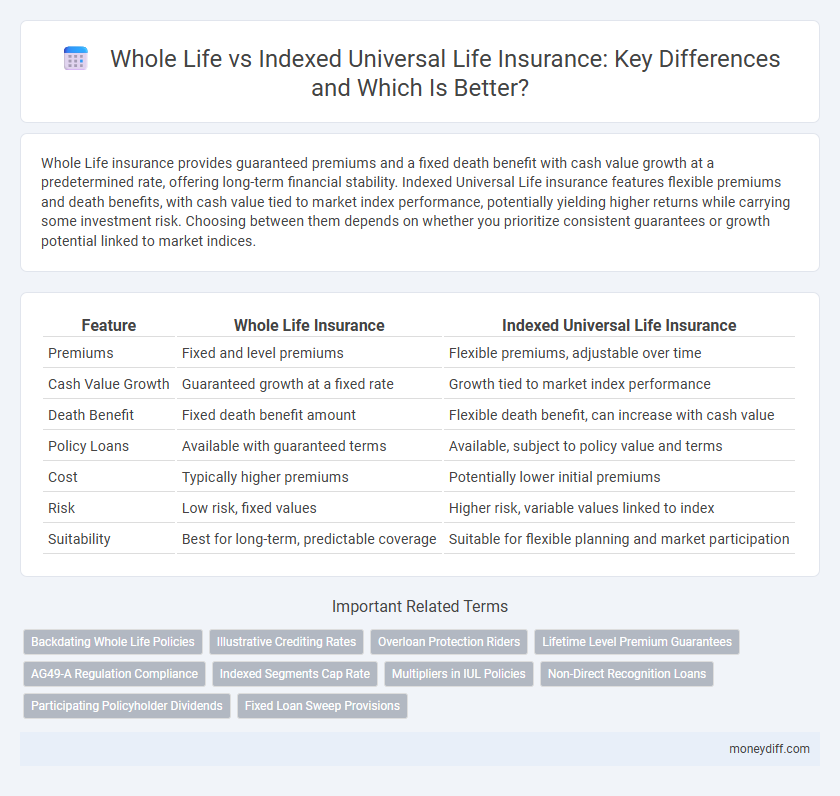

Whole Life insurance provides guaranteed premiums and a fixed death benefit with cash value growth at a predetermined rate, offering long-term financial stability. Indexed Universal Life insurance features flexible premiums and death benefits, with cash value tied to market index performance, potentially yielding higher returns while carrying some investment risk. Choosing between them depends on whether you prioritize consistent guarantees or growth potential linked to market indices.

Table of Comparison

| Feature | Whole Life Insurance | Indexed Universal Life Insurance |

|---|---|---|

| Premiums | Fixed and level premiums | Flexible premiums, adjustable over time |

| Cash Value Growth | Guaranteed growth at a fixed rate | Growth tied to market index performance |

| Death Benefit | Fixed death benefit amount | Flexible death benefit, can increase with cash value |

| Policy Loans | Available with guaranteed terms | Available, subject to policy value and terms |

| Cost | Typically higher premiums | Potentially lower initial premiums |

| Risk | Low risk, fixed values | Higher risk, variable values linked to index |

| Suitability | Best for long-term, predictable coverage | Suitable for flexible planning and market participation |

Understanding Whole Life and Indexed Universal Insurance

Whole Life insurance provides guaranteed death benefits, fixed premiums, and cash value growth at a guaranteed minimum rate, offering stability and predictability. Indexed Universal Life (IUL) insurance features flexible premiums, death benefits, and cash value tied to a market index like the S&P 500, allowing for potential higher returns with downside protection. Understanding these differences helps policyholders align their insurance choices with long-term financial goals and risk tolerance.

Key Features of Whole Life Insurance

Whole Life Insurance guarantees lifelong coverage with fixed premiums and a guaranteed death benefit, making it a reliable financial safety net. Its cash value grows at a guaranteed rate, offering stable accumulation and the ability to borrow against the policy. Policyholders benefit from predictable costs and consistent growth, providing long-term financial security without market risk.

Core Benefits of Indexed Universal Life Insurance

Indexed Universal Life Insurance offers flexible premium payments, adjustable death benefits, and the potential for cash value growth linked to a market index, providing policyholders opportunities for higher returns compared to Whole Life insurance. The cash value accumulation is tax-deferred, and policyholders can access funds through loans or withdrawals, enhancing liquidity and financial planning options. These features combine to create a tailored insurance solution that balances protection and investment growth aligned with market performance.

Premium Structures: Whole Life vs Indexed Universal

Whole Life insurance features fixed premiums that remain level throughout the policyholder's lifetime, providing predictable cost management. Indexed Universal Life (IUL) insurance offers flexible premiums that can be adjusted within certain limits, allowing policyholders to increase or decrease payments based on financial needs and market conditions. The premium flexibility in IUL policies can enable optimizing cash value growth tied to market indexes, while Whole Life premiums prioritize stability and long-term planning.

Cash Value Accumulation Compared

Whole Life insurance offers guaranteed cash value accumulation with fixed premiums and a stable growth rate tied to the insurer's portfolio performance, ensuring predictable growth over time. Indexed Universal Life (IUL) insurance links cash value growth to a stock market index, such as the S&P 500, providing higher growth potential but with capped returns and no direct stock market risk. Policyholders seeking conservative, steady cash value may prefer Whole Life, while those aiming for greater cash value growth with market-based upside might favor Indexed Universal Life.

