Life insurance provides financial security to beneficiaries by paying a death benefit upon the policyholder's death, covering personal income loss and final expenses. Parametric insurance offers rapid compensation based on predefined event triggers, such as natural disasters or weather conditions, without requiring traditional loss assessment. Choosing between life insurance and parametric insurance depends on whether protection is needed for personal life risk or specific event-based financial exposure.

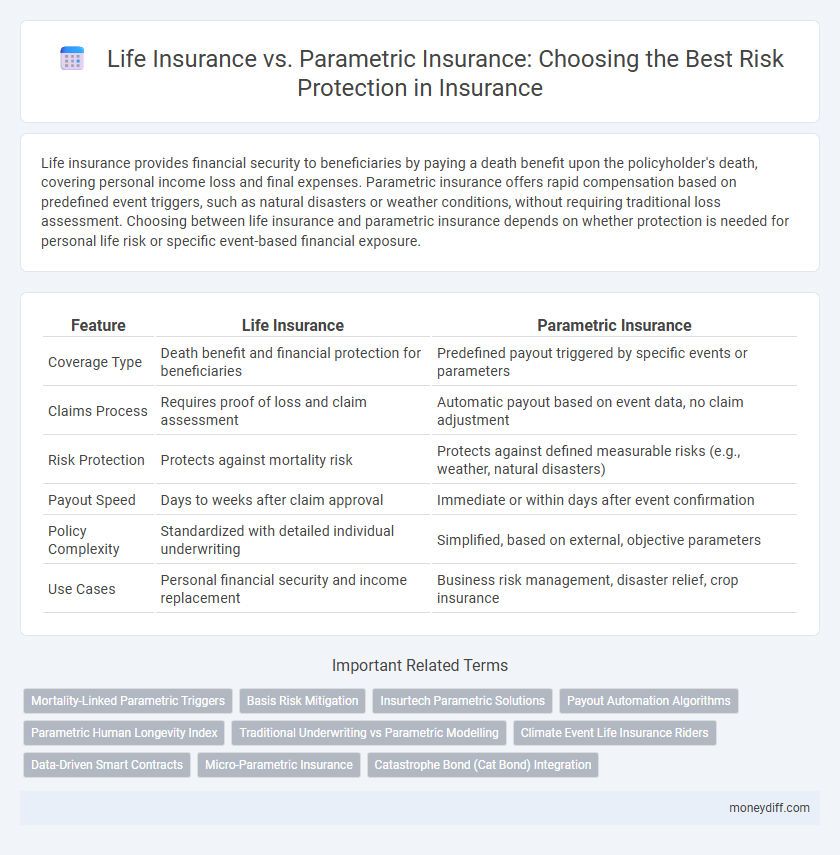

Table of Comparison

| Feature | Life Insurance | Parametric Insurance |

|---|---|---|

| Coverage Type | Death benefit and financial protection for beneficiaries | Predefined payout triggered by specific events or parameters |

| Claims Process | Requires proof of loss and claim assessment | Automatic payout based on event data, no claim adjustment |

| Risk Protection | Protects against mortality risk | Protects against defined measurable risks (e.g., weather, natural disasters) |

| Payout Speed | Days to weeks after claim approval | Immediate or within days after event confirmation |

| Policy Complexity | Standardized with detailed individual underwriting | Simplified, based on external, objective parameters |

| Use Cases | Personal financial security and income replacement | Business risk management, disaster relief, crop insurance |

Understanding Life Insurance: Traditional Risk Protection

Life insurance provides financial security by paying beneficiaries a predetermined sum upon the policyholder's death, covering risks related to income loss and funeral expenses. Traditional life insurance policies are underwritten based on health, age, and lifestyle, offering long-term protection with fixed premiums and guaranteed payouts. This ensures stable financial support for dependents during unforeseen life events, differentiating it from parametric insurance which relies on predefined triggers instead of actual loss assessments.

