Premium payments for traditional insurance often pose affordability challenges for low-income individuals due to high costs and lengthy commitments. Microinsurance offers a cost-effective alternative by providing tailored coverage with lower premiums and flexible payment options. This approach enhances financial inclusion and ensures essential protection without imposing significant financial burdens.

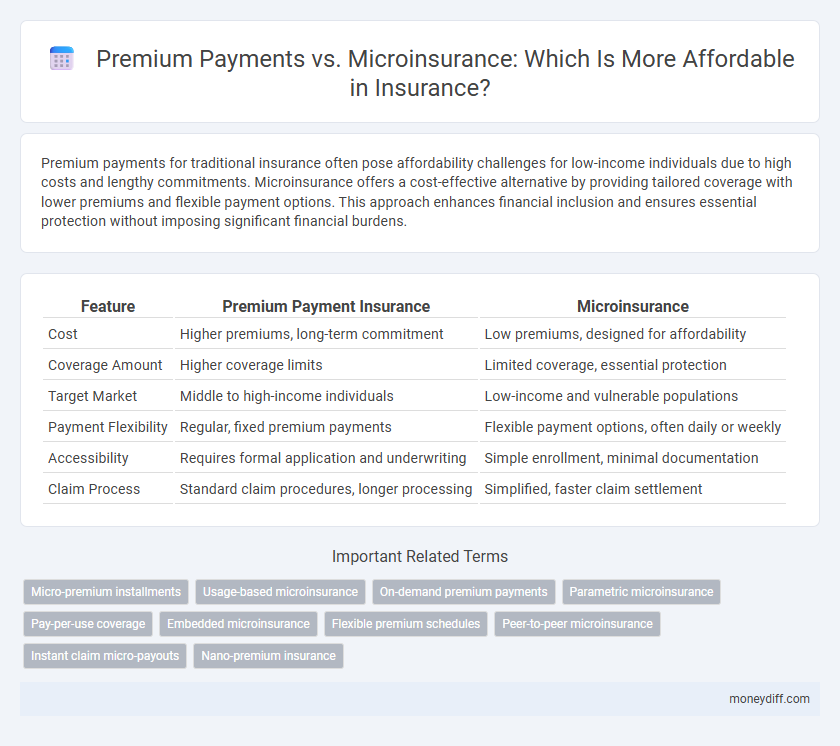

Table of Comparison

| Feature | Premium Payment Insurance | Microinsurance |

|---|---|---|

| Cost | Higher premiums, long-term commitment | Low premiums, designed for affordability |

| Coverage Amount | Higher coverage limits | Limited coverage, essential protection |

| Target Market | Middle to high-income individuals | Low-income and vulnerable populations |

| Payment Flexibility | Regular, fixed premium payments | Flexible payment options, often daily or weekly |

| Accessibility | Requires formal application and underwriting | Simple enrollment, minimal documentation |

| Claim Process | Standard claim procedures, longer processing | Simplified, faster claim settlement |

Understanding Premium Payments in Traditional Insurance

Premium payments in traditional insurance often involve fixed, higher amounts paid regularly, which can limit affordability for low-income individuals. Microinsurance offers a more accessible alternative by providing lower-cost premiums tailored to specific risks and shorter coverage periods. Understanding these payment structures helps consumers choose insurance solutions that best fit their financial capabilities and protection needs.

What is Microinsurance?

Microinsurance provides affordable insurance coverage tailored specifically for low-income populations, offering protection against risks such as health issues, natural disasters, or accidents with lower premium payments compared to traditional insurance. This financial product is designed to bridge the gap for those who cannot afford conventional premiums, ensuring essential security and risk management for vulnerable households. By minimizing premium costs and simplifying coverage terms, microinsurance enhances accessibility and promotes financial inclusion among underserved communities.

Key Differences: Premium Payments vs Microinsurance

Premium payments typically involve higher, fixed costs that require regular financial commitment, making them less affordable for low-income individuals. Microinsurance offers lower premiums with flexible payment options, designed to enhance accessibility and affordability for underserved populations. Key differences include coverage scope, cost structure, and target demographic, where microinsurance emphasizes simplicity and affordability over comprehensive benefits.

Affordability: A Comparative Overview

Premium payment models in traditional insurance often require higher upfront costs and longer-term commitments, limiting affordability for low-income populations. Microinsurance offers lower premiums and flexible payment options, making coverage accessible to underserved communities with modest financial capacity. This comparative affordability drives wider adoption of microinsurance as a viable risk management tool in emerging markets.

How Premium Frequency Affects Insurance Accessibility

Premium frequency significantly influences insurance accessibility by determining the payment structure that policyholders must follow. Microinsurance, with its smaller and more frequent premium payments, enhances affordability for low-income individuals by reducing upfront financial burdens and enabling incremental contributions aligned with income flow. In contrast, traditional insurance often requires larger, less frequent premiums that can limit access for economically vulnerable populations.

