Life insurance provides financial protection to beneficiaries upon the insured's death, offering a lump sum or regular payouts for long-term security. Parametric insurance, on the other hand, triggers payments based on predefined events or parameters, such as natural disasters, enabling faster claims without detailed loss assessments. Choosing between life insurance and parametric insurance depends on whether the coverage need is personal financial security or rapid response to specific events.

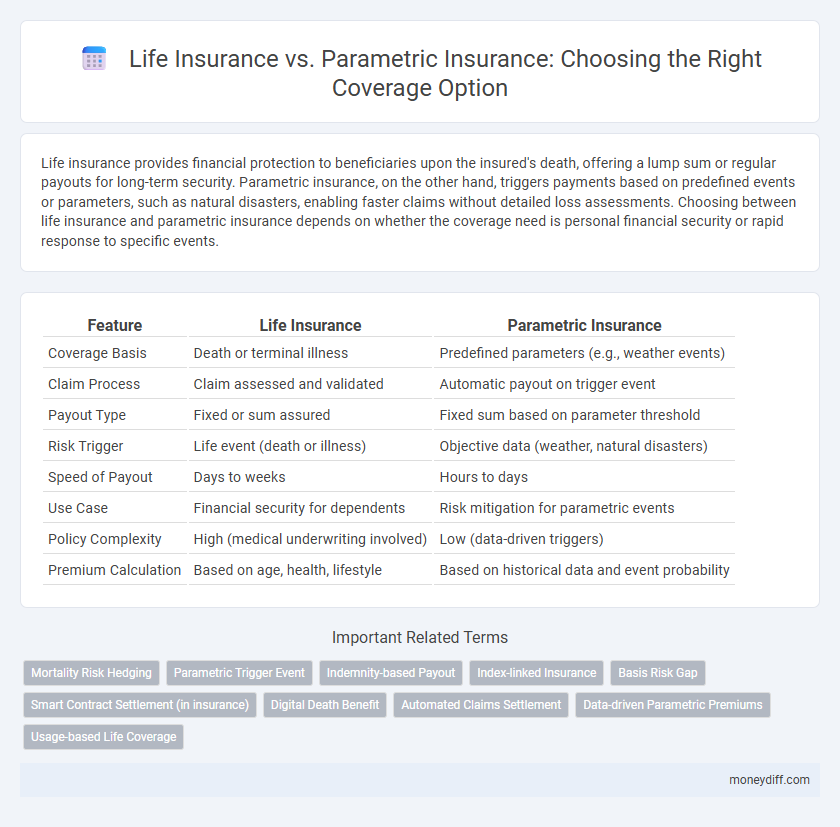

Table of Comparison

| Feature | Life Insurance | Parametric Insurance |

|---|---|---|

| Coverage Basis | Death or terminal illness | Predefined parameters (e.g., weather events) |

| Claim Process | Claim assessed and validated | Automatic payout on trigger event |

| Payout Type | Fixed or sum assured | Fixed sum based on parameter threshold |

| Risk Trigger | Life event (death or illness) | Objective data (weather, natural disasters) |

| Speed of Payout | Days to weeks | Hours to days |

| Use Case | Financial security for dependents | Risk mitigation for parametric events |

| Policy Complexity | High (medical underwriting involved) | Low (data-driven triggers) |

| Premium Calculation | Based on age, health, lifestyle | Based on historical data and event probability |

Understanding Life Insurance: Traditional Coverage Explained

Life insurance provides financial protection by paying beneficiaries a lump sum upon the insured's death, ensuring income replacement and debt coverage for dependents. Traditional life insurance policies include term life, offering coverage for a specified period, and whole life, which combines a death benefit with a savings component. Unlike parametric insurance, which pays based on predefined triggers like natural disasters, life insurance focuses on individual mortality risk and long-term financial security.

What is Parametric Insurance? A Modern Approach

Parametric insurance offers a modern approach by providing coverage based on predefined triggers or parameters, such as weather data or seismic activity, instead of traditional indemnity-based claims. This type of insurance ensures swift payouts once specific conditions are met, reducing claim processing time and administrative costs. Unlike life insurance, which compensates beneficiaries after an event like death, parametric insurance focuses on rapid financial relief tied to measurable events, making it ideal for natural disaster risk management.

Key Differences Between Life and Parametric Insurance

Life insurance provides financial protection to beneficiaries upon the policyholder's death, typically requiring claims processing based on proof of loss and medical documentation. Parametric insurance offers predetermined payouts triggered by predefined events or parameters, such as natural disasters, enabling faster claims settlement without traditional loss assessment. The key difference lies in life insurance's indemnity-based model versus parametric insurance's index-based approach focused on objective event data for coverage validation.

Coverage Scope: Life Insurance vs Parametric Insurance

Life insurance provides comprehensive coverage by paying a predetermined benefit upon the policyholder's death, ensuring financial security for beneficiaries regardless of specific event triggers. Parametric insurance delivers payouts based on predefined parameters or measurable events, such as natural disasters, offering fast, transparent claims without assessing actual loss. The coverage scope of life insurance centers on mortality risk protection, while parametric insurance targets quantifiable risks, offering tailored solutions for event-driven financial protection.

How Claims are Paid: Traditional vs Parametric Models

Life insurance claims are typically paid based on a thorough assessment of documented losses, requiring detailed proof such as death certificates and beneficiary requests. Parametric insurance simplifies claim payments by using predefined triggers like weather data or event parameters, enabling faster payouts without the need for loss adjustment. This model reduces administrative delays and increases transparency, offering a more efficient alternative to traditional indemnity-based life insurance claims.

