Disability insurance provides income replacement if you become unable to work due to injury or illness, covering a broad range of conditions that affect your ability to earn. Critical illness cover offers a lump sum payment upon diagnosis of specified severe illnesses such as cancer, heart attack, or stroke, helping to manage medical costs and other expenses. Choosing between the two depends on your need for ongoing income support versus a one-time financial boost during critical health events.

Table of Comparison

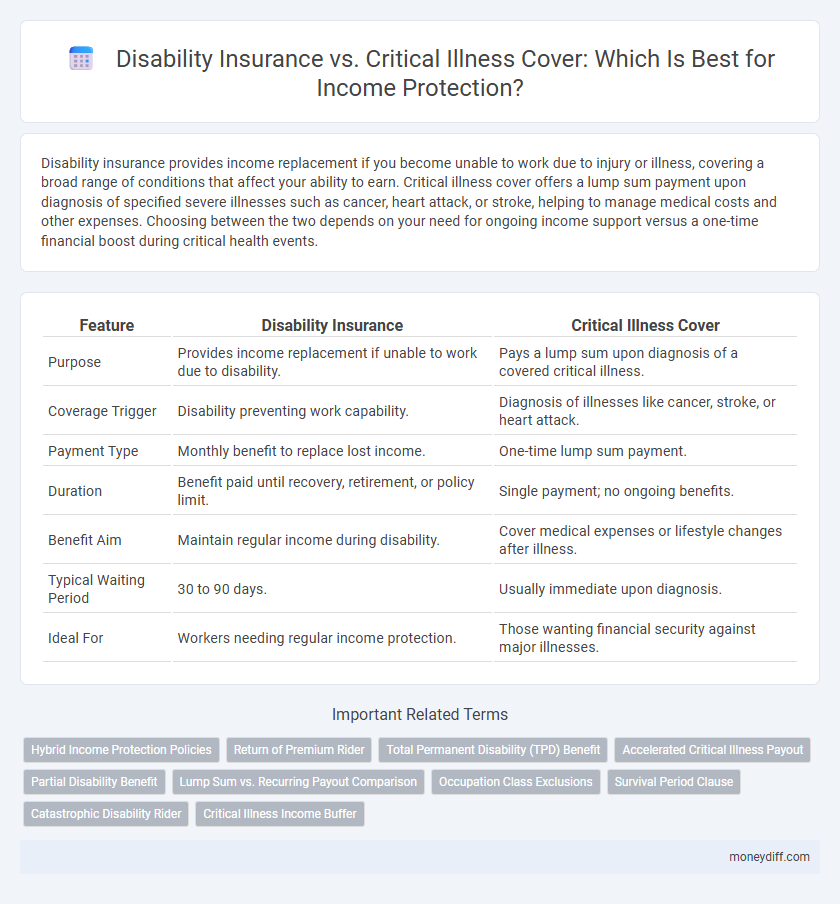

| Feature | Disability Insurance | Critical Illness Cover |

|---|---|---|

| Purpose | Provides income replacement if unable to work due to disability. | Pays a lump sum upon diagnosis of a covered critical illness. |

| Coverage Trigger | Disability preventing work capability. | Diagnosis of illnesses like cancer, stroke, or heart attack. |

| Payment Type | Monthly benefit to replace lost income. | One-time lump sum payment. |

| Duration | Benefit paid until recovery, retirement, or policy limit. | Single payment; no ongoing benefits. |

| Benefit Aim | Maintain regular income during disability. | Cover medical expenses or lifestyle changes after illness. |

| Typical Waiting Period | 30 to 90 days. | Usually immediate upon diagnosis. |

| Ideal For | Workers needing regular income protection. | Those wanting financial security against major illnesses. |

Understanding Disability Insurance and Critical Illness Cover

Disability Insurance provides income replacement if you are unable to work due to illness or injury, ensuring financial stability during extended periods of incapacity. Critical Illness Cover pays a lump sum upon diagnosis of specific severe health conditions, offering funds to cover medical expenses or lifestyle adjustments. Understanding the distinctions between these policies helps in selecting appropriate income protection tailored to your health risks and financial needs.