Microinsurance: Tailored for Low-Income Households

Microinsurance offers affordable premium payment options specifically designed to meet the needs of low-income households, providing crucial financial protection without imposing substantial economic burdens. Its flexible payment structures and lower coverage amounts enable broader access compared to traditional insurance products, making it a viable solution for financial inclusion. By focusing on essential risks and cost-effective coverage, microinsurance enhances affordability while delivering meaningful benefits to vulnerable populations.

Cost-Benefit Analysis: Traditional Insurance vs Microinsurance

Traditional insurance often involves higher premium payments that may be prohibitive for low-income individuals, while microinsurance offers more affordable options with lower premiums but limited coverage. Cost-benefit analysis reveals that microinsurance provides essential risk protection tailored to the financial capacity of underserved populations, balancing price with benefit accessibility. Insurers and policymakers focus on optimizing coverage features and premium structures in microinsurance to maximize affordability without substantially sacrificing the scope of protection.

Barriers to Premium Payment in Conventional Policies

High premium payments in conventional insurance policies present significant barriers for low-income individuals, limiting their access to crucial financial protection. Microinsurance offers affordable, low-cost premiums tailored for vulnerable populations, enabling wider coverage despite limited resources. Addressing premium payment challenges through microinsurance models enhances inclusivity and mitigates financial risks for underserved communities.

Innovations in Microinsurance for Enhanced Affordability

Innovations in microinsurance leverage mobile technology and data analytics to significantly reduce premium costs, making coverage more accessible to low-income populations. Usage-based models and flexible payment schedules enable clients to pay premiums aligned with their cash flow, enhancing affordability. These advancements address traditional barriers by offering tailored, cost-effective insurance solutions that meet the financial capabilities of underserved communities.

Choosing the Right Insurance Based on Financial Capacity

Premium payment options vary significantly between traditional insurance and microinsurance, impacting affordability for different income groups. Microinsurance offers lower premiums and tailored coverage, making it accessible for low-income individuals who struggle with standard premium payments. Assessing financial capacity and risk exposure ensures the selection of an insurance plan that balances cost-effectiveness with adequate protection.

Related Important Terms

Micro-premium installments

Micro-premium installments in microinsurance significantly enhance affordability by allowing policyholders to pay smaller, manageable amounts frequently, reducing financial strain compared to traditional lump-sum premium payments. This flexible payment structure increases accessibility for low-income individuals, promoting broader coverage and financial inclusion in underserved communities.

Usage-based microinsurance

Usage-based microinsurance leverages real-time data from devices like telematics and smartphones to tailor premium payments according to individual risk profiles and usage patterns, significantly enhancing affordability for low-income consumers. This model reduces upfront costs by aligning premiums with actual behavior, making insurance accessible to underserved populations who otherwise face barriers due to traditional fixed premium structures.

On-demand premium payments

On-demand premium payments in microinsurance offer flexible affordability by allowing policyholders to pay premiums only when needed, reducing financial strain compared to traditional fixed premium schedules. This approach enhances access to insurance for low-income individuals by aligning payments with their irregular income patterns, thereby improving coverage continuity and risk protection.

Parametric microinsurance

Parametric microinsurance offers a cost-effective alternative to traditional premium payment models by triggering automatic payouts based on predefined parameters, reducing administrative expenses and making coverage more affordable for low-income populations. This approach enhances financial inclusion by providing timely, transparent protection against risks such as natural disasters, without the complexities and delays of claims assessment.

Pay-per-use coverage

Pay-per-use coverage in microinsurance enhances affordability by allowing policyholders to pay premiums based only on their actual usage or exposure, significantly reducing upfront costs compared to traditional fixed-premium models. This flexible payment approach aligns insurance expenses with real-time risk, making protection accessible to low-income individuals who might otherwise forgo coverage due to financial constraints.

Embedded microinsurance

Embedded microinsurance integrates premium payments seamlessly into everyday transactions, significantly enhancing affordability by reducing upfront costs and simplifying access for low-income consumers. This model leverages digital platforms and partnerships with retailers or service providers to embed coverage in routine purchases, making insurance more inclusive and financially manageable.

Flexible premium schedules

Flexible premium schedules in microinsurance enhance affordability by allowing policyholders to pay in small, manageable installments aligned with their income cycles, reducing financial strain. This adaptability contrasts with traditional insurance premium payments that often require lump sums, making microinsurance a practical option for low-income populations seeking consistent coverage.

Peer-to-peer microinsurance

Peer-to-peer microinsurance significantly enhances affordability by pooling small premiums from community members, lowering individual costs compared to traditional premium payments in conventional insurance models. This decentralized approach mitigates administrative expenses and fosters trust among policyholders, making financial protection accessible to low-income populations.

Instant claim micro-payouts

Instant claim micro-payouts revolutionize affordability in insurance by providing small, rapid payments that reduce premium burdens and enhance accessibility for low-income individuals. This approach ensures timely financial support without the strain of large premium payments, making insurance more inclusive and practical.

Nano-premium insurance

Nano-premium insurance offers ultra-low premium payments designed to enhance affordability and financial inclusion for low-income individuals, addressing the limitations often seen in traditional premium payment models. By enabling microinsurance coverage with minimal financial barriers, it supports wider access to essential protection without compromising policy benefits.

Premium payment vs Microinsurance for affordability. Infographic