Accident insurance provides standalone coverage specifically for personal accidents, offering tailored protection and benefits in case of injury or disability. Embedded insurance integrates accident coverage within other products or services, such as travel or automotive policies, providing seamless protection without requiring a separate policy. Choosing between the two depends on the need for specialized coverage versus convenience and cost-effectiveness within bundled offers.

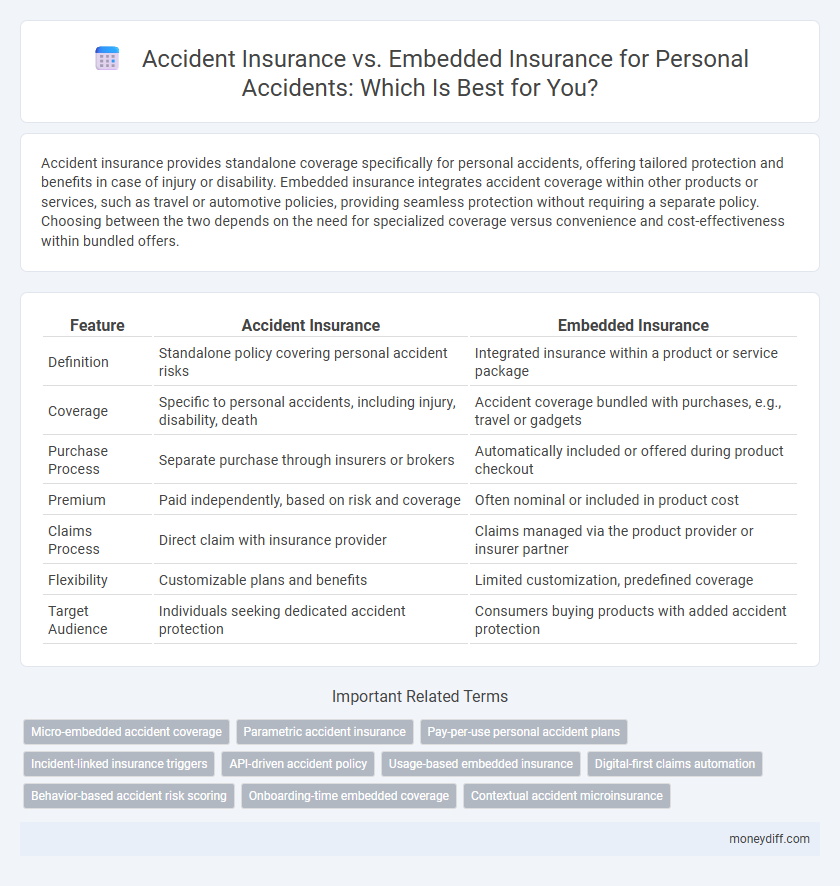

Table of Comparison

| Feature | Accident Insurance | Embedded Insurance |

|---|---|---|

| Definition | Standalone policy covering personal accident risks | Integrated insurance within a product or service package |

| Coverage | Specific to personal accidents, including injury, disability, death | Accident coverage bundled with purchases, e.g., travel or gadgets |

| Purchase Process | Separate purchase through insurers or brokers | Automatically included or offered during product checkout |

| Premium | Paid independently, based on risk and coverage | Often nominal or included in product cost |

| Claims Process | Direct claim with insurance provider | Claims managed via the product provider or insurer partner |

| Flexibility | Customizable plans and benefits | Limited customization, predefined coverage |

| Target Audience | Individuals seeking dedicated accident protection | Consumers buying products with added accident protection |

Understanding Accident Insurance: Key Features

Accident insurance provides standalone coverage specifically for injuries resulting from accidents, offering benefits such as medical expense reimbursement, disability support, and accidental death payouts. Embedded insurance integrates accident coverage within other products or services, delivering seamless protection without separate policy management. Understanding the distinct claims processes, premium structures, and coverage limits is essential for choosing between dedicated accident insurance and embedded options tailored to personal accident risks.

What Is Embedded Insurance for Personal Accidents?

Embedded insurance for personal accidents integrates coverage directly into the purchase of products or services, offering seamless protection without requiring separate insurance transactions. This approach enhances customer convenience by bundling accident insurance with items like electronics, travel bookings, or ride-sharing services, ensuring immediate coverage at the point of sale. Compared to traditional accident insurance, embedded insurance simplifies claims processing and increases policy adoption by embedding protection within everyday purchases.

Coverage Comparison: Accident vs Embedded Insurance

Accident insurance provides dedicated coverage for personal injuries resulting from specific accidents, often with predefined benefits and exclusions tailored to various risk levels. Embedded insurance integrates accident coverage within broader policies, such as travel or auto insurance, offering convenience but potentially limited payouts and conditions tied to the primary policy. Understanding the scope, limits, and claim processes of each helps optimize protection based on individual risk profiles and lifestyle needs.

Policy Flexibility: Standalone vs Integrated Options

Accident insurance offers standalone policies with customizable coverage limits and tailored benefits specific to personal accidents, providing maximum policy flexibility for individual needs. Embedded insurance integrates personal accident coverage within broader insurance products like travel or health plans, resulting in less flexible but more convenient options. Choosing between standalone and integrated policies depends on the desired balance of coverage customization versus seamless inclusion in overall insurance packages.

Costs and Premiums: Which Offers Better Value?

Accident insurance typically involves separate policies with fixed premiums based on individual risk profiles, often resulting in higher costs compared to embedded insurance. Embedded insurance integrates personal accident coverage within existing services or products, offering lower premiums by leveraging bundled risk and operational efficiencies. Consumers seeking cost-effective solutions generally find embedded insurance delivers better value through reduced premiums and streamlined coverage.

