Critical illness insurance offers broad protection by covering multiple serious diseases under one policy, providing financial support regardless of the specific illness diagnosed. Disease-specific insurance targets coverage for particular conditions such as cancer or heart disease, often resulting in lower premiums but limited scope. Choosing between the two depends on individual risk factors, budget, and the desire for comprehensive versus focused illness protection.

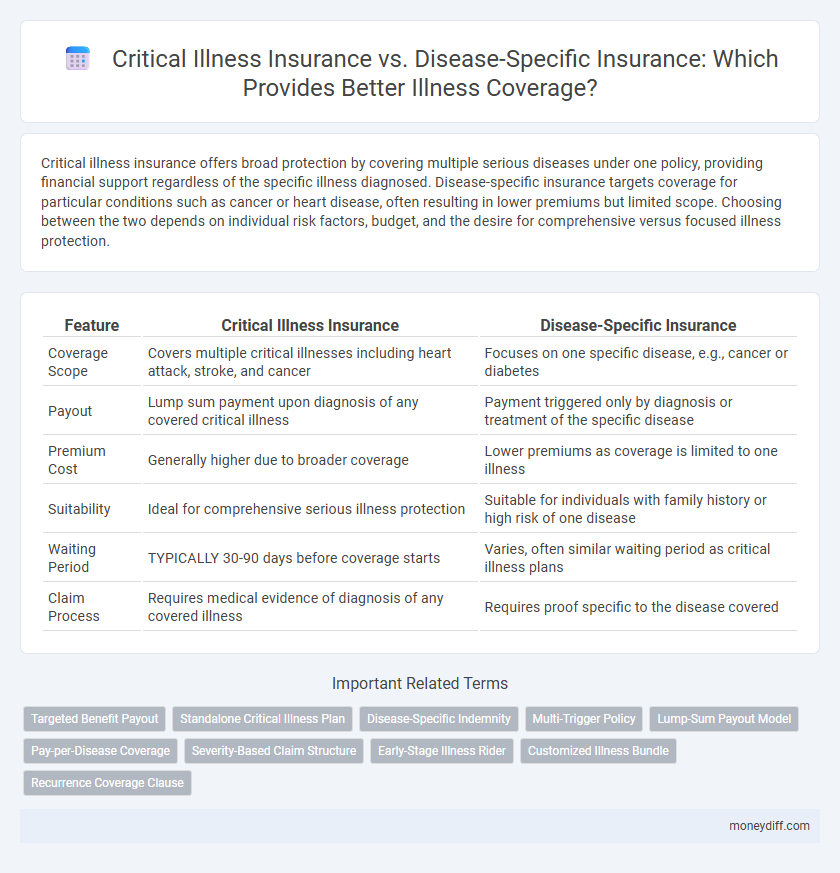

Table of Comparison

| Feature | Critical Illness Insurance | Disease-Specific Insurance |

|---|---|---|

| Coverage Scope | Covers multiple critical illnesses including heart attack, stroke, and cancer | Focuses on one specific disease, e.g., cancer or diabetes |

| Payout | Lump sum payment upon diagnosis of any covered critical illness | Payment triggered only by diagnosis or treatment of the specific disease |

| Premium Cost | Generally higher due to broader coverage | Lower premiums as coverage is limited to one illness |

| Suitability | Ideal for comprehensive serious illness protection | Suitable for individuals with family history or high risk of one disease |

| Waiting Period | TYPICALLY 30-90 days before coverage starts | Varies, often similar waiting period as critical illness plans |

| Claim Process | Requires medical evidence of diagnosis of any covered illness | Requires proof specific to the disease covered |

Understanding Critical Illness Insurance

Critical illness insurance offers broad financial protection by covering multiple severe health conditions defined in the policy, such as cancer, heart attack, and stroke, providing a lump-sum benefit upon diagnosis. Disease-specific insurance targets a single illness, like cancer-only insurance, limiting coverage but often reducing premiums for focused needs. Understanding critical illness insurance is crucial for comprehensive coverage, as it addresses a range of serious diseases, minimizing financial risk from unexpected medical costs.

What Is Disease-Specific Insurance?