Flexibility and Customization: Comparing Coverage Options

Life insurance offers customizable coverage options tailored to individual financial needs, such as term, whole, or universal life policies with adjustable premiums and benefits. Parametric insurance provides flexible, trigger-based payouts linked to specific event parameters, enabling quicker claims and tailored risk protection without traditional loss assessments. The choice depends on desired flexibility in benefit structure versus rapid, data-driven compensation tailored to measurable events.

Payout Speed: Life Insurance vs Parametric Insurance

Parametric insurance delivers payouts rapidly by triggering payments based on predefined parameters, eliminating lengthy claim assessments common in traditional life insurance. Life insurance involves detailed claim investigations and documentation, often resulting in slower payout times. This speed advantage makes parametric insurance ideal for urgent financial needs following specific events.

Cost Comparison: Premiums and Value for Money

Life insurance premiums are typically higher due to personalized risk assessments and comprehensive coverage, while parametric insurance offers lower premiums by triggering payouts based on predefined events rather than assessed losses. Parametric insurance delivers faster claims processing and potentially better value for money in scenarios with clear, quantifiable triggers, but may lack the tailored protection life insurance provides. Evaluating cost-effectiveness depends on the balance between premium affordability and the specific coverage needs of the insured.

Suitability: Who Should Choose Life or Parametric Insurance?

Life insurance is ideal for individuals seeking financial protection for their beneficiaries in the event of death, offering predictable payouts based on predefined conditions such as mortality. Parametric insurance suits those exposed to specific, measurable risks like natural disasters, providing rapid compensation triggered by predefined parameters rather than traditional claims assessments. Choosing between the two depends on whether the primary need is long-term financial security for dependents or swift coverage for quantifiable event-driven losses.

Future Trends: The Evolving Role of Parametric Insurance

Parametric insurance is rapidly transforming the life insurance landscape by offering faster claims processing through predefined triggers based on objective data such as weather events or biometric readings. Emerging technologies like IoT sensors and AI analytics enhance the precision and responsiveness of parametric policies, positioning them as a complementary solution to traditional life insurance coverage. Market forecasts predict significant growth in parametric insurance adoption, driven by increasing demand for transparent, efficient, and customizable risk management options.

Related Important Terms

Mortality Risk Hedging

Life insurance provides financial protection against mortality risk by paying a death benefit upon the insured's passing, ensuring beneficiaries receive a fixed amount regardless of external factors. Parametric insurance offers mortality risk hedging through predefined triggers based on quantitative data, enabling faster payouts that are not dependent on loss assessments or traditional claims processes.

Parametric Trigger Event

Parametric insurance provides coverage based on predefined trigger events such as specific weather conditions or natural disasters, allowing for faster and more transparent claim payouts compared to traditional life insurance that relies on individual risk assessment and claim verification. The parametric trigger event eliminates the need for loss adjustment, accelerating benefit distribution and reducing administrative costs.

Indemnity-based Payout

Life insurance provides indemnity-based payouts by compensating beneficiaries for financial losses due to the insured individual's death, typically based on the policy's face value and loss assessment. Parametric insurance differs by delivering pre-agreed fixed payouts triggered by specific event parameters, reducing claims processing time but not directly matching actual financial loss.

Index-linked Insurance

Life insurance provides financial protection based on the policyholder's life events, while parametric insurance offers rapid payouts triggered by predefined index measurements such as natural disaster metrics, making index-linked insurance ideal for transparent, objective, and quick coverage settlements in scenarios like climate-related risks. Index-linked parametric insurance reduces claim processing time and enhances risk management efficiency by relying on external data indices instead of traditional loss assessments.

Basis Risk Gap

Life insurance provides financial protection based on the insured's death or disability, while parametric insurance uses predefined triggers like weather events to pay claims quickly but often introduces basis risk due to discrepancies between the trigger event and actual losses. The basis risk gap in parametric insurance can leave policyholders undercompensated compared to traditional life insurance, which directly indemnifies verified losses.

Smart Contract Settlement (in insurance)

Life insurance typically involves traditional claim processes requiring detailed assessments, whereas parametric insurance leverages smart contract settlement to automate payouts based on predefined triggers like weather data or indices. This blockchain-enabled automation reduces processing time and administrative costs, ensuring faster and transparent compensation to policyholders without the need for loss validation.

Digital Death Benefit

Life insurance provides a traditional death benefit payout based on a policyholder's death, while parametric insurance offers a digital death benefit triggered by predefined events or data parameters, enabling faster and more transparent claims processing. Parametric coverage leverages real-time digital data to automate payouts, reducing claim disputes and accelerating financial support to beneficiaries.

Automated Claims Settlement

Life insurance typically requires detailed claim assessments and documentation, whereas parametric insurance streamlines automated claims settlement by triggering payouts based on predefined parameters and real-time data, significantly reducing processing time. This automation enhances efficiency and transparency, offering faster financial relief to policyholders without extensive claims verification.

Data-driven Parametric Premiums

Life insurance premiums are traditionally based on actuarial data and individual risk assessments, whereas parametric insurance leverages real-time data triggers such as weather events or natural disasters to automatically calculate claims and premiums. Data-driven parametric premiums offer greater transparency and speed in payouts by utilizing precise metrics and minimizing subjective loss adjustments.

Usage-based Life Coverage

Usage-based life insurance leverages real-time data from wearables and health apps to tailor premiums and coverage, providing a personalized approach compared to traditional parametric insurance that pays out based on predefined events or indices. This model enhances risk assessment accuracy and customer engagement by dynamically adjusting benefits according to individual behavior and health metrics.

Life Insurance vs Parametric Insurance for coverage. Infographic