Traditional insurance provides coverage based on assessed damages after an event, requiring claims adjustments and proof of loss, which can delay payouts. Parametric insurance offers a faster solution by triggering payments automatically when predefined parameters, such as weather thresholds or seismic activity, are met, eliminating the need for lengthy claim verification. This model enhances transparency and efficiency, making it ideal for covering specific, quantifiable risks.

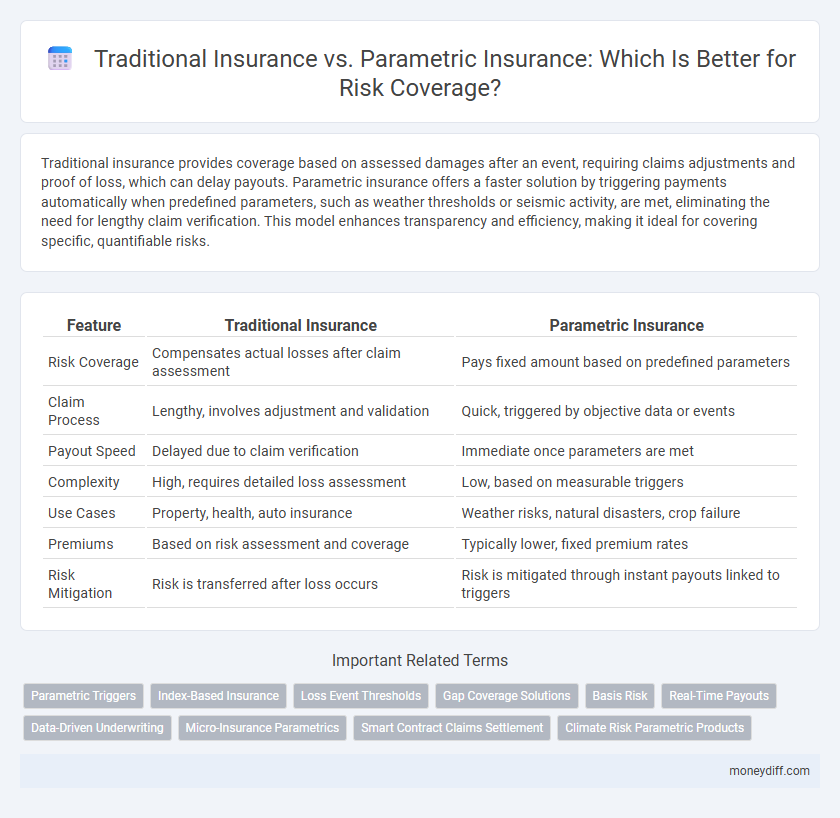

Table of Comparison

| Feature | Traditional Insurance | Parametric Insurance |

|---|---|---|

| Risk Coverage | Compensates actual losses after claim assessment | Pays fixed amount based on predefined parameters |

| Claim Process | Lengthy, involves adjustment and validation | Quick, triggered by objective data or events |

| Payout Speed | Delayed due to claim verification | Immediate once parameters are met |

| Complexity | High, requires detailed loss assessment | Low, based on measurable triggers |

| Use Cases | Property, health, auto insurance | Weather risks, natural disasters, crop failure |

| Premiums | Based on risk assessment and coverage | Typically lower, fixed premium rates |

| Risk Mitigation | Risk is transferred after loss occurs | Risk is mitigated through instant payouts linked to triggers |

Understanding Traditional Insurance: Key Features

Traditional insurance offers risk coverage by assessing individual claims based on actual losses, providing personalized compensation after thorough claim evaluations. It relies on detailed documentation and loss verification processes to determine the payout amount, ensuring coverage aligns with the policyholder's specific damages. This model emphasizes indemnity and risk pooling, often involving longer claim settlement periods compared to parametric insurance alternatives.

What is Parametric Insurance?

Parametric insurance provides predefined payouts based on specific triggering events or parameters, such as earthquake magnitude or rainfall levels, rather than actual loss assessment. This model allows for faster claims processing and reduced administrative costs compared to traditional indemnity insurance, which requires damage verification. By offering predictable coverage tied to measurable events, parametric insurance enhances risk management for natural disasters and weather-related incidents.

Differences Between Traditional and Parametric Insurance

Traditional insurance covers losses based on damage assessments and claims adjustments, requiring detailed documentation and time-consuming processes. Parametric insurance pays predetermined amounts based on measurable triggers like weather events or seismic activity, eliminating the need for loss verification. This results in faster payouts and reduced administrative costs, offering a more efficient risk coverage model for specific scenarios.

Risk Assessment Methods: Indemnity vs. Parametric Triggers

Traditional insurance relies on indemnity-based risk assessment methods, where claims are evaluated based on the actual loss or damage incurred by the policyholder, often requiring detailed documentation and on-site inspections. Parametric insurance utilizes predefined, data-driven triggers such as specific weather measurements or seismic activity thresholds, enabling faster payouts without loss verification. This parametric approach reduces claim processing time and mitigates moral hazard by objectively linking payouts to measurable events rather than subjective damage assessments.

Speed of Claims Settlement: Traditional vs. Parametric

Traditional insurance claims settlement involves thorough assessments and documentation, often leading to lengthy processing times that can delay payouts. Parametric insurance accelerates claim payments by using predefined triggers and data-driven indexes, enabling near-instant disbursement once conditions are met. This speed enhancement significantly improves liquidity and financial recovery for policyholders facing urgent risk exposures.

Cost Efficiency in Insurance Models

Traditional insurance typically involves higher administrative costs and slower claim settlements due to manual assessment processes, impacting overall cost efficiency. Parametric insurance leverages predefined triggers and automated payouts, significantly reducing operational expenses and accelerating compensation. This model enhances cost efficiency by minimizing claim disputes and streamlining risk transfer for both insurers and policyholders.

