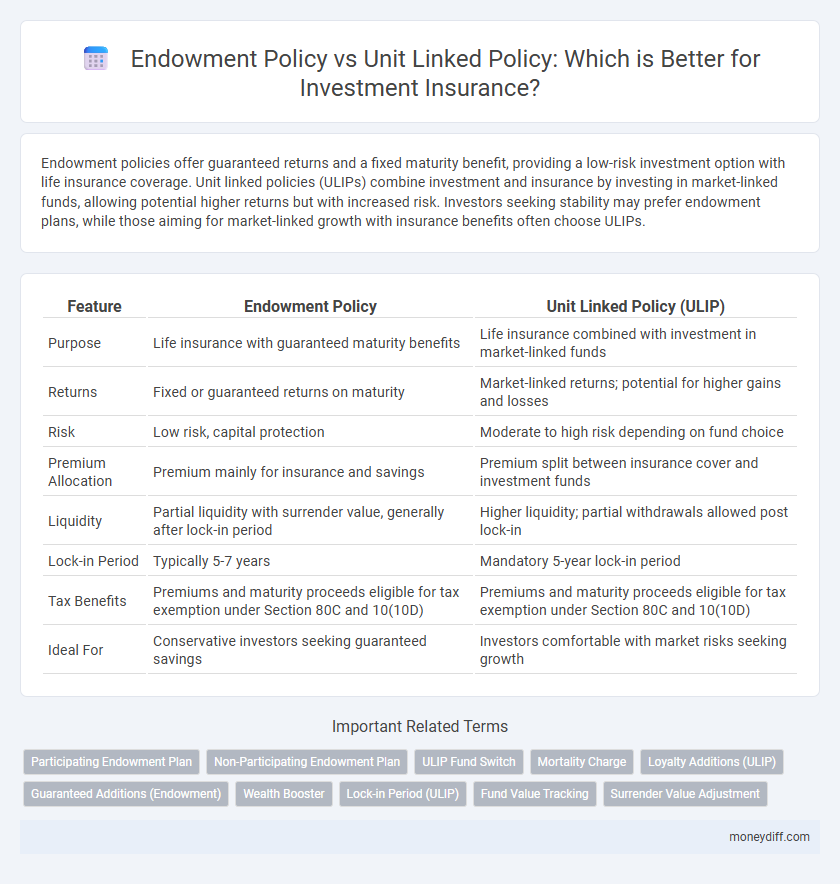

Endowment policies offer guaranteed returns and a fixed maturity benefit, providing a low-risk investment option with life insurance coverage. Unit linked policies (ULIPs) combine investment and insurance by investing in market-linked funds, allowing potential higher returns but with increased risk. Investors seeking stability may prefer endowment plans, while those aiming for market-linked growth with insurance benefits often choose ULIPs.

Table of Comparison

| Feature | Endowment Policy | Unit Linked Policy (ULIP) |

|---|---|---|

| Purpose | Life insurance with guaranteed maturity benefits | Life insurance combined with investment in market-linked funds |

| Returns | Fixed or guaranteed returns on maturity | Market-linked returns; potential for higher gains and losses |

| Risk | Low risk, capital protection | Moderate to high risk depending on fund choice |

| Premium Allocation | Premium mainly for insurance and savings | Premium split between insurance cover and investment funds |

| Liquidity | Partial liquidity with surrender value, generally after lock-in period | Higher liquidity; partial withdrawals allowed post lock-in |

| Lock-in Period | Typically 5-7 years | Mandatory 5-year lock-in period |

| Tax Benefits | Premiums and maturity proceeds eligible for tax exemption under Section 80C and 10(10D) | Premiums and maturity proceeds eligible for tax exemption under Section 80C and 10(10D) |

| Ideal For | Conservative investors seeking guaranteed savings | Investors comfortable with market risks seeking growth |

Understanding Endowment Policies: An Overview

Endowment policies are life insurance contracts designed to provide a lump sum payment on maturity or in the event of the policyholder's death, combining savings with insurance. These policies offer guaranteed returns, making them a low-risk investment option compared to market-linked plans. The emphasis on capital protection and assured maturity benefits distinguishes endowment policies from unit linked insurance plans (ULIPs), which are subject to market fluctuations.

What Are Unit Linked Insurance Policies (ULIPs)?

Unit Linked Insurance Policies (ULIPs) combine investment and insurance by allocating premiums into various funds like equity, debt, or balanced schemes, enabling capital growth alongside life coverage. ULIPs offer flexibility in premium payments, fund selection, and switching options to optimize returns based on market conditions and risk appetite. These policies also provide tax benefits under Section 80C and tax-free maturity proceeds under Section 10(10D) of the Income Tax Act, making them a popular choice for long-term wealth creation and financial protection.

