Homeowners insurance provides traditional coverage by compensating policyholders for damages or losses based on assessed repair costs, subject to policy limits and deductibles. Parametric insurance offers a streamlined approach by triggering payouts when predefined events, such as specific wind speeds or earthquake magnitudes, occur, ensuring faster and more predictable claims settlements. Choosing between these options depends on the need for customizable risk protection and the desire for rapid financial support following property damage.

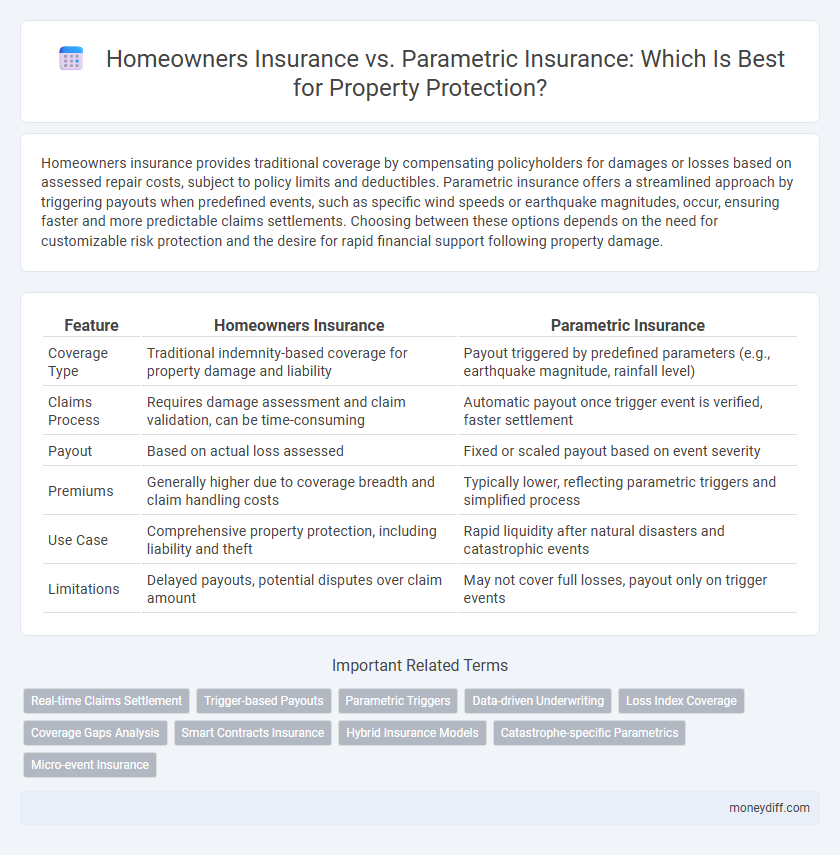

Table of Comparison

| Feature | Homeowners Insurance | Parametric Insurance |

|---|---|---|

| Coverage Type | Traditional indemnity-based coverage for property damage and liability | Payout triggered by predefined parameters (e.g., earthquake magnitude, rainfall level) |

| Claims Process | Requires damage assessment and claim validation, can be time-consuming | Automatic payout once trigger event is verified, faster settlement |

| Payout | Based on actual loss assessed | Fixed or scaled payout based on event severity |

| Premiums | Generally higher due to coverage breadth and claim handling costs | Typically lower, reflecting parametric triggers and simplified process |

| Use Case | Comprehensive property protection, including liability and theft | Rapid liquidity after natural disasters and catastrophic events |

| Limitations | Delayed payouts, potential disputes over claim amount | May not cover full losses, payout only on trigger events |

Understanding Homeowners Insurance: Traditional Coverage Explained

Homeowners insurance provides comprehensive coverage for property damage and personal liability caused by events like fire, theft, and natural disasters, with claims assessed based on actual repair or replacement costs. Policies typically include dwelling protection, personal property coverage, liability protection, and additional living expenses if the home becomes uninhabitable. Understanding policy limits, deductibles, and exclusions is essential to ensure adequate financial protection under traditional homeowners insurance.

