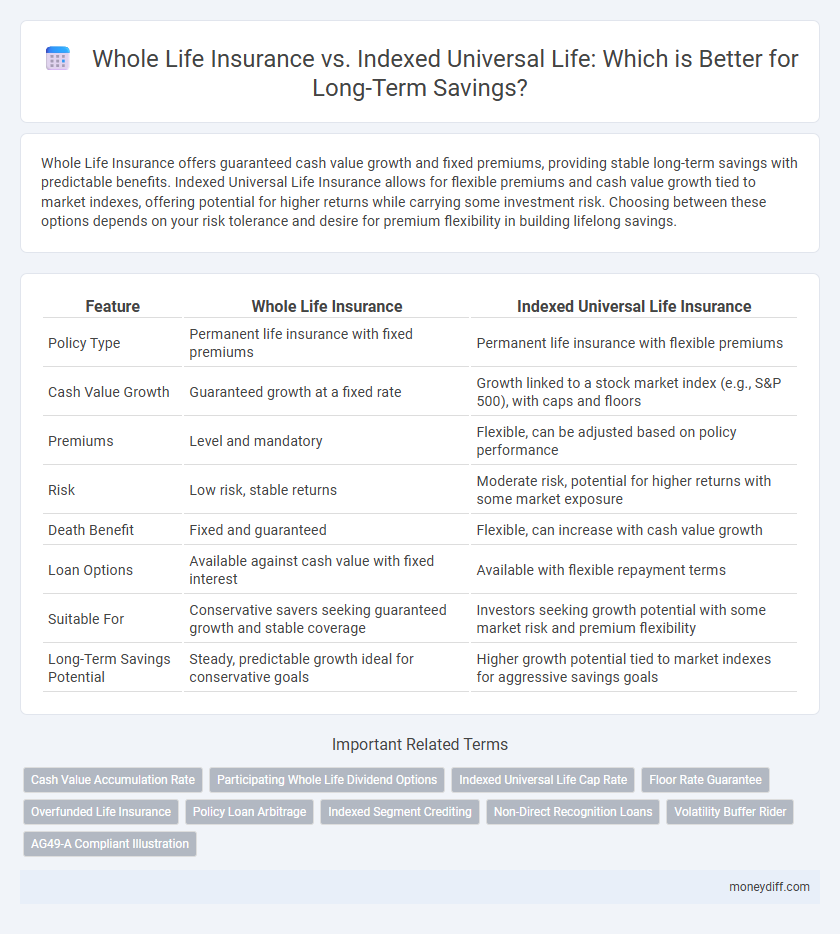

Whole Life Insurance offers guaranteed cash value growth and fixed premiums, providing stable long-term savings with predictable benefits. Indexed Universal Life Insurance allows for flexible premiums and cash value growth tied to market indexes, offering potential for higher returns while carrying some investment risk. Choosing between these options depends on your risk tolerance and desire for premium flexibility in building lifelong savings.

Table of Comparison

| Feature | Whole Life Insurance | Indexed Universal Life Insurance |

|---|---|---|

| Policy Type | Permanent life insurance with fixed premiums | Permanent life insurance with flexible premiums |

| Cash Value Growth | Guaranteed growth at a fixed rate | Growth linked to a stock market index (e.g., S&P 500), with caps and floors |

| Premiums | Level and mandatory | Flexible, can be adjusted based on policy performance |

| Risk | Low risk, stable returns | Moderate risk, potential for higher returns with some market exposure |

| Death Benefit | Fixed and guaranteed | Flexible, can increase with cash value growth |

| Loan Options | Available against cash value with fixed interest | Available with flexible repayment terms |

| Suitable For | Conservative savers seeking guaranteed growth and stable coverage | Investors seeking growth potential with some market risk and premium flexibility |

| Long-Term Savings Potential | Steady, predictable growth ideal for conservative goals | Higher growth potential tied to market indexes for aggressive savings goals |

Understanding Whole Life Insurance and Indexed Universal Life

Whole Life Insurance offers guaranteed cash value growth, fixed premiums, and death benefits, making it a stable choice for long-term savings with predictable returns. Indexed Universal Life (IUL) insurance allows policyholders to earn interest based on stock market index performance, providing potential for higher cash value accumulation with flexible premiums and adjustable death benefits. Understanding the balance between the guaranteed stability of Whole Life and the growth potential and flexibility of IUL is essential in aligning a long-term savings strategy with individual financial goals.

