funded coverage focusing on specific risks agreed by the group. |

| Claims Process | Standardized claims handled by professional insurers with set procedures. | Collaborative claims approval often faster with group consensus. |

| Cost | Fixed premiums based on property value, location, and risk factors. | Potentially lower costs through shared risk and reduced overhead. |

| Risk Pool | Large, diverse risk pool managed by insurance companies for stability. | Smaller, community-based risk pools increasing transparency and control. |

| Regulation | Highly regulated by state and federal insurance authorities ensuring consumer protection. | Varies by platform; emerging regulatory frameworks with less formal oversight. |

| Customization | Standard policies with limited customization options. | Flexible coverage tailored by the peer group preferences. |

| Trust & Transparency | Relies on insurer reputation and industry standards. | High transparency via blockchain or open platforms enhancing trust. |

Understanding Homeowners Insurance: Traditional Protection Explained

Homeowners insurance provides comprehensive protection by covering property damage, liability, and theft under standard policies regulated by insurance companies. This traditional coverage includes dwelling, personal property, and additional living expenses in case of covered perils such as fire, storms, or vandalism. Established underwriting processes and claims handling ensure predictable support and financial reimbursement for homeowners.

What Is Peer-to-Peer Insurance? An Innovative Alternative

Peer-to-peer insurance is a model where policyholders pool their premiums to insure each other, reducing reliance on traditional insurance companies. This innovative alternative fosters transparency, lowers costs, and often includes community-based claims management for homeowners seeking customized property safeguarding. Unlike conventional homeowners insurance, peer-to-peer insurance emphasizes shared risk and collective decision-making.

Coverage Comparison: Standard Policies vs Community-Based Models

Homeowners insurance offers standardized coverage including dwelling protection, personal property, liability, and additional living expenses, typically backed by established insurers with regulated claim processes. Peer-to-peer insurance models rely on community-funded pools where members share risks and claim costs, often providing more transparency and potential cost savings but with less coverage predictability. Standard policies generally provide comprehensive, legally mandated protections, whereas peer-to-peer coverage emphasizes collaborative risk management and flexibility according to the community's specific needs.

Cost Differences: Premiums, Fees, and Potential Savings

Homeowners insurance typically involves fixed premiums and standard fees set by established insurance companies, resulting in predictable but sometimes higher costs. Peer-to-peer insurance offers a cost-efficient alternative by pooling members' contributions, often lowering premiums and administrative fees through shared risk. Potential savings emerge from reduced overhead and the possibility of receiving refunds if claims are low within the group, making peer-to-peer models attractive for budget-conscious property owners.

Claims Process: How Homeowners and P2P Insurance Handle Loss

Homeowners insurance typically involves a centralized claims process managed by a professional insurer, ensuring standardized assessments and quicker payouts based on policy terms and documented losses. Peer-to-peer (P2P) insurance employs a community-driven claims approach, where claims are often evaluated by members of the group, potentially enhancing transparency but sometimes extending resolution timeframes. Both models require thorough documentation of property loss, but P2P platforms may include social verification elements that impact claim approval and reimbursement speed.

Risk Assessment: Underwriting in Traditional and P2P Insurance

Risk assessment in homeowners insurance relies on thorough underwriting processes performed by insurance companies to evaluate property risks, such as location, construction materials, and claim history. Peer-to-peer (P2P) insurance utilizes community-based risk pools where members collectively share risks, often supported by algorithmic assessments and transparency tools to manage underwriting more dynamically. Traditional underwriting offers personalized risk analysis and pricing, while P2P insurance leverages social data and technology to distribute risk and potentially reduce premiums through group incentives.

Community Trust: The Social Aspect of P2P Insurance

Peer-to-peer (P2P) insurance leverages community trust by pooling resources among members who share similar risks, fostering a sense of collective responsibility and transparency absent in traditional homeowners insurance. This social structure can lead to quicker claims resolution and reduced fraud due to active peer monitoring. The collaborative nature of P2P models enhances risk management and aligns incentives, promoting stronger community engagement in property safeguarding.

Regulatory Considerations: Legal and Compliance Factors

Homeowners insurance operates under well-established regulatory frameworks with standardized coverage mandates and state-specific compliance requirements, ensuring consumer protection and financial stability. Peer-to-peer insurance platforms face evolving regulatory scrutiny as they blend traditional insurance models with decentralized risk-sharing mechanisms, necessitating clear legal definitions and adherence to licensing, solvency, and consumer rights laws. Understanding these regulatory considerations is critical for property owners when choosing between conventional insurers and emerging peer-to-peer solutions for safeguarding real estate assets.

