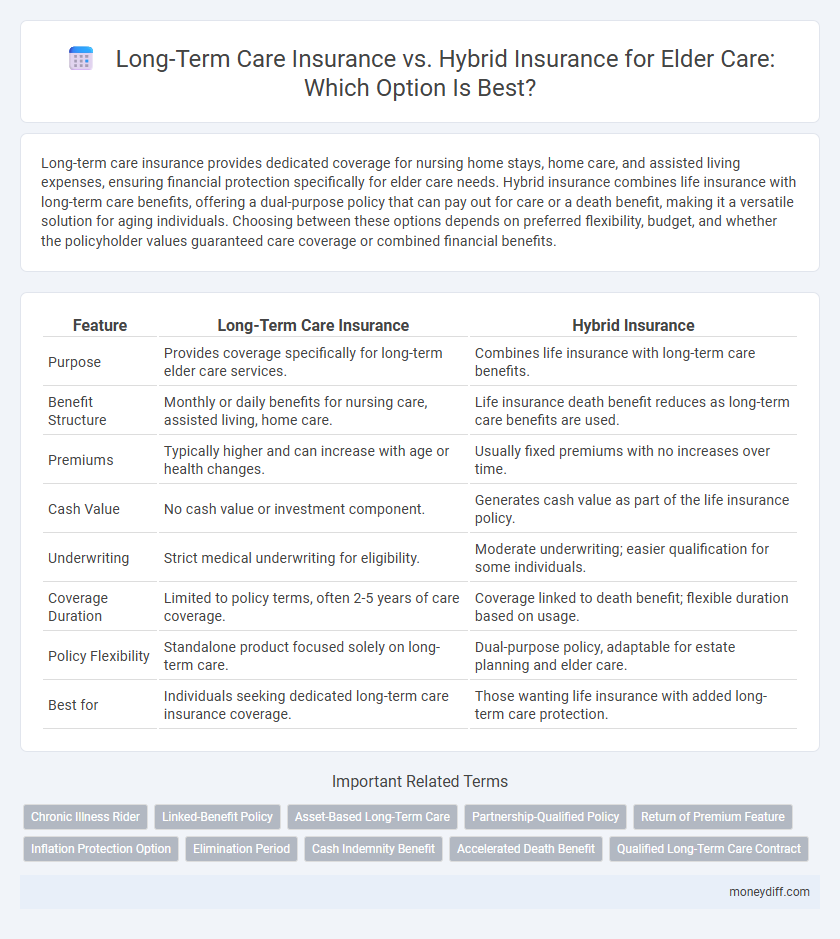

Long-term care insurance provides dedicated coverage for nursing home stays, home care, and assisted living expenses, ensuring financial protection specifically for elder care needs. Hybrid insurance combines life insurance with long-term care benefits, offering a dual-purpose policy that can pay out for care or a death benefit, making it a versatile solution for aging individuals. Choosing between these options depends on preferred flexibility, budget, and whether the policyholder values guaranteed care coverage or combined financial benefits.

Table of Comparison

| Feature | Long-Term Care Insurance | Hybrid Insurance |

|---|---|---|

| Purpose | Provides coverage specifically for long-term elder care services. | Combines life insurance with long-term care benefits. |

| Benefit Structure | Monthly or daily benefits for nursing care, assisted living, home care. | Life insurance death benefit reduces as long-term care benefits are used. |

| Premiums | Typically higher and can increase with age or health changes. | Usually fixed premiums with no increases over time. |

| Cash Value | No cash value or investment component. | Generates cash value as part of the life insurance policy. |

| Underwriting | Strict medical underwriting for eligibility. | Moderate underwriting; easier qualification for some individuals. |

| Coverage Duration | Limited to policy terms, often 2-5 years of care coverage. | Coverage linked to death benefit; flexible duration based on usage. |

| Policy Flexibility | Standalone product focused solely on long-term care. | Dual-purpose policy, adaptable for estate planning and elder care. |

| Best for | Individuals seeking dedicated long-term care insurance coverage. | Those wanting life insurance with added long-term care protection. |

Understanding Long-Term Care Insurance

Long-term care insurance provides dedicated coverage for nursing home stays, assisted living, and in-home care services, helping to protect assets from the high costs of extended elder care. Hybrid insurance combines life insurance benefits with long-term care coverage, offering flexibility but often at a higher cost and more complex terms. Understanding the differences in policy structure, payout triggers, and premium stability is crucial for selecting the most effective elder care insurance solution.