Key Features: Whole Life vs Indexed Universal Life

Whole Life Insurance offers guaranteed cash value growth, fixed premiums, and stable death benefits, making it ideal for conservative long-term savings. Indexed Universal Life Insurance provides flexible premiums, adjustable death benefits, and cash value linked to market indices, allowing potential for higher returns with some market risk. Both policies build cash value over time, but Indexed Universal Life offers greater growth potential and customization compared to the predictability of Whole Life.

Cash Value Growth and Accumulation

Whole Life Insurance provides guaranteed cash value growth with fixed premiums and steady accumulation, ensuring predictable long-term savings. Indexed Universal Life (IUL) offers potential for higher cash value growth by linking returns to market indexes while protecting against negative performance with a minimum guaranteed interest rate. Choosing between the two depends on risk tolerance, desired flexibility, and growth prospects for long-term financial goals.

Flexibility in Premium Payments

Whole Life Insurance offers fixed premium payments, providing stability and predictability over the policy's duration. Indexed Universal Life allows flexible premium payments, enabling policyholders to adjust contributions based on financial capacity or changing needs. This premium flexibility in Indexed Universal Life can enhance long-term savings growth by accommodating variable cash flow and investment opportunities.

Policy Loan and Withdrawal Options

Whole Life Insurance offers fixed policy loans with guaranteed interest rates and predictable repayment schedules, ensuring stable access to cash value without affecting the death benefit. Indexed Universal Life insurance provides flexible loan and withdrawal options tied to the policy's cash value performance, enabling potential growth but with greater variability in borrowing costs and impact on policy sustainability. Policyholders should consider loan interest rates, repayment terms, and the effect of withdrawals on long-term cash value and death benefits when choosing between these options for retirement planning.

Death Benefit Guarantees and Options

Whole Life Insurance provides fixed death benefit guarantees that remain stable throughout the policyholder's lifetime, offering predictable financial security for beneficiaries. Indexed Universal Life Insurance offers flexible death benefit options that can increase based on the policy's cash value growth linked to market indexes, balancing potential for higher returns with adjustable coverage amounts. Policyholders should evaluate their risk tolerance and long-term goals to choose between the guaranteed stability of Whole Life and the growth potential and flexibility of Indexed Universal Life.

Tax Advantages and Implications

Whole Life Insurance offers guaranteed cash value growth with tax-deferred accumulation and tax-free death benefits, ensuring predictable long-term savings stability. Indexed Universal Life Insurance provides potential for higher cash value growth linked to market indexes, maintaining tax-deferred status but with flexible premium payments and death benefits. Both policies allow tax-free loans and withdrawals up to the cost basis, but Indexed Universal Life requires careful management to avoid policy lapse and taxable events.

Cost Comparison: Premiums and Fees

Whole Life Insurance typically features fixed premiums and consistent fees, providing predictable long-term costs that suit individuals seeking stability in their savings strategy. Indexed Universal Life Insurance offers flexible premiums with fees that may vary based on market performance and policy adjustments, potentially resulting in lower initial costs but higher uncertainty over time. Evaluating the total cost including premium payments, administrative fees, and cost of insurance charges is crucial for effective comparison of these long-term savings options.

Suitability for Long-Term Savings Goals

Whole Life Insurance offers guaranteed cash value growth and fixed premiums, making it suitable for conservative, long-term savings goals with predictable outcomes. Indexed Universal Life combines flexible premiums and death benefits with cash value growth tied to market indices, appealing to individuals seeking potential higher returns alongside policyholder control. Choosing between these depends on risk tolerance, desired flexibility, and the importance of guaranteed versus market-linked growth in a long-term financial strategy.