Pros and Cons: Weighing Homeowners and P2P Insurance Options

Homeowners insurance offers comprehensive coverage backed by established providers, ensuring reliable protection and legal compliance but often comes with higher premiums and less personalized service. Peer-to-peer insurance leverages community pooling to lower costs and foster transparency, yet it may present risks such as limited coverage scope and potential payout delays during high claim volumes. Evaluating factors like cost efficiency, coverage limits, claim processing speed, and risk tolerance is essential when choosing between traditional homeowners insurance and emerging P2P models.

Which Is Right for You? Choosing the Best Property Safeguarding Solution

Homeowners insurance offers comprehensive coverage backed by established insurance companies, ensuring protection against fire, theft, natural disasters, and liability claims. Peer-to-peer insurance leverages community risk-sharing, often providing lower premiums and increased transparency by pooling resources among policyholders. Evaluating factors like coverage scope, cost, claims process, and personal risk tolerance is essential to determine the most suitable property safeguarding solution for your needs.

Related Important Terms

Parametric Homeowners Insurance

Parametric homeowners insurance offers swift, predefined payout triggers based on measurable events such as wind speed or earthquake magnitude, providing transparent and efficient property safeguarding compared to traditional loss-assessment models. Peer-to-peer insurance pools risks among community members, but parametric policies reduce claim disputes and accelerate settlements by leveraging real-time data from trusted weather or seismic sources.

Usage-Based Insurance (UBI)

Usage-Based Insurance (UBI) in homeowners insurance leverages real-time data from smart home devices and sensors to tailor premiums based on actual property risk and homeowner behavior, enhancing cost efficiency and personalization. Peer-to-peer insurance platforms utilize UBI by pooling homeowners with similar risk profiles, promoting transparency and reducing fraud while incentivizing proactive property maintenance.

Fractional Homeownership Coverage

Fractional homeownership coverage in peer-to-peer insurance offers flexible, cost-effective protection by allowing multiple owners to collectively insure their property, minimizing individual premiums compared to traditional homeowners insurance. This model enhances risk distribution and transparency, empowering fractional owners with tailored coverage that adapts to shared property usage and ownership structures.

Micro-Pooling Risk Models

Micro-pooling risk models in peer-to-peer insurance enable homeowners to collectively share risks by forming small groups that contribute to a common fund, often resulting in lower premiums and increased transparency compared to traditional homeowners insurance. This decentralized approach leverages real-time data and community trust to enhance property safeguarding while minimizing administrative costs and claim disputes.

Blockchain-Enabled P2P Insurance

Blockchain-enabled P2P insurance leverages decentralized networks to offer transparent, cost-effective homeowners insurance by eliminating traditional intermediaries and enabling direct peer claims settlements. This technology enhances trust, reduces fraud risks, and customizes coverage to homeowners' specific needs through smart contracts, setting it apart from conventional insurance models.

Telematics-Driven Property Assessment

Telematics-driven property assessment in homeowners insurance leverages real-time data from smart sensors to monitor property conditions, enabling personalized risk evaluation and dynamic premium adjustments. Peer-to-peer insurance incorporates similar telematics technology but emphasizes community risk sharing and transparency, fostering collective accountability while potentially reducing costs through data-driven insights.

Smart Contract Claims Processing

Homeowners insurance typically relies on traditional claim processing methods that often involve lengthy verification and approval times, whereas peer-to-peer insurance leverages blockchain-based smart contract claims processing to automate and expedite claim settlements, increasing transparency and reducing fraud risks. Smart contracts enable real-time verification of property damage through predefined criteria, facilitating faster payouts and enhanced trust among policyholders within decentralized insurance pools.

Dynamic Premium Adjustment

Homeowners insurance typically offers fixed premiums based on standard risk assessments, while peer-to-peer insurance leverages dynamic premium adjustment through real-time data and community risk profiles, enabling personalized pricing and potentially lower costs. This adaptive approach in peer-to-peer models enhances property safeguarding by reflecting actual usage, behavior, and claim history more accurately than traditional fixed-premium homeowners policies.

Community-Underwriting Pools

Homeowners insurance provides property safeguarding through traditional underwriting and risk assessment by established insurance companies, while peer-to-peer insurance leverages community-underwriting pools where policyholders collectively share risk and claims costs, often resulting in lower premiums and increased transparency. Community-underwriting pools foster mutual trust and incentivize risk prevention by aligning interests among members in the insurance ecosystem.

Loss-Sharing Circles

Homeowners insurance typically involves a traditional risk transfer model where an insurer underwrites and covers property losses, whereas peer-to-peer (P2P) insurance utilizes loss-sharing circles, enabling groups of policyholders to pool premiums and share financial responsibility for claims directly. Loss-sharing circles in P2P insurance enhance transparency, reduce administrative costs, and can incentivize risk mitigation among participants, offering a collaborative alternative to conventional coverage for property safeguarding.

Homeowners Insurance vs Peer-to-Peer Insurance for property safeguarding. Infographic