What Is Parametric Insurance? A Modern Approach to Property Protection

Parametric insurance offers a modern approach to property protection by providing pre-defined payouts based on specific triggers like weather events or natural disasters, rather than traditional loss assessments. Unlike homeowners insurance, which requires claim adjustments and proof of damage, parametric policies streamline compensation using objective data such as wind speed or earthquake magnitude. This innovation reduces claim processing time and enhances financial resilience against rapid-impact hazards for property owners.

Key Differences Between Homeowners and Parametric Insurance

Homeowners insurance provides coverage based on actual repair or replacement costs following property damage, requiring claims adjustment and proof of loss. Parametric insurance triggers predetermined payouts when specific parameters, such as earthquake magnitude or hurricane wind speed, are met, independent of actual damage assessment. This results in faster claims processing for parametric policies but may not cover full repair costs, unlike traditional homeowners coverage.

Coverage Scope: What Each Policy Protects Against

Homeowners insurance provides broad protection against a wide range of risks including fire, theft, liability, and water damage, covering both the physical structure and personal belongings. Parametric insurance specifically protects against predefined events such as natural disasters like earthquakes or hurricanes, triggering payouts based on the occurrence of these events rather than incurred losses. This makes parametric insurance ideal for rapid financial relief after catastrophic events, while homeowners insurance offers comprehensive, ongoing property protection.

Claims Process: Homeowners vs. Parametric Insurance

Homeowners insurance claims involve detailed damage assessments, adjuster investigations, and documentation, often resulting in longer processing times due to the need for precise damage validation. Parametric insurance simplifies the claims process by triggering payouts based on predefined parameters like earthquake magnitude or wind speed, eliminating the need for loss verification. This parametric model accelerates claims settlement and provides faster financial relief compared to traditional homeowners insurance.

Payout Structures: Fixed Benefits vs. Loss Assessment

Homeowners insurance typically operates on an indemnity basis, assessing actual losses to determine payout amounts, which can lead to lengthy claim processes and variable compensation. Parametric insurance offers fixed benefits triggered by predefined parameters, such as earthquake magnitude or hurricane wind speed, enabling faster and more predictable payouts independent of actual loss assessment. This structure reduces claim disputes and provides liquidity promptly after a triggering event, enhancing financial resilience for property owners.

Cost Comparison: Premiums and Affordability

Homeowners insurance typically involves higher premiums due to comprehensive coverage and personalized risk assessment, whereas parametric insurance offers more affordable premiums by triggering payouts based on predefined parameters like weather data. Parametric insurance reduces administrative costs and claim processing time, resulting in cost efficiency, especially for properties in areas prone to specific risks. Choosing between these depends on balancing the predictability of costs against the scope of coverage needed for property protection.

Risk Scenarios: When to Choose Parametric or Homeowners Insurance

Homeowners insurance is ideal for covering traditional risks such as fire, theft, and liability, providing compensation based on actual repair or replacement costs after damage assessment. Parametric insurance suits scenarios involving rapid payouts triggered by predefined events like natural disasters (earthquakes, hurricanes) where loss assessment delays financial recovery. Selecting parametric insurance is beneficial in high-risk areas with frequent catastrophic events, while homeowners insurance remains preferable for comprehensive protection against everyday home damages.

Limitations and Exclusions of Both Insurance Types

Homeowners insurance typically excludes coverage for certain natural disasters like floods and earthquakes, requiring additional policies or endorsements for comprehensive protection. Parametric insurance offers quick payouts based on predefined triggers such as wind speed or rainfall levels but may not cover actual damages exceeding the set parameters. Both insurance types have limitations in scope, with homeowners insurance relying on detailed damage assessments and parametric insurance focusing on event metrics rather than individual loss specifics.