What Is Parametric Insurance? A Modern Approach

Parametric insurance offers a modern approach to risk protection by providing pre-agreed payouts based on measurable triggering events such as natural disasters, rather than traditional loss assessments. Unlike life insurance, which indemnifies policyholders after evaluating the actual loss or death, parametric insurance delivers rapid compensation once specific parameters, like earthquake magnitude or rainfall levels, are met. This model reduces claim processing time and eliminates disputes over damage extent, making it ideal for fast, transparent financial relief.

Key Features: Life Insurance vs Parametric Insurance

Life insurance provides a fixed payout based on a policyholder's death or critical illness, offering financial security to beneficiaries through assessed individual risk profiles and medical underwriting. Parametric insurance delivers predetermined payments triggered by specific, measurable events like natural disasters, utilizing objective data such as earthquake magnitude or hurricane wind speed for rapid claims settlement. Key features include life insurance's personalized risk assessment and long-term coverage versus parametric insurance's event-triggered payouts and efficiency in managing risks with clear, predefined parameters.

How Each Insurance Type Handles Claims

Life insurance handles claims through a comprehensive evaluation process requiring beneficiaries to submit detailed documentation, such as death certificates and policy information, before receiving a lump-sum payout that supports long-term financial security. Parametric insurance simplifies claims by using predefined parameters, such as weather data or seismic activity measurements, to trigger automatic payments without the need for loss verification, enabling faster compensation. This streamlined approach benefits those seeking immediate liquidity after specific events, while traditional life insurance offers robust protection tailored to individual circumstances.

Cost Comparison: Premiums and Payouts

Life insurance premiums typically vary based on age, health, and coverage amount, with payouts contingent on the policyholder's death or terminal illness, often resulting in higher costs due to individualized underwriting. Parametric insurance offers lower, fixed premiums by triggering payouts based on pre-defined parameters like natural disaster magnitude or weather thresholds, enabling faster claim settlements and reduced administrative expenses. The cost efficiency of parametric insurance makes it a viable alternative for specific risks, while life insurance remains essential for personalized, long-term financial protection.

Coverage Scope: Which Risks Are Protected?

Life insurance primarily covers mortality risk by providing a death benefit to beneficiaries upon the policyholder's death, thereby securing financial stability for dependents. Parametric insurance protects against specific, predefined events such as natural disasters or weather-related incidents by triggering payouts based on measured parameters rather than actual loss assessments. The coverage scope of parametric insurance is more event-specific and often complements traditional life insurance by addressing non-mortality risks linked to environmental or operational disruptions.

Customization and Flexibility in Insurance Plans

Life insurance policies offer extensive customization through variable coverage options, riders, and premium payment plans tailored to individual needs, ensuring long-term financial security for beneficiaries. Parametric insurance provides enhanced flexibility by triggering pre-defined payouts based on specific parameters or indices, enabling rapid claim settlements without the need for loss assessment. This parametric approach allows for more precise risk management in dynamic environments, complementing traditional life insurance policies with adaptable protection.

Claims Process: Speed and Transparency

Life insurance claims typically involve detailed documentation and underwriting, which can extend processing times and introduce complexity. Parametric insurance offers faster payouts by triggering claims based on predefined parameters, such as weather events or earthquake magnitude, without the need for extensive loss adjustment. This model enhances transparency and reduces disputes, providing swift financial relief to policyholders after qualifying events.

Suitability: Who Should Choose Which Insurance?

Life insurance is suitable for individuals seeking financial security for their dependents in the event of death, providing a predetermined payout to beneficiaries. Parametric insurance best serves businesses or individuals requiring rapid compensation for specific, measurable risks like natural disasters, as it triggers payment based on predefined parameters rather than assessed damages. Choosing between life and parametric insurance depends on whether the primary need is long-term personal income protection or quick risk mitigation for quantifiable events.