Key Differences Between Disability Insurance and Critical Illness Cover

Disability insurance provides financial support by replacing a portion of income if an individual becomes unable to work due to illness or injury, whereas critical illness cover delivers a lump sum payment upon diagnosis of specific serious health conditions like cancer or stroke. Disability insurance typically covers a broader range of health issues impacting work capacity, while critical illness policies focus on predefined illnesses listed in the contract. Income protection through disability insurance tends to be ongoing based on disability duration, contrasting with critical illness cover's one-time benefit designed for immediate medical and personal expenses.

How Disability Insurance Protects Your Income

Disability insurance provides essential income protection by replacing a portion of your earnings if illness or injury prevents you from working, ensuring financial stability during recovery. It covers a broad range of disabilities, including temporary and permanent impairments, offering long-term support unlike critical illness cover, which pays a lump sum only upon diagnosis of specific diseases. This ongoing income replacement allows policyholders to maintain daily living expenses and financial obligations without depleting savings or assets.

The Role of Critical Illness Cover in Financial Planning

Critical Illness Cover plays a crucial role in financial planning by providing a lump sum payment upon diagnosis of specified serious illnesses, helping to cover medical expenses and replace lost income during recovery. Unlike Disability Insurance, which offers ongoing income replacement for inability to work, Critical Illness Cover addresses high-cost medical events that can disrupt financial stability. Integrating Critical Illness Cover ensures broader protection against life-altering health conditions, safeguarding savings and maintaining financial resilience.

Coverage Scenarios: When Each Policy Pays Out

Disability insurance pays out when an insured individual is unable to work due to injury or illness, providing income replacement during periods of partial or total disability. Critical illness cover offers a lump sum payout following the diagnosis of specified severe conditions such as cancer, heart attack, or stroke, regardless of work capacity. Income protection is better supported by disability insurance for ongoing wage replacement, while critical illness cover is focused on financial support for treatment and recovery costs related to major illnesses.

Costs and Premiums: Disability vs Critical Illness Insurance

Disability insurance typically features higher premiums compared to critical illness cover due to broader income protection that includes partial disabilities and long-term impairment. Critical illness insurance premiums tend to be lower because payouts are triggered only upon diagnosis of specific serious conditions outlined in the policy. Cost differences also reflect varying risk assessments and benefit structures, impacting affordability and coverage scope for policyholders seeking income protection.

Claim Process: Disability Insurance vs Critical Illness Cover

Disability insurance claims typically require medical documentation proving the inability to work due to injury or illness, often involving detailed assessments by healthcare professionals and insurers to confirm long-term disability. Critical illness cover claims mandate a confirmed diagnosis of one of the specified conditions listed in the policy, such as cancer or stroke, with payout usually occurring upon medical verification, often resulting in quicker benefit disbursement compared to disability claims. Both processes demand stringent proof but differ in trigger events, with disability claims tied to work impairment and critical illness claims linked directly to diagnosed diseases.

Assessing Your Personal Income Protection Needs

Disability insurance provides income replacement if you become unable to work due to injury or illness, while critical illness cover offers a lump sum payment upon diagnosis of specified serious conditions. Assessing your personal income protection needs requires evaluating your financial obligations, existing savings, and potential recovery timeline to determine which policy better safeguards your livelihood. Understanding the nuances of both covers ensures an optimal strategy for maintaining financial stability during health crises.

Combining Disability and Critical Illness Policies for Comprehensive Protection

Combining disability insurance and critical illness cover enhances income protection by addressing a wider range of health-related risks, ensuring financial stability during extended periods of illness or injury. Disability insurance provides ongoing income replacement if you are unable to work due to a disability, while critical illness cover offers a lump sum payment upon diagnosis of specified serious illnesses. Integrating both policies delivers comprehensive protection by covering both long-term inability to work and immediate financial burdens caused by critical health conditions.