What Is Hybrid Insurance for Elder Care?

Hybrid insurance for elder care combines long-term care coverage with a life insurance policy, offering financial protection for both chronic care needs and beneficiaries upon the policyholder's death. This integrated approach allows policyholders to access funds for caregiving expenses if needed, while ensuring a death benefit is paid out if long-term care is not utilized. Hybrid insurance often appeals to those seeking flexibility and value, blending asset protection with elder care planning.

Key Features: Long-Term Care vs Hybrid Insurance

Long-term care insurance provides dedicated coverage exclusively for extended elder care services, including nursing home stays, home health care, and assisted living, often featuring tax-advantaged benefits and inflation protection. Hybrid insurance combines life insurance or annuities with long-term care benefits, allowing policyholders to access funds for elder care while preserving a death benefit for beneficiaries. Key differentiators include premium stability and benefit flexibility in hybrid policies versus specialized, standalone coverage with potentially higher costs and limited cash value in traditional long-term care insurance.

Cost Comparison: Premiums and Affordability

Long-term care insurance typically involves higher premiums due to comprehensive coverage for extended elder care needs, often resulting in affordability challenges for some applicants. Hybrid insurance policies, combining life insurance with long-term care benefits, generally offer more stable and potentially lower premium costs while providing flexible payout options. Cost comparisons highlight that hybrid insurance can serve as a more budget-friendly solution for individuals seeking elder care coverage without sacrificing financial security.

Coverage Benefits and Payout Structures

Long-term care insurance offers dedicated coverage specifically for extended custodial care services, with benefits structured as periodic payouts directly to providers or policyholders, often requiring medical necessity for claim approval. Hybrid insurance combines life insurance with a long-term care benefit, allowing policyholders to access a lump sum or accelerated death benefit for elder care expenses, providing greater flexibility in payout options and potential legacy value. Coverage benefits in hybrid policies tend to include death benefit guarantees alongside care payouts, whereas traditional long-term care insurance focuses solely on reimbursing qualified caregiving costs over an extended period.

Flexibility and Policy Options

Long-term care insurance offers specialized coverage exclusively for elder care services, providing flexible benefit periods and customizable daily benefit amounts tailored to individual needs. Hybrid insurance combines life insurance or annuities with long-term care benefits, allowing policyholders to access funds for care or retain death benefits if long-term care is not required. Policy options in hybrid plans often include broader financial flexibility, such as premium returns or cash value accumulation, appealing to those seeking both protection and investment potential.

Suitability: Who Should Consider Each Option?

Long-term care insurance is ideal for individuals seeking dedicated coverage for extended elder care expenses without impacting life insurance benefits. Hybrid insurance suits those looking for a combined policy that provides both life insurance and long-term care benefits, offering financial flexibility and accelerated benefits in case of chronic illness. People with a strong preference for guaranteed payout or legacy planning often find hybrid insurance more suitable, while those prioritizing comprehensive long-term care protection tend to favor traditional long-term care insurance.

Tax Implications and Incentives

Long-term care insurance premiums may qualify for tax deductions as medical expenses if they exceed a certain percentage of adjusted gross income, while benefits received are generally tax-free. Hybrid insurance policies, combining life insurance with long-term care benefits, offer tax-advantaged growth and death benefits that can be accessed tax-free when used for qualified long-term care expenses. Policyholders should evaluate eligibility for tax credits, deductions, and the impact on estate planning when choosing between standalone long-term care insurance and hybrid products.

Claims Process and Ease of Use

Long-term care insurance offers a straightforward claims process with clear eligibility criteria based on medical assessments, ensuring timely benefit payouts for elder care services. Hybrid insurance combines life insurance with long-term care benefits, often simplifying claims by integrating multiple coverages under one policy, which can reduce paperwork and processing time. Policyholders generally find hybrid insurance easier to manage due to consolidated billing and a single point of contact for claims assistance.