Flexibility and Customization Options

Whole Life insurance offers guaranteed premiums and fixed cash value growth with limited flexibility, making it ideal for policyholders seeking stability and predictability. Indexed Universal Life insurance provides flexible premium payments and adjustable death benefits, allowing customization based on changing financial needs and market performance. Policyholders can tailor Indexed Universal Life policies to optimize cash value accumulation and death benefit amounts, offering greater adaptability compared to Whole Life coverage.

Policy Loans and Withdrawals: How They Differ

Whole Life insurance offers fixed cash value growth with predictable policy loan interest rates, allowing for stable borrowing against the cash value without affecting the death benefit if loans are repaid. Indexed Universal Life insurance provides flexible loan and withdrawal options tied to market index performance, with variable interest rates and potential impacts on cash value and death benefits. Policyholders must consider the trade-offs between guaranteed growth and flexibility in loans and withdrawals when choosing between these types.

Cost Analysis: Which Policy is More Affordable?

Whole Life insurance features fixed premiums and predictable costs, making it more affordable for long-term budget planning compared to Indexed Universal Life (IUL) policies, which have flexible premiums but can vary significantly based on market index performance. IUL policies may appear initially lower in cost but can become expensive due to rising premiums when cash value growth underperforms. A comprehensive cost analysis reveals that Whole Life provides stable, manageable expenses, whereas Indexed Universal Life requires careful monitoring to avoid unexpected cost increases.

Suitability: Who Should Choose Each Policy?

Whole Life insurance suits individuals seeking guaranteed lifelong coverage with stable premiums and predictable cash value growth, ideal for conservative investors prioritizing financial security. Indexed Universal Life insurance appeals to policyholders comfortable with market-linked cash value potential, offering flexible premiums and death benefits suitable for those desiring growth opportunities and adaptability. Understanding personal risk tolerance, financial goals, and long-term planning needs is essential when choosing between these two insurance products.

Making the Right Choice: Factors to Consider

When choosing between Whole Life and Indexed Universal Life insurance, focus on factors like premium stability, cash value growth potential, and risk tolerance. Whole Life offers guaranteed premiums and steady cash value accumulation, while Indexed Universal Life provides flexible premiums with growth linked to market indices but carries more variability. Evaluate your long-term financial goals, desire for policy flexibility, and comfort with market fluctuations to make the right decision.

Related Important Terms

Backdating Whole Life Policies

Backdating whole life policies allows policyholders to establish an earlier policy effective date, increasing cash value accumulation compared to indexed universal life insurance, which focuses more on flexible premiums and market-indexed growth. Whole life backdating can also lock in lower premiums based on the insured's younger age, creating long-term cost advantages not typically available with indexed universal policies.

Illustrative Crediting Rates

Whole Life insurance offers guaranteed cash value growth with fixed interest rates, providing stability and predictability in illustrative crediting rates. Indexed Universal Life insurance credits interest based on stock market index performance, potentially yielding higher returns but with variable illustrative crediting rates tied to market fluctuations.

Overloan Protection Riders

Whole Life insurance policies offer Overloan Protection Riders that safeguard the policy's cash value and death benefit from reduction due to loan overages, ensuring long-term financial security. Indexed Universal Life insurance also provides similar riders, but they typically include flexible premium options and potential cash value growth linked to market indexes, balancing protection with investment opportunity.

Lifetime Level Premium Guarantees

Whole Life insurance provides lifetime level premium guarantees, ensuring stable payments throughout the policyholder's life without risk of increase. Indexed Universal Life insurance offers flexible premiums and potential cash value growth linked to market indexes but typically lacks guaranteed level premiums, posing possible premium adjustments over time.

AG49-A Regulation Compliance

Whole Life insurance provides guaranteed cash value growth and fixed premiums, ensuring AG49-A regulation compliance by maintaining conservative dividend scales and reserves. Indexed Universal Life insurance offers potential cash value linked to market indexes but requires strict policy design and actuarial reviews to meet AG49-A guidelines on interest crediting and lapse-supported reserves.

Indexed Segments Cap Rate

Indexed Universal Life insurance offers flexible premiums and cash value growth linked to market indexes, with Indexed Segments typically subject to a Cap Rate that limits maximum returns to protect against market downturns. Whole Life insurance provides guaranteed cash value growth without caps, but lacks the potential upside tied to indexed market performance found in Indexed Universal policies.

Multipliers in IUL Policies

Indexed Universal Life (IUL) insurance policies often feature multipliers that can significantly enhance the credited interest based on the performance of a specified market index, offering the potential for higher cash value growth compared to Whole Life insurance, which typically provides fixed dividends. These multipliers in IUL policies magnify returns during favorable market conditions, making them attractive for policyholders seeking a balance between growth potential and life insurance protection.

Non-Direct Recognition Loans

Whole Life insurance offers guaranteed cash value growth with stable premiums, while Indexed Universal Life provides flexible premiums and potential for higher cash value through market index-linked interest. Non-Direct Recognition loans in Indexed Universal Life policies allow policyholders to borrow against cash value without reducing credited interest, maximizing growth potential during loan periods.

Participating Policyholder Dividends

Whole Life insurance policies often provide participating policyholder dividends derived from the insurer's surplus, offering potential cash value growth and premium reduction, whereas Indexed Universal Life policies typically do not pay dividends but instead accumulate cash value linked to market indexes. Participating dividends in Whole Life can enhance policyholder returns by reflecting company performance, adding a layer of financial benefit beyond guaranteed cash values.

Fixed Loan Sweep Provisions

Whole Life insurance offers guaranteed fixed loan sweep provisions with stable cash value growth, ensuring predictable loan repayment without market risk exposure. Indexed Universal Life insurance features variable loan sweep options tied to market indexes, allowing flexible policy adjustments but with potential fluctuations in repayment and cash value.

Whole Life vs Indexed Universal for insurance. Infographic