Making the Right Choice for Your Financial Security

Life insurance provides financial security by offering a predetermined payout upon the policyholder's death, ensuring long-term family protection. Parametric insurance covers specific, predefined events like natural disasters through pre-agreed triggers, enabling faster claim settlements without detailed loss assessments. Choosing between life insurance and parametric insurance depends on individual risk exposure, financial goals, and the need for either comprehensive personal coverage or rapid disaster-related compensation.

Related Important Terms

Mortality-Linked Parametric Triggers

Life insurance provides financial security through traditional indemnity payments upon death, while parametric insurance with mortality-linked parametric triggers offers rapid, predetermined payouts based on specific mortality data thresholds, enhancing timely risk protection. Mortality-linked parametric triggers reduce claim processing delays by activating payments once defined mortality indices, such as excess death rates, are met, optimizing coverage efficiency and transparency.

Basis Risk Mitigation

Life insurance provides a fixed payout based on the insured event, which can result in basis risk if actual losses do not align with policy terms. Parametric insurance mitigates basis risk by triggering payouts based on predefined parameters or indices, ensuring faster and more accurate compensation aligned with the specific risk exposure.

Insurtech Parametric Solutions

Parametric insurance, powered by advanced insurtech solutions, offers rapid payouts based on predefined triggers such as weather data or natural disasters, contrasting with traditional life insurance that requires claim validation and lengthy processing. These innovative parametric products enhance risk protection by providing transparency, speed, and cost-efficiency, ideal for addressing gaps where conventional life insurance may fall short in covering event-driven losses.

Payout Automation Algorithms

Life insurance traditionally relies on claim verification processes that can delay payouts, whereas parametric insurance uses payout automation algorithms triggered by predefined event parameters, enabling rapid and transparent compensation. These algorithms leverage real-time data sources such as weather sensors or seismic activity monitors to eliminate subjective assessments, enhancing efficiency and reducing administrative costs in risk protection.

Parametric Human Longevity Index

Parametric insurance leverages the Human Longevity Index to provide swift, predetermined payouts based on quantifiable longevity risk triggers, bypassing traditional claims assessments found in life insurance. This approach enhances risk protection by offering transparent, data-driven solutions that address uncertainties in lifespan more efficiently than conventional life policies.

Traditional Underwriting vs Parametric Modelling

Traditional underwriting in life insurance relies on detailed individual assessments such as medical history, lifestyle, and actuarial data to determine premiums and coverage, ensuring personalized risk evaluation. Parametric insurance uses predefined trigger events, like natural disaster indices or biometric data thresholds, enabling faster, automated payouts based on objective parameters rather than individual loss verification.

Climate Event Life Insurance Riders

Life Insurance with Climate Event Riders enhances traditional death benefits by providing payouts linked to specific climate disasters, offering policyholders targeted financial protection against environmental risks. Parametric Insurance triggers automatic payments based on predefined climate data thresholds, delivering faster, transparent coverage but without life event contingencies inherent in traditional life policies.

Data-Driven Smart Contracts

Life insurance relies on traditional underwriting and claims assessments, while parametric insurance uses data-driven smart contracts to automatically trigger payouts based on predefined parameters such as weather data or seismic activity. This automation enhances efficiency and transparency, reducing claim processing time and minimizing disputes by leveraging real-time data from IoT sensors and satellite feeds.

Micro-Parametric Insurance

Micro-parametric insurance provides targeted, algorithm-driven payouts triggered by specific measurable events, offering faster claims settlement and reduced administrative costs compared to traditional life insurance. This innovative approach enhances risk protection for underserved populations by enabling affordable, transparent coverage tied directly to quantifiable parameters such as weather conditions or biometric data.

Catastrophe Bond (Cat Bond) Integration

Life insurance provides financial protection based on individual mortality risk, whereas parametric insurance offers predefined payouts triggered by specific events such as natural disasters, enhancing immediacy in claims processing. Catastrophe bonds (Cat Bonds) integrated with parametric insurance facilitate risk transfer to capital markets, enabling insurers to manage catastrophe risk efficiently and ensure rapid liquidity post-disaster.

Life Insurance vs Parametric Insurance for risk protection. Infographic