Car insurance typically offers comprehensive coverage based on fixed premiums regardless of miles driven, providing predictable costs and extensive protection. Pay-per-mile insurance charges based on actual driving distance, making it cost-effective for low-mileage drivers seeking savings without compromising essential coverage. Choosing between the two depends on driving habits, budget preferences, and the level of vehicle protection required.

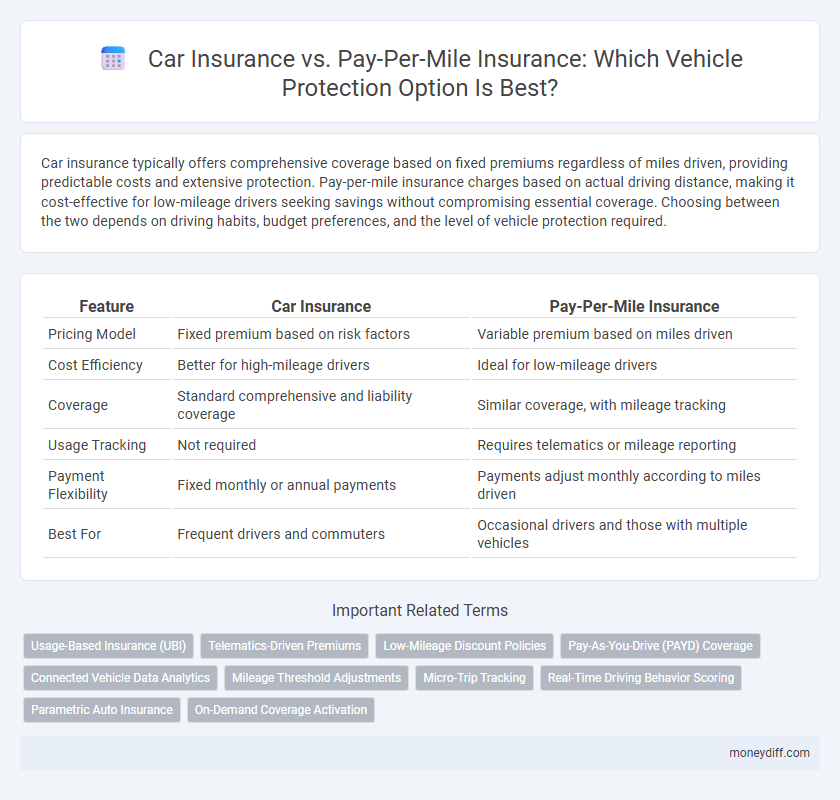

Table of Comparison

| Feature | Car Insurance | Pay-Per-Mile Insurance |

|---|---|---|

| Pricing Model | Fixed premium based on risk factors | Variable premium based on miles driven |

| Cost Efficiency | Better for high-mileage drivers | Ideal for low-mileage drivers |

| Coverage | Standard comprehensive and liability coverage | Similar coverage, with mileage tracking |

| Usage Tracking | Not required | Requires telematics or mileage reporting |

| Payment Flexibility | Fixed monthly or annual payments | Payments adjust monthly according to miles driven |

| Best For | Frequent drivers and commuters | Occasional drivers and those with multiple vehicles |

Understanding Traditional Car Insurance

Traditional car insurance offers comprehensive coverage based on fixed premiums calculated from factors such as driver history, vehicle type, and annual mileage estimates. This model provides predictable monthly or annual payments regardless of actual miles driven, making it convenient for regular commuters. Policyholders benefit from extensive protection options, including liability, collision, and comprehensive coverage, ensuring broad financial security.

What is Pay-Per-Mile Insurance?

Pay-per-mile insurance charges drivers based on the exact number of miles they drive, making it a cost-effective option for low-mileage vehicles. Unlike traditional car insurance, which requires a fixed premium regardless of usage, pay-per-mile plans offer personalized rates that can significantly reduce expenses for infrequent drivers. This model uses telematics technology to track mileage, ensuring accurate billing and enhancing transparency in vehicle protection costs.

Key Differences Between Standard and Pay-Per-Mile Policies

Standard car insurance typically charges a fixed premium based on estimated annual mileage, driving history, and vehicle type, providing consistent coverage regardless of actual miles driven. Pay-per-mile insurance calculates costs primarily on the exact number of miles driven, offering lower rates for low-mileage drivers and promoting cost efficiency for infrequent use. Policyholders choosing pay-per-mile plans benefit from increased transparency and potential savings, while standard policies offer predictable payments and broader coverage options.

Cost Comparison: Which Option Saves More?

Pay-per-mile insurance generally offers more cost savings for low-mileage drivers by charging based on actual miles driven, potentially lowering premiums compared to traditional car insurance with fixed rates. Traditional car insurance can be more expensive for infrequent drivers due to flat fees that don't account for reduced usage, whereas pay-per-mile policies provide flexibility and potential savings for those who drive less than the average. However, frequent drivers may benefit more from conventional car insurance as high mileage under pay-per-mile plans could lead to increased overall costs.

Coverage Types in Both Insurance Models

Car insurance typically offers comprehensive coverage including liability, collision, and comprehensive protection, covering a wide range of incidents regardless of mileage. Pay-per-mile insurance primarily focuses on liability with optional add-ons for collision and comprehensive, making it cost-effective for low-mileage drivers. Both models provide essential vehicle protection, but coverage depth varies based on usage patterns and selected policy options.

Who Benefits Most From Pay-Per-Mile Insurance?