Deciding the Best Fit for Your Elder Care Needs

Long-term care insurance offers dedicated coverage for extended elder care services, including nursing home stays, home health care, and assisted living, with premiums based solely on this protection. Hybrid insurance combines life insurance or annuity benefits with long-term care coverage, providing a death benefit or cash value if long-term care is not needed, potentially maximizing value for policyholders. Choosing the best fit depends on factors like budget, risk tolerance, health status, and financial goals, as long-term care insurance focuses on pure protection while hybrid policies offer flexible benefits.

Related Important Terms

Chronic Illness Rider

Long-term care insurance with a chronic illness rider offers dedicated benefits specifically for extended care services due to conditions like Alzheimer's or Parkinson's, ensuring comprehensive coverage for chronic health needs. Hybrid insurance combines life insurance with long-term care benefits, allowing policyholders to access funds for chronic illness care while preserving a death benefit for beneficiaries, enhancing financial flexibility in elder care planning.

Linked-Benefit Policy

Linked-benefit policies combine long-term care coverage with life insurance or annuities, offering a hybrid solution that provides both elder care funding and financial benefits to beneficiaries. These policies can be more cost-effective than standalone long-term care insurance, ensuring coverage while preserving value even if long-term care services are not utilized.

Asset-Based Long-Term Care

Asset-based long-term care insurance combines life insurance or annuities with long-term care benefits, allowing policyholders to use their assets to cover elder care expenses while preserving wealth. Hybrid insurance offers flexible payouts and potential death benefits, making it a strategic option for managing long-term care costs without depleting other financial resources.

Partnership-Qualified Policy

Partnership-Qualified Policies in long-term care insurance offer asset protection benefits by allowing policyholders to shield a portion of their assets from Medicaid spend-down requirements, enhancing financial security for elder care. Hybrid insurance plans combine life insurance with long-term care benefits but typically do not qualify for partnership programs, limiting their potential for Medicaid asset protection.

Return of Premium Feature

Long-term care insurance typically offers a Return of Premium feature that refunds a portion of paid premiums if benefits are not fully used, providing financial reassurance for policyholders. Hybrid insurance combines life insurance with long-term care benefits, often including a Return of Premium option that enhances value by allowing unused premiums to be passed on as a death benefit, optimizing elder care planning.

Inflation Protection Option

Long-term care insurance with an inflation protection option ensures that benefit amounts increase over time to keep pace with rising care costs, preserving purchasing power for elder care. Hybrid insurance policies may include inflation protection riders that adjust the cash value or death benefit, balancing long-term care coverage with life insurance benefits to address inflation concerns.

Elimination Period

Long-term care insurance typically features a defined elimination period, during which policyholders must cover care costs out-of-pocket before benefits begin, often ranging from 30 to 90 days. Hybrid insurance for elder care often incorporates a shorter or waived elimination period, combining life insurance with long-term care benefits to provide more immediate financial support.

Cash Indemnity Benefit

Long-term care insurance offers a dedicated Cash Indemnity Benefit that provides fixed daily or monthly payments for covered care services, ensuring predictable cash flow regardless of actual expenses. Hybrid insurance combines life insurance with long-term care benefits, allowing the Cash Indemnity Benefit to accelerate death benefits for care costs, offering more flexible financial planning for elder care needs.

Accelerated Death Benefit

Long-term care insurance provides dedicated coverage for extended elder care services, while hybrid insurance combines life insurance with long-term care benefits, often including an Accelerated Death Benefit that allows policyholders to access a portion of the death benefit early to cover care expenses. This feature enhances financial flexibility by reducing out-of-pocket costs and ensuring funds are available during critical elder care needs.

Qualified Long-Term Care Contract

Long-term care insurance provides dedicated coverage for elder care services under a Qualified Long-Term Care Contract, ensuring tax-qualified benefits receive favorable tax treatment. Hybrid insurance combines life insurance or annuities with long-term care benefits, offering flexibility but may not always meet the strict IRS criteria for qualified contracts, affecting tax advantages.

Long-term care insurance vs Hybrid insurance for elder care. Infographic