Disease-specific insurance provides coverage exclusively for one particular illness, such as cancer, heart disease, or stroke, allowing policyholders to receive targeted financial support for diagnosis and treatment of that specific condition. Unlike critical illness insurance, which offers a lump sum payment upon diagnosis of any covered critical illness, disease-specific policies concentrate benefits on a narrowly defined medical condition, often resulting in more affordable premiums. This specialization helps individuals with a family history or high risk of a particular disease manage healthcare costs with focused protection tailored to their needs.

Key Differences Between Critical Illness and Disease-Specific Insurance

Critical illness insurance provides a lump-sum payout upon diagnosis of a range of major illnesses such as cancer, heart attack, and stroke, offering broad coverage that helps cover various medical and living expenses. Disease-specific insurance focuses exclusively on one particular illness, like cancer insurance or diabetes insurance, delivering targeted financial support tailored to the costs associated with that specific condition. The key difference lies in the scope: critical illness insurance offers comprehensive protection across multiple diseases, while disease-specific insurance delivers specialized, focused coverage for higher-risk or prevalent conditions.

Coverage Scope: Broad vs. Focused Protection

Critical illness insurance offers broad protection by covering multiple serious health conditions such as cancer, heart attack, and stroke under a single policy, providing financial security against a range of major illnesses. Disease-specific insurance targets a particular illness like cancer or diabetes, delivering focused coverage that often includes specialized treatments and benefits tailored to that condition. Choosing between broad and focused protection depends on individual risk factors and healthcare needs, balancing comprehensive coverage against targeted support for a specific disease.

Premium Comparisons: Which Is More Cost-Effective?

Critical illness insurance generally offers broader coverage for multiple conditions under a single policy, often resulting in higher premiums compared to disease-specific insurance, which targets one illness, such as cancer or diabetes. Disease-specific insurance usually comes with lower premiums due to its limited scope, making it more cost-effective for individuals with a family history or high risk of that particular illness. Evaluating personal health risks and coverage needs is crucial to determine whether the comprehensive protection of critical illness insurance justifies the higher premium or if the specialized, budget-friendly disease-specific plan is a better financial choice.

Claim Process: Simplicity and Speed

Critical illness insurance offers a streamlined claim process with lump-sum payouts upon diagnosis of covered conditions, minimizing paperwork and enabling faster financial support. Disease-specific insurance often requires detailed medical documentation and proof of diagnosis related to a particular illness, which can extend the claim approval timeline. Understanding these differences helps policyholders choose coverage that suits their need for claim simplicity and quick access to benefits.

Flexibility of Payouts and Policy Benefits

Critical illness insurance offers broader flexibility in payouts by covering multiple serious conditions under a single policy, allowing policyholders to receive lump-sum payments tailored to various illnesses. Disease-specific insurance provides targeted benefits with tailored coverage for one illness, often resulting in more specialized but limited payout options. Choosing between the two depends on whether one values comprehensive protection and adaptable benefits or prefers focused coverage with potentially higher benefits for a specific disease.

Suitability for Different Life Stages and Health Profiles

Critical illness insurance offers broad coverage ideal for individuals seeking protection against multiple severe health conditions, making it suitable for those with varied health risks or family history. Disease-specific insurance targets particular illnesses such as cancer or diabetes, providing more focused benefits that align with diagnosed risk factors or pre-existing conditions, often preferred by individuals with known vulnerabilities. Choosing between these options depends on life stage and health profile, where younger, healthier individuals may benefit from comprehensive critical illness plans, while those with specific health concerns may find disease-specific insurance more cost-effective and tailored.

Exclusions and Waiting Periods Explained

Critical illness insurance typically covers a broad range of serious conditions but often excludes pre-existing diseases and less common ailments, with waiting periods ranging from 30 to 90 days before coverage begins. Disease-specific insurance targets one illness, such as cancer or stroke, usually featuring shorter or no waiting periods but includes exclusions related to disease severity or recurrence. Understanding these differences helps policyholders select coverage that balances comprehensive protection and timely benefits.

