Traditional car insurance offers fixed premiums based on factors like age, driving history, and vehicle type, providing consistent coverage regardless of miles driven. Pay-per-mile car insurance calculates costs according to the actual distance driven, making it a cost-effective option for low-mileage drivers seeking personalized coverage. Comparing these options helps drivers choose the best value by balancing coverage needs with driving habits.

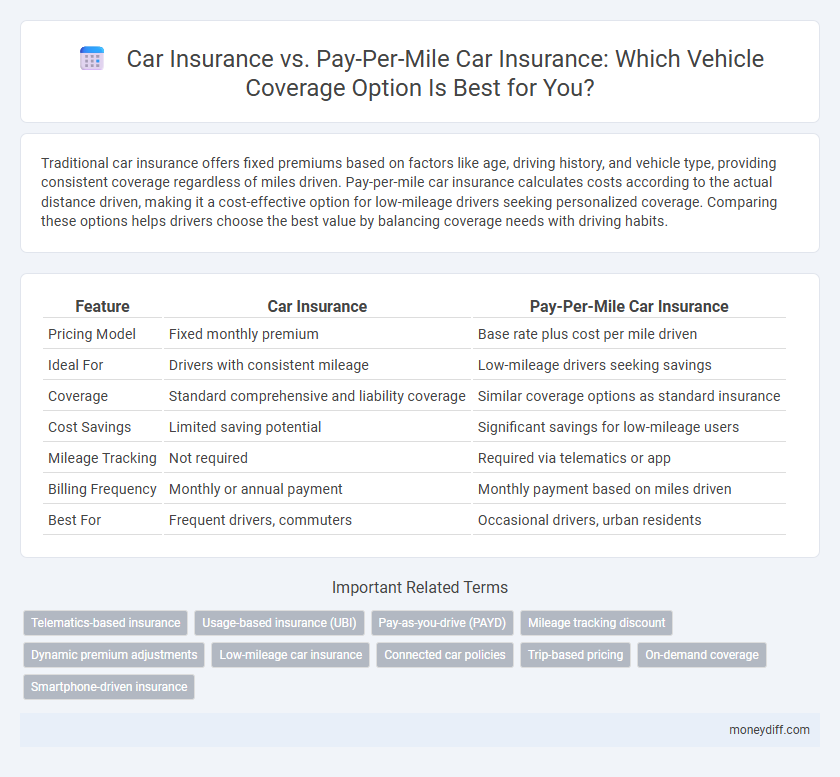

Table of Comparison

| Feature | Car Insurance | Pay-Per-Mile Car Insurance |

|---|---|---|

| Pricing Model | Fixed monthly premium | Base rate plus cost per mile driven |

| Ideal For | Drivers with consistent mileage | Low-mileage drivers seeking savings |

| Coverage | Standard comprehensive and liability coverage | Similar coverage options as standard insurance |

| Cost Savings | Limited saving potential | Significant savings for low-mileage users |

| Mileage Tracking | Not required | Required via telematics or app |

| Billing Frequency | Monthly or annual payment | Monthly payment based on miles driven |

| Best For | Frequent drivers, commuters | Occasional drivers, urban residents |

Understanding Traditional Car Insurance

Traditional car insurance provides comprehensive coverage, including collision, liability, and uninsured motorist protection, with premiums based on factors such as driving history, vehicle type, and annual mileage estimates. This model offers predictable monthly or annual payments regardless of actual miles driven, making it suitable for individuals with consistent driving patterns. Understanding policy terms and coverage limits is essential to ensure adequate protection and cost efficiency.

What Is Pay-Per-Mile Car Insurance?

Pay-per-mile car insurance charges drivers based on the exact number of miles they drive, offering a cost-effective alternative to traditional fixed-rate policies for low-mileage drivers. This coverage model uses a telematics device or smartphone app to track mileage, ensuring premiums align directly with actual road usage. Pay-per-mile insurance is ideal for individuals who drive infrequently or commute short distances, promoting savings and personalized vehicle coverage.

Key Differences Between Traditional and Pay-Per-Mile Policies

Traditional car insurance typically charges a fixed premium based on estimated annual mileage, driving history, and vehicle type, offering consistent coverage regardless of actual usage. Pay-per-mile car insurance calculates costs directly from the miles driven, providing cost savings for low-mileage drivers through metered billing and usage tracking technology. Key differences include pricing structure, billing methods, and suitability for varying driving habits, impacting overall affordability and customization in vehicle coverage.

Cost Comparison: Which Is More Affordable?

Pay-per-mile car insurance often proves more affordable for drivers with low annual mileage, as premiums are based on actual miles driven rather than estimated usage. Traditional car insurance typically involves fixed monthly rates that may result in higher costs for infrequent drivers due to standard risk assessments. Evaluating average yearly mileage and driving habits helps determine whether mileage-based pricing or flat-rate policies offer better financial savings.

Coverage Options: Similarities and Differences

Car insurance and pay-per-mile car insurance both offer liability, collision, and comprehensive coverage, but pay-per-mile plans typically include flexible mileage-based premiums that can lower costs for infrequent drivers. Standard car insurance often provides a broader range of add-ons like rental reimbursement and roadside assistance regardless of mileage. The key difference lies in how premiums are calculated, with pay-per-mile policies linking costs directly to actual miles driven, making it ideal for low-mileage vehicle coverage.

Who Should Consider Pay-Per-Mile Insurance?