Coverage Scenarios: When to Choose Traditional Insurance

Traditional insurance is ideal for complex coverage scenarios involving multiple risk factors such as property damage, liability claims, or health-related expenses where detailed loss assessment is necessary. It provides tailored indemnity payments based on actual loss evaluations, ensuring comprehensive financial protection for unpredictable or heterogeneous risks. Choose traditional insurance when precise damage verification and customizable coverage limits are essential for mitigating diverse or high-value exposures.

Ideal Use Cases for Parametric Insurance

Parametric insurance is ideal for covering risks linked to specific, measurable events such as natural disasters, where payouts are triggered by predefined parameters like earthquake magnitude or rainfall levels. This type of insurance suits businesses and regions vulnerable to climate-related events, enabling rapid claims settlement without lengthy loss assessments. Parametric models efficiently protect agricultural sectors, event organizers, and supply chain operators exposed to weather volatility or catastrophic events.

Limitations and Challenges of Each Approach

Traditional insurance often faces challenges such as lengthy claims processing, subjective damage assessments, and complex policy conditions that may delay payouts. Parametric insurance relies on preset triggers like weather data or seismic activity, but it can result in basis risk where payouts do not perfectly match the actual loss experienced by the insured. Both approaches require accurate data and robust infrastructure, yet parametric insurance can struggle with limited coverage scenarios and acceptance among consumers unfamiliar with its model.

Choosing the Right Insurance Solution for Optimal Risk Coverage

Traditional insurance provides indemnity based on actual loss assessment, offering broad coverage for unpredictable risks but often involving lengthy claims processes and potential disputes over damage valuation. Parametric insurance triggers automatic payouts when predefined parameters, such as earthquake magnitude or hurricane wind speed, are met, ensuring rapid compensation and reducing claim settlement complexity. Selecting the right insurance solution depends on the risk profile, desired payout speed, and transparency, with parametric insurance being ideal for quantifiable, high-frequency events and traditional insurance better suited for complex, variable claims.

Related Important Terms

Parametric Triggers

Parametric insurance uses predefined triggers based on measurable parameters such as rainfall levels, wind speed, or earthquake magnitude to initiate payouts, enabling faster and more transparent claim settlements than traditional indemnity insurance. This approach reduces the need for loss adjustment processes and mitigates disputes, offering efficient risk coverage especially in sectors vulnerable to natural disasters.

Index-Based Insurance

Index-based parametric insurance offers faster, transparent payouts triggered by predefined metrics such as weather indices or seismic activity levels, reducing claim processing time compared to traditional indemnity insurance that requires individual loss assessment. This model significantly lowers administrative costs and moral hazard by providing objective, data-driven risk coverage tailored for natural disasters and crop failures.

Loss Event Thresholds

Traditional insurance typically requires proof of actual loss before payout, often involving complex claims assessments and delays, whereas parametric insurance triggers payments based on predefined loss event thresholds such as earthquake magnitude or rainfall levels, enabling faster and more transparent risk coverage. This threshold-based approach reduces administrative costs and uncertainty, providing policyholders with immediate financial support when specified parameters are met, regardless of the actual loss incurred.

Gap Coverage Solutions

Traditional insurance offers indemnity-based risk coverage by compensating losses after an event, while parametric insurance provides predefined payouts triggered by specific parameters, enabling faster claims resolution. Gap coverage solutions leverage parametric insurance to fill coverage voids in standard policies, ensuring comprehensive protection against uncovered risks.

Basis Risk

Traditional insurance often involves indemnity-based claims with potential delays and disputes over coverage, leading to increased basis risk where payouts do not perfectly match actual losses. Parametric insurance reduces basis risk by triggering payments based on predefined parameters or indices, ensuring faster, more transparent compensation aligned closely with the insured event.

Real-Time Payouts

Parametric insurance offers real-time payouts by using predefined triggers and automated data feeds, eliminating lengthy claim assessments typical of traditional insurance. This instant compensation enhances risk coverage efficiency, particularly in scenarios like natural disasters where rapid financial support is critical.

Data-Driven Underwriting

Data-driven underwriting in traditional insurance relies on comprehensive historical claims data and individual risk assessments, enabling precise premium calculations based on past loss patterns. In contrast, parametric insurance leverages real-time, objective data such as weather sensors or seismic readings to trigger predefined payouts, streamlining claims processing and reducing underwriting complexity.

Micro-Insurance Parametrics

Micro-insurance parametrics use predefined triggers based on measurable data such as rainfall levels or wind speed to provide rapid payouts, reducing claim processing time compared to traditional insurance. This approach enhances risk coverage for low-income populations by offering affordable, transparent, and efficient protection against specific environmental and climate-related risks.

Smart Contract Claims Settlement

Traditional insurance relies on assessed damages and lengthy claims processes, whereas parametric insurance uses predefined trigger events verified through smart contract claims settlement, ensuring faster and transparent payouts. Smart contracts automate claim validation by linking real-time data inputs to policy conditions, minimizing disputes and reducing administrative costs in risk coverage.

Climate Risk Parametric Products

Climate risk parametric insurance offers rapid payouts based on predefined climate triggers such as temperature, rainfall, or wind speed thresholds, eliminating the need for lengthy claims assessments typical in traditional indemnity insurance. This innovative approach enhances financial resilience for vulnerable regions by providing immediate liquidity following climate events like floods or droughts, optimizing risk coverage and mitigating economic losses.

Insurance vs Parametric Insurance for risk coverage. Infographic