How to Choose the Best Insurance for Your Needs

Evaluate your health risks and family medical history to decide between critical illness insurance, which offers broad coverage for multiple major illnesses, and disease-specific insurance that targets singular conditions like cancer or heart disease. Consider the premium costs, coverage limits, and payout structures to ensure the policy aligns with your financial capacity and expected medical needs. Review policy terms carefully for waiting periods, exclusions, and claim procedures to make an informed decision tailored to your personal health profile.

Related Important Terms

Targeted Benefit Payout

Critical illness insurance provides a lump-sum payout upon diagnosis of a broad range of major health conditions, offering flexible financial support for diverse medical expenses. Disease-specific insurance targets a particular illness, such as cancer or heart disease, delivering focused benefits that cover specialized treatments and related costs specific to that condition.

Standalone Critical Illness Plan

Standalone critical illness plans provide comprehensive coverage by offering a lump-sum benefit upon diagnosis of specified major illnesses, whereas disease-specific insurance targets only one particular condition, limiting the scope of financial protection. These standalone policies are designed to cover multiple critical diseases such as cancer, heart attack, and stroke, ensuring broader support during medical emergencies compared to narrow, condition-specific plans.

Disease-Specific Indemnity

Disease-specific indemnity insurance provides targeted financial protection by paying a fixed benefit upon diagnosis of particular illnesses such as cancer, stroke, or heart attack, ensuring straightforward claims without the complexities of treatment costs. Unlike critical illness insurance, which covers a broader range of conditions with variable payouts, disease-specific plans offer focused coverage, often at lower premiums, making them suitable for policyholders concerned about specific health risks.

Multi-Trigger Policy

Critical illness insurance offers broad coverage by providing a lump sum upon diagnosis of any of the multiple specified severe conditions, whereas disease-specific insurance targets coverage for a single illness, such as cancer or heart disease. Multi-trigger policies enhance protection by covering several qualifying illnesses or stages within a condition, increasing flexibility and financial support compared to single-disease plans.

Lump-Sum Payout Model

Critical illness insurance offers a lump-sum payout upon diagnosis of any covered serious conditions, providing broad financial protection across multiple illnesses, while disease-specific insurance delivers a lump sum only for a particular illness, optimizing coverage and benefits for individuals with known health risks. The lump-sum payout model in critical illness insurance enables flexible use of funds for medical expenses or income replacement, contrasting with disease-specific plans that target specialized treatment costs and related financial needs for one condition.

Pay-per-Disease Coverage

Critical illness insurance offers lump-sum payouts upon diagnosis of a broad range of serious diseases, providing flexible financial support, while pay-per-disease insurance covers specific illnesses individually, allowing policyholders to tailor coverage and premiums according to distinct health risks. Selecting pay-per-disease coverage enables focused protection and cost-efficiency by targeting prevalent conditions like cancer or stroke without paying for unnecessary blanket coverage.

Severity-Based Claim Structure

Critical illness insurance offers a severity-based claim structure that provides lump-sum payouts upon diagnosis of major illnesses, covering a broad range of conditions with payouts varying based on the severity of the illness. Disease-specific insurance targets one particular illness, offering tailored benefits that often include staged payments aligned with the progression and severity of that disease, ensuring focused financial support for treatment and recovery.

Early-Stage Illness Rider

Critical illness insurance offers broad coverage for multiple major diseases, while disease-specific insurance targets protection for a single illness, often at a lower premium. Adding an Early-Stage Illness Rider enhances both policies by providing financial support during the initial diagnosis phase, improving early intervention and treatment outcomes.

Customized Illness Bundle

Critical illness insurance offers broad coverage for multiple severe health conditions under a single policy, while disease-specific insurance targets protection for a particular illness such as cancer or stroke. Customized illness bundles combine these approaches by tailoring coverage to an individual's risk profile, ensuring comprehensive financial support for both general critical conditions and specific diseases.

Recurrence Coverage Clause

Critical illness insurance typically includes a recurrence coverage clause that provides benefits if the same illness returns, offering broader protection across multiple serious conditions, whereas disease-specific insurance focuses on one particular illness with coverage primarily limited to initial diagnosis and treatment. Recurrence coverage in critical illness policies ensures continued financial support during subsequent episodes of the covered illnesses, which is often absent or limited in disease-specific plans.

Critical illness insurance vs Disease-specific insurance for illness coverage. Infographic