Pay-per-mile car insurance offers significant savings for low-mileage drivers, such as those who primarily work from home or use their vehicle only for short trips. This model benefits urban residents, retirees, and second-car owners who log fewer miles annually compared to traditional policyholders. Policyholders seeking customized, usage-based coverage to align premiums directly with actual driving behavior should consider pay-per-mile insurance.

Pros and Cons of Traditional Car Insurance

Traditional car insurance offers comprehensive coverage with predictable monthly premiums, providing extensive protection against accidents, theft, and liability. However, higher costs can result from flat-rate pricing regardless of actual driving behavior, making it less economical for low-mileage drivers. Policyholders may benefit from additional perks like roadside assistance and rental car reimbursement, but should weigh these against potentially inflated expenses.

Pros and Cons of Pay-Per-Mile Car Insurance

Pay-per-mile car insurance offers cost savings for low-mileage drivers by charging premiums based on actual miles driven, promoting fair pricing and potentially reducing unnecessary expenses. However, it may lead to higher overall costs for frequent drivers and requires accurate mileage tracking, raising privacy concerns. This model suits occasional drivers seeking customized coverage but may be less advantageous for those with daily commutes or high annual mileage.

Factors to Consider When Choosing Car Insurance

Choosing between traditional car insurance and pay-per-mile car insurance depends heavily on annual mileage, driving habits, and budget constraints. Pay-per-mile insurance typically benefits low-mileage drivers by lowering premiums based on actual miles driven, while traditional policies may offer broader coverage and fixed rates. Key factors to consider include average miles driven per year, type of coverage needed, and potential cost savings from usage-based pricing models.

How to Switch Between Car Insurance Types

To switch between traditional car insurance and pay-per-mile car insurance, start by evaluating your annual mileage and driving habits to determine which plan offers better cost savings. Contact your current insurance provider to inquire about policy adjustments or request a new quote for the pay-per-mile option, ensuring coverage limits and deductibles meet your needs. Finally, cancel your old policy only after confirming the new policy is active to avoid any lapse in coverage and potential penalties.

Related Important Terms

Telematics-based insurance

Telematics-based car insurance leverages real-time driving data through GPS and onboard diagnostics to offer personalized premiums, contrasting with traditional pay-per-mile insurance models that charge solely based on distance driven. This technology enhances risk assessment by incorporating factors like driving behavior, speed, and braking patterns, resulting in more accurate vehicle coverage and potential cost savings for safe drivers.

Usage-based insurance (UBI)

Usage-based insurance (UBI) models, including pay-per-mile car insurance, offer personalized vehicle coverage by tracking actual driving behavior and mileage through telematics, resulting in potentially lower premiums compared to traditional car insurance. These plans benefit low-mileage drivers by aligning insurance costs with real-time usage patterns, promoting safer driving habits and cost efficiency.

Pay-as-you-drive (PAYD)

Pay-as-you-drive (PAYD) car insurance offers significant savings by charging premiums based on the actual miles driven, making it ideal for low-mileage drivers seeking cost-effective vehicle coverage. This model utilizes telematics to provide personalized rates that reflect driving behavior and mileage, enhancing affordability compared to traditional car insurance policies with fixed premiums.

Mileage tracking discount

Pay-per-mile car insurance offers significant savings for low-mileage drivers by tracking actual miles driven and calculating premiums based on usage, rather than a fixed rate. Traditional car insurance typically charges a higher flat premium regardless of mileage, missing opportunities for discounts that mileage tracking can provide.

Dynamic premium adjustments

Dynamic premium adjustments in car insurance allow traditional policies to update rates based on factors like driving history and claims frequency, whereas pay-per-mile car insurance directly ties premiums to the exact miles driven, offering more precise cost control and potential savings for low-mileage drivers. This flexibility in pricing models enhances personalized coverage, promoting cost efficiency and encouraging safer driving habits.

Low-mileage car insurance

Pay-per-mile car insurance offers significant savings for low-mileage drivers by charging premiums based on actual miles driven, unlike traditional car insurance with fixed rates. This usage-based model provides cost-effective coverage, especially for individuals who drive less than 10,000 miles annually, reducing overall insurance expenses while maintaining comprehensive protection.

Connected car policies

Connected car policies use telematics technology to monitor driving behavior, offering personalized pay-per-mile car insurance rates that can result in significant savings for low-mileage drivers compared to traditional car insurance. This data-driven approach enhances risk assessment accuracy and supports dynamic pricing models, making coverage more affordable and tailored to individual usage patterns.

Trip-based pricing

Pay-per-mile car insurance offers a trip-based pricing model that charges drivers accurately based on the exact miles they drive, potentially lowering costs for low-mileage motorists compared to traditional car insurance, which typically uses fixed premiums regardless of actual vehicle use. This usage-based approach incentivizes careful driving habits and provides flexibility, making it an attractive option for urban commuters and infrequent drivers seeking tailored vehicle coverage.

On-demand coverage

Pay-per-mile car insurance offers flexible, on-demand coverage by charging premiums based on the actual miles driven, providing significant cost savings for low-mileage drivers compared to traditional car insurance with fixed rates. This usage-based model enhances affordability and ensures tailored protection that aligns with individual driving habits.

Smartphone-driven insurance

Smartphone-driven pay-per-mile car insurance leverages telematics to track actual miles driven, offering personalized premiums that can significantly lower costs for low-mileage drivers compared to traditional car insurance's fixed-rate models. This technology enhances transparency and allows insurers to evaluate risk more accurately, promoting fairer pricing and flexible coverage options based on real-time driving behavior.

Car insurance vs Pay-per-mile car insurance for vehicle coverage. Infographic