Deciding Between Whole Life and Indexed Universal Life

Whole Life Insurance offers guaranteed cash value growth and fixed premiums, providing stability and predictable long-term savings. Indexed Universal Life Insurance allows for flexible premiums and potential cash value growth linked to market indexes, offering higher returns with some risk. Evaluate your risk tolerance, need for premium flexibility, and long-term financial goals to decide the best option for maximizing retirement savings and protection.

Related Important Terms

Cash Value Accumulation Rate

Whole Life Insurance offers a guaranteed cash value accumulation rate with stable growth tied to fixed premiums, providing predictable savings over time. Indexed Universal Life insurance features a cash value growth linked to a market index, allowing for potentially higher returns with flexible premiums but with less certainty in accumulation rates.

Participating Whole Life Dividend Options

Participating Whole Life Insurance offers policyholders dividend options such as cash payouts, paid-up additions, and premium reductions, enhancing long-term cash value growth and stability compared to Indexed Universal Life policies. These dividends, typically declared by mutual insurance companies, provide a predictable source of additional value, reinforcing financial security over decades.

Indexed Universal Life Cap Rate

Indexed Universal Life insurance offers flexible premium payments and potential cash value growth linked to a market index, with cap rates typically ranging from 6% to 12%, which limits the maximum return but protects against market losses. Whole Life insurance provides guaranteed cash value accumulation and fixed premiums, making Indexed Universal Life more attractive for long-term savings due to its growth potential tied to market performance within the cap rate constraints.

Floor Rate Guarantee

Whole Life Insurance offers a guaranteed floor rate, ensuring steady growth and protection against market downturns, while Indexed Universal Life Insurance links cash value growth to market indexes with a floor rate that prevents loss during negative index performance. Choosing between these depends on risk tolerance and desired flexibility, as Whole Life provides stable, predictable returns and Indexed Universal Life offers potential for higher gains with downside protection through the floor rate guarantee.

Overfunded Life Insurance

Overfunded Whole Life Insurance offers guaranteed cash value growth and stable premiums, making it a reliable choice for conservative long-term savings with predictable benefits. Indexed Universal Life Insurance provides potential for higher cash value accumulation linked to stock market indexes, combining flexibility in premiums and death benefits with the opportunity for tax-advantaged growth.

Policy Loan Arbitrage

Whole Life Insurance offers guaranteed cash value growth with stable policy loan rates, enabling predictable policy loan arbitrage, while Indexed Universal Life Insurance provides potential for higher returns linked to market indexes but with variable policy loan costs that may affect arbitrage benefits. Evaluating loan interest rates against cash value accumulation is crucial for optimizing long-term savings strategies in either policy type.

Indexed Segment Crediting

Indexed Universal Life insurance offers long-term savings growth linked to a market index, providing potential higher returns through indexed segment crediting without exposure to direct market losses. Whole Life insurance provides guaranteed cash value growth with fixed premiums, but typically lacks the upside potential available from the indexed crediting strategy in Indexed Universal Life policies.

Non-Direct Recognition Loans

Whole Life Insurance offers stable cash value growth with non-direct recognition loans, allowing policyholders to borrow against the policy without reducing dividends on the loaned portion. Indexed Universal Life insurance may provide higher potential returns tied to market indexes but often features direct recognition loans that reduce dividends on borrowed amounts, affecting long-term savings accumulation.

Volatility Buffer Rider

The Volatility Buffer Rider in Indexed Universal Life insurance provides a strategic advantage by smoothing out market fluctuations, offering a more stable growth potential compared to Whole Life Insurance's fixed cash value. This rider enhances long-term savings by mitigating downside risks while still allowing for indexed interest accumulation, making it a preferred choice for policyholders seeking both protection and growth.

AG49-A Compliant Illustration

Whole Life Insurance provides guaranteed cash value growth with fixed premiums and dividends, while Indexed Universal Life offers flexible premiums and potential cash value tied to a market index, both requiring AG49-A Compliant Illustrations to ensure transparency and compliance with insurance regulations. Accurate AG49-A Illustrations demonstrate long-term performance scenarios, helping policyholders compare the stable accumulation of Whole Life against the market-linked growth and flexibility of Indexed Universal Life for optimized savings strategies.

Whole Life Insurance vs Indexed Universal Life for long-term savings. Infographic