Tips for Choosing the Right Income Protection Insurance

Evaluate your specific financial needs and job risks to determine whether disability insurance or critical illness cover provides better income protection tailored to your situation. Prioritize policies with comprehensive definitions of disability or critical illness, waiting periods, and benefit durations that align with your budget and long-term security goals. Consult with an insurance advisor to compare coverage options, exclusions, and premium costs to ensure optimal protection and peace of mind.

Related Important Terms

Hybrid Income Protection Policies

Hybrid income protection policies combine the benefits of disability insurance and critical illness cover, providing comprehensive financial support by covering both inability to work due to disability and diagnosed critical illnesses. These policies ensure continuous income replacement while addressing specific health conditions, optimizing protection and reducing gaps in traditional coverage.

Return of Premium Rider

Disability Insurance with a Return of Premium Rider refunds policyholders their premiums if no claims are made, enhancing long-term value compared to Critical Illness Cover, which typically does not offer premium returns. This rider makes Disability Insurance a cost-effective option for income protection by combining financial security during disability with potential premium recovery.

Total Permanent Disability (TPD) Benefit

Total Permanent Disability (TPD) Benefit within Disability Insurance provides comprehensive income protection by offering a lump sum payment when an individual is permanently unable to work due to disability, ensuring financial stability during long-term incapacity. Critical Illness Cover, while valuable for covering specific medical diagnoses, typically offers lump sum payouts only upon diagnosis of listed illnesses and may not cover the broader financial impact of permanent disability affecting work capacity.

Accelerated Critical Illness Payout

Disability insurance provides income replacement when you cannot work due to injury or illness, while Critical Illness Cover offers a lump-sum payment upon diagnosis of specified conditions, with Accelerated Critical Illness Payout allowing early access to a portion of the sum assured to cover immediate expenses. This feature enhances financial flexibility by reducing long-term stress during critical health events, complementing traditional disability income protection strategies.

Partial Disability Benefit

Partial Disability Benefit under Disability Insurance provides income replacement when policyholders return to work in a limited capacity due to injury or illness, bridging the gap between full disability and recovery. Critical Illness Cover pays a lump sum upon diagnosis of specified conditions but does not offer ongoing income support for partial work capabilities.

Lump Sum vs. Recurring Payout Comparison

Disability insurance typically provides recurring payouts based on a percentage of your income while you are unable to work, offering ongoing financial support. Critical illness cover delivers a lump sum payment upon diagnosis of a covered condition, allowing policyholders to manage immediate expenses without ongoing installments.

Occupation Class Exclusions

Disability insurance typically has strict occupation class exclusions that can limit coverage for high-risk professions, whereas critical illness cover often includes broader protection regardless of occupation, focusing instead on specific health conditions. Understanding these exclusions is crucial for accurate income protection, especially for individuals in hazardous or specialized jobs who may face policy denials under disability insurance but maintain eligibility under critical illness cover.

Survival Period Clause

Disability insurance typically includes a survival period clause that requires the insured to survive a specified number of days after the disability onset before benefits are payable, whereas critical illness cover often mandates a survival period to confirm the diagnosis and severity of the illness. Understanding the differences in survival period clauses is crucial for ensuring timely income protection and avoiding benefit delays during critical health events.

Catastrophic Disability Rider

Disability insurance with a Catastrophic Disability Rider provides enhanced income protection by covering severe disabilities that result in complete inability to perform daily activities, unlike standard critical illness cover which typically pays out a lump sum upon diagnosis of specific illnesses. This rider ensures ongoing financial support during long-term or permanent disabilities, addressing gaps left by critical illness policies that may not cover all causes of income loss.

Critical Illness Income Buffer

Critical Illness Cover provides a crucial income buffer by delivering a lump sum payment upon diagnosis of specified severe illnesses, helping policyholders manage financial obligations during recovery. Unlike Disability Insurance, which offers ongoing income replacement for work-related disabilities, Critical Illness Cover targets early-stage financial stability in the face of critical health events.

Disability Insurance vs Critical Illness Cover for income protection. Infographic