Future Trends: The Evolving Landscape of Property Insurance

Future trends in property insurance indicate a growing adoption of parametric insurance alongside traditional homeowners insurance, driven by advancements in data analytics and IoT technology that enable quicker claim settlements based on predefined parameters like weather events. Parametric insurance offers increased transparency and reduced administrative costs, making it a preferred choice for mitigating risks associated with climate change and natural disasters. This evolution highlights a shift towards more customized and technology-driven insurance products that enhance resilience and provide faster financial support to property owners.

Related Important Terms

Real-time Claims Settlement

Homeowners insurance typically requires detailed damage assessments and claim validations, causing delays in payouts, whereas parametric insurance uses predefined triggers such as seismic activity or wind speed to enable real-time claims settlement and faster financial recovery. This automated process reduces administrative costs and accelerates support for property owners immediately after qualifying events.

Trigger-based Payouts

Homeowners insurance provides coverage based on assessed damages after loss verification, while parametric insurance offers trigger-based payouts activated by specific predefined events such as earthquake magnitude or hurricane wind speed. Parametric policies ensure faster claim settlements and reduced administrative costs by eliminating the need for traditional damage assessments.

Parametric Triggers

Parametric insurance uses predefined triggers such as earthquake magnitude, wind speed, or rainfall amount to automatically release payments, providing faster and more transparent claims processing compared to traditional homeowners insurance that requires damage assessments. This approach reduces claim disputes and accelerates recovery efforts for property owners by linking payouts directly to measurable environmental parameters.

Data-driven Underwriting

Homeowners insurance relies on traditional claim assessments and historical data analysis for underwriting, often leading to longer claim processing times and subjective evaluations. Parametric insurance utilizes real-time data and predefined parameters such as weather metrics, enabling faster, automated payouts and more transparent, objective property protection.

Loss Index Coverage

Homeowners insurance provides traditional coverage based on itemized damage assessments, while parametric insurance offers loss index coverage triggered by pre-defined events such as earthquakes or hurricanes, enabling faster claims payouts. Parametric policies reduce claim adjustment delays and improve transparency by linking payouts directly to measurable event parameters rather than subjective damage evaluations.

Coverage Gaps Analysis

Homeowners insurance often leaves coverage gaps in cases of natural disasters or rapid damage events, while parametric insurance fills these gaps by providing predefined payouts based on specific triggers such as earthquake magnitude or hurricane wind speeds. Parametric policies enhance property protection by offering faster claims settlements and reducing uncertainties inherent in traditional loss assessments.

Smart Contracts Insurance

Homeowners insurance provides traditional indemnity coverage based on assessed damages, while parametric insurance leverages smart contracts to trigger automatic payouts when predefined event parameters, such as earthquake magnitude or flood levels, are met, enhancing speed and transparency. Smart contracts enable seamless execution without claims adjustment delays, reducing administrative costs and improving customer experience in property protection.

Hybrid Insurance Models

Hybrid insurance models combine traditional homeowners insurance with parametric coverage to enhance property protection by offering both comprehensive loss indemnity and rapid, predefined payouts triggered by specific events. These models optimize risk management by leveraging the detailed damage assessment of homeowners policies alongside the efficiency and transparency of parametric triggers, improving claims settlement speed and financial resilience for property owners.

Catastrophe-specific Parametrics

Homeowners insurance provides traditional indemnity coverage with claims settled based on assessed damages, often resulting in lengthy adjuster processes, whereas catastrophe-specific parametric insurance offers rapid, predetermined payouts triggered by objective metrics such as earthquake magnitude or hurricane wind speed, enabling faster financial recovery. Parametric insurance reduces claim settlement uncertainties and is increasingly adopted for large-scale disaster protection, complementing or sometimes replacing conventional homeowners policies in high-risk areas.

Micro-event Insurance

Homeowners insurance traditionally covers property damage based on assessed losses, while parametric insurance provides predefined payouts triggered by specific micro-events such as localized storms or earthquakes, enabling faster claims settlement and reduced administrative costs. Micro-event parametric insurance leverages precise data analytics and IoT sensors to offer tailored, cost-effective protection for homeowners against frequent, low-impact incidents often excluded from standard policies.

Homeowners insurance vs Parametric insurance for property protection. Infographic