Pay-per-mile insurance offers significant savings for low-mileage drivers, including urban residents, retirees, and remote workers who drive fewer than 10,000 miles annually. This model benefits those seeking customized premiums based on actual road usage rather than traditional flat rates, reducing costs linked to infrequent driving. Pay-per-mile policies appeal especially to environmentally conscious individuals and budget-sensitive consumers aiming to optimize vehicle protection without overpaying for unused coverage.

Pros and Cons of Traditional Car Insurance

Traditional car insurance offers comprehensive coverage options including liability, collision, and comprehensive protection, providing broad security regardless of mileage. Premiums are predictable due to fixed rates, simplifying budgeting for most drivers. Higher costs and potential overpayment for low-mileage drivers represent significant drawbacks compared to more usage-based models like pay-per-mile insurance.

Pros and Cons of Pay-Per-Mile Insurance

Pay-per-mile insurance offers significant cost savings for low-mileage drivers by charging premiums based on actual miles driven, promoting fairness and budget control. However, it may lead to higher expenses for frequent travelers and complicates billing with the need for accurate mileage tracking through telematics devices. Limited availability and restrictions on vehicle types can also reduce its suitability compared to traditional car insurance options.

How to Choose the Right Vehicle Protection Plan

Choosing the right vehicle protection plan depends on your driving habits and budget, with traditional car insurance offering comprehensive coverage for frequent drivers while pay-per-mile insurance benefits low-mileage drivers by charging based on actual miles driven. Evaluating factors such as average annual mileage, coverage needs, and cost savings potential can help determine the most cost-effective and tailored policy. Comparing policy limits, deductibles, and additional coverage options ensures the selected insurance aligns with both financial goals and protection requirements.

Tips for Saving on Car Insurance Premiums

Choosing pay-per-mile insurance can significantly reduce premiums for drivers who log fewer miles annually, as rates are directly tied to usage rather than estimated risk factors. Maintaining a clean driving record, bundling multiple insurance policies, and opting for higher deductibles also contribute to lowering car insurance costs. Regularly reviewing and comparing insurance providers ensures access to competitive rates and tailored coverage options that align with individual driving habits and budgets.

Related Important Terms

Usage-Based Insurance (UBI)

Usage-Based Insurance (UBI) such as Pay-per-mile insurance offers personalized vehicle protection by calculating premiums based on actual miles driven, contrasting traditional car insurance that charges fixed rates regardless of usage. This model incentivizes low-mileage drivers with cost savings while providing insurers with accurate data on driving habits for risk assessment.

Telematics-Driven Premiums

Telematics-driven premiums in car insurance use real-time driving data to customize rates based on individual behavior, offering potential savings for safe drivers compared to traditional pay-per-mile insurance models. While pay-per-mile insurance charges based solely on distance driven, telematics incorporates variables such as speed, acceleration, and braking patterns, promoting safer driving habits and more precise risk assessment.

Low-Mileage Discount Policies

Low-mileage discount policies in car insurance offer significant savings for drivers who log fewer miles annually, making traditional coverage more affordable for occasional drivers. Pay-per-mile insurance directly charges based on actual mileage driven, providing transparent cost benefits for low-mileage vehicle owners by aligning premiums closely with road usage.

Pay-As-You-Drive (PAYD) Coverage

Pay-As-You-Drive (PAYD) car insurance offers personalized vehicle protection by charging premiums based on actual miles driven, providing cost savings for low-mileage drivers compared to traditional flat-rate car insurance. PAYD coverage aligns insurance costs with usage, promoting fuel efficiency and reducing overall expenses by incentivizing less frequent driving.

Connected Vehicle Data Analytics

Connected vehicle data analytics enhances pay-per-mile insurance by providing real-time driving behavior insights, enabling personalized premiums based on actual usage rather than fixed rates. This data-driven approach contrasts with traditional car insurance, which relies on generalized risk profiles and often results in less accurate pricing for low-mileage or infrequent drivers.

Mileage Threshold Adjustments

Pay-per-mile insurance offers dynamic mileage threshold adjustments, allowing drivers to tailor premiums based on actual miles driven, unlike traditional car insurance that relies on fixed mileage estimates. This flexibility reduces costs for low-mileage vehicle owners while ensuring adequate coverage adjustments as driving habits change.

Micro-Trip Tracking

Pay-per-mile insurance leverages micro-trip tracking technology to monitor and charge based on actual miles driven, offering cost efficiency for low-mileage drivers compared to traditional car insurance with fixed premiums. By analyzing each short trip's data, pay-per-mile plans provide tailored coverage that reflects real driving behavior, promoting fairer pricing and enhanced vehicle protection.

Real-Time Driving Behavior Scoring

Real-time driving behavior scoring in pay-per-mile insurance dynamically adjusts premiums based on factors such as speed, acceleration, and braking patterns, offering more personalized and potentially lower costs than traditional car insurance. This usage-based model incentivizes safer driving habits by providing immediate feedback and rewards, enhancing vehicle protection while optimizing expenses according to actual road usage.

Parametric Auto Insurance

Parametric auto insurance offers a data-driven approach to vehicle protection by triggering payouts based on predefined parameters such as mileage, weather conditions, or collision impact, enabling personalized car insurance coverage. Unlike traditional car insurance, pay-per-mile models utilize real-time telematics data to calculate premiums according to actual driving behavior, reducing costs for low-mileage drivers while maintaining comprehensive risk management.

On-Demand Coverage Activation

Pay-per-mile insurance offers on-demand coverage activation tailored to low-mileage drivers, allowing policyholders to pay solely for the miles driven, resulting in cost savings compared to traditional car insurance with fixed premiums. This flexible approach uses telematics to track mileage in real time, providing precise billing and customizable protection that adapts to varying driving patterns.

Car insurance vs Pay-per-mile insurance for vehicle protection. Infographic