Claim Processes: Is Embedded Insurance Simpler?

Embedded insurance streamlines the claim process by integrating coverage directly into products or services, reducing paperwork and approval times compared to traditional accident insurance. Claims are often triggered automatically or require minimal customer intervention, accelerating payouts and enhancing user experience. This simplified approach contrasts with standalone accident insurance, which typically demands detailed documentation and longer verification periods.

Customization: Tailoring Protection to Individual Needs

Accident insurance offers customizable coverage options that allow individuals to select specific protection tailored to their unique risk factors and lifestyle, enhancing personal security. Embedded insurance, integrated into products or services, provides automatic yet limited protection, often lacking the flexibility to adjust coverage levels or benefits according to individual circumstances. Personalized customization in accident insurance ensures optimal financial support and peace of mind by addressing distinct personal accident risks and coverage preferences.

Exclusions and Limitations: What’s Not Covered?

Accident insurance typically excludes coverage for injuries sustained during high-risk activities such as extreme sports, self-inflicted harm, or accidents under the influence of alcohol or drugs. Embedded insurance for personal accidents often comes with limitations tied to the primary product, excluding incidents unrelated to the main service or product purchased. Both forms may exclude pre-existing conditions, war-related injuries, and intentional acts, heavily influencing the scope of protection available to policyholders.

Accessibility: Purchasing Accident vs Embedded Insurance

Accident insurance typically requires a separate purchase process, involving detailed underwriting and possibly medical examinations, which can limit accessibility for some consumers. Embedded insurance for personal accidents is integrated directly into related products or services, such as travel bookings or credit cards, enabling instant coverage without separate application procedures. This seamless accessibility of embedded insurance enhances consumer convenience and broadens protection reach compared to traditional standalone accident insurance policies.

Making the Right Choice for Personal Accident Protection

Accident insurance offers standalone coverage specifically designed to provide financial support during personal accidents, often featuring comprehensive benefits and customizable plans. Embedded insurance integrates personal accident coverage within another product or service, such as travel or vehicle insurance, providing convenience and cost-effectiveness but sometimes with limited coverage scope. Evaluating individual risk exposure, coverage limits, and premium costs is crucial in making the right choice for robust personal accident protection.

Related Important Terms

Micro-embedded accident coverage

Micro-embedded accident coverage integrates personal accident protection directly into everyday services and products, offering seamless, low-cost accident insurance tailored for digital consumers. This approach enhances accessibility and convenience compared to traditional standalone accident insurance policies by embedding risk protection at points of purchase or usage.

Parametric accident insurance

Parametric accident insurance offers predefined payouts triggered by specific accident parameters, providing faster claims settlement compared to traditional embedded insurance integrated within broader policies. This approach enhances transparency and efficiency by using data-driven triggers rather than subjective loss assessments, making it ideal for personal accident coverage with clear, immediate compensation.

Pay-per-use personal accident plans

Pay-per-use personal accident plans offer flexible, cost-effective coverage by charging premiums based on actual usage or exposure time, contrasting with traditional accident insurance that involves fixed, continuous payments regardless of risk occurrence. Embedded insurance integrates personal accident coverage directly into products or services, streamlining claims and enhancing customer experience but often lacks the dynamic adaptability of pay-per-use models tailored to individual activity levels.

Incident-linked insurance triggers

Accident insurance offers standalone coverage activated by specific personal accident incidents, ensuring direct financial protection when a qualifying event occurs. Embedded insurance integrates accident coverage within other products or services, triggering claims automatically based on incident data or usage patterns linked to the primary offering.

API-driven accident policy

API-driven accident insurance policies offer seamless integration with digital platforms, enabling real-time underwriting and claims processing for personalized accident coverage. Embedded insurance integrates accident protection directly into products or services, enhancing customer experience by providing hassle-free, context-specific coverage without separate policy management.

Usage-based embedded insurance

Usage-based embedded insurance for personal accidents integrates accident coverage directly into products or services, leveraging real-time data from devices or apps to tailor premiums and benefits according to individual risk profiles. This model contrasts with traditional accident insurance by offering seamless protection within everyday activities, enhancing convenience and personalized risk management.

Digital-first claims automation

Accident insurance offers standalone coverage specifically for personal injuries, while embedded insurance integrates personal accident protection seamlessly within digital platforms, enhancing user experience. Digital-first claims automation accelerates claim processing, reduces errors, and provides instant policyholder updates, significantly improving efficiency and customer satisfaction in both models.

Behavior-based accident risk scoring

Behavior-based accident risk scoring enhances the precision of personal accident insurance underwriting by analyzing individual driving habits, thereby reducing claim frequency and cost. Embedded insurance integrates this scoring within other services or products, allowing seamless risk assessment and personalized insurance pricing without disrupting the customer experience.

Onboarding-time embedded coverage

Onboarding-time embedded coverage in personal accident insurance seamlessly integrates protection into existing services, enhancing customer experience by providing immediate, hassle-free coverage without separate policy purchases. This contrasts with traditional accident insurance requiring standalone policies, often leading to longer acquisition processes and potential coverage gaps during onboarding.

Contextual accident microinsurance

Accident microinsurance offers affordable, context-specific coverage tailored to daily personal accident risks, providing rapid claims processing and flexible benefits unlike traditional embedded insurance that is bundled within broader policies and may lack personalization. This targeted approach enhances financial protection for low-income individuals by addressing unique accident exposures in various environments.

Accident insurance vs Embedded insurance for personal accidents. Infographic