Key Differences Between Endowment and ULIP Plans

Endowment policies provide guaranteed maturity benefits along with life cover, making them suitable for conservative investors seeking fixed returns and risk protection. Unit Linked Insurance Plans (ULIPs) combine investment and insurance by allocating funds to market-linked assets, offering potential higher returns but with higher risk and market exposure. The key differences lie in the risk profile, return potential, and transparency of fund allocation, with endowments focusing on capital preservation and ULIPs on wealth creation through market participation.

Investment Structure: Guaranteed vs Market-Linked Returns

Endowment policies offer guaranteed maturity benefits and fixed returns, ensuring a predefined sum upon policy completion, making them suitable for risk-averse investors seeking stability. Unit Linked Policies (ULIPs) invest in market-linked instruments like equities and bonds, with returns fluctuating based on market performance, appealing to investors aiming for higher growth potential and willing to accept volatility. The core difference lies in endowment's assured payouts versus ULIP's variable returns driven by underlying investment funds.

Risk Factors: Stability vs Market Volatility

Endowment policies offer stable returns with guaranteed maturity benefits, making them suitable for conservative investors seeking predictable outcomes. Unit Linked Policies (ULIPs) expose investors to market volatility by linking returns to equity or debt fund performance, resulting in potentially higher but uncertain gains. Understanding the risk tolerance and investment horizon is crucial when choosing between the stability of endowment policies and the fluctuating returns of ULIPs.

Flexibility and Customization Options in Policies

Endowment policies offer fixed maturity benefits with limited flexibility in investment choices, making them suitable for conservative investors seeking guaranteed returns. Unit Linked Insurance Plans (ULIPs) provide extensive customization options, allowing policyholders to switch between equity, debt, and balanced funds based on risk appetite and market conditions. The enhanced flexibility in ULIPs enables dynamic portfolio management, aligning investment strategies with changing financial goals.

Insurance Coverage and Death Benefits

Endowment policies provide guaranteed maturity benefits along with fixed insurance coverage, ensuring a specified sum is paid out either on death or maturity. Unit Linked Insurance Policies (ULIPs) combine investment with insurance, offering market-linked returns with variable death benefits based on fund performance. Endowment plans typically have higher insurance coverage compared to ULIPs, which allocate a portion of premiums to investments and insurance premiums, affecting the death benefit amount.

Tax Benefits: Comparing Endowment and ULIP Policies

Endowment policies offer tax benefits under Section 80C with a maximum deduction limit of Rs1.5 lakh, and the maturity proceeds are generally exempt from tax under Section 10(10D). Unit Linked Insurance Plans (ULIPs) also qualify for deductions under Section 80C up to Rs1.5 lakh, but gains upon maturity are tax-exempt only if the premium paid does not exceed 10% of the sum assured; otherwise, gains become taxable as capital gains. Both policies provide tax-efficient investment options, but ULIPs offer greater flexibility in fund choice and risk, impacting the overall tax treatment of returns.

Ideal Investor Profiles for Each Policy Type

Endowment policies suit risk-averse investors seeking guaranteed maturity benefits and disciplined savings with moderate returns. Unit linked policies attract those comfortable with market risks aiming for potentially higher returns through investment in equities and bonds. Investors prioritizing capital protection and steady growth prefer endowment plans, whereas those pursuing wealth accumulation and flexibility opt for unit linked plans.

How to Choose: Endowment Policy or ULIP for Your Goals?

Choosing between an Endowment Policy and a Unit Linked Insurance Plan (ULIP) depends on your financial goals, risk tolerance, and investment horizon. Endowment policies offer guaranteed returns and life cover, making them suitable for conservative investors seeking stable growth and maturity benefits. ULIPs combine investment and insurance by allowing exposure to equity and debt markets, appealing to investors aiming for higher returns with moderate to high risk preferences.

Related Important Terms

Participating Endowment Plan

A Participating Endowment Plan offers guaranteed returns along with bonuses derived from the insurer's profits, providing a stable investment with the security of life coverage. In contrast, a Unit Linked Policy (ULIP) combines investment and insurance by allocating premiums to market-linked funds, presenting higher growth potential but with greater market risk exposure.

Non-Participating Endowment Plan

A Non-Participating Endowment Policy offers guaranteed maturity benefits without dividends, providing predictable returns and risk-averse investment security, whereas a Unit Linked Insurance Plan (ULIP) integrates investment and insurance by linking premiums to market-based funds, enabling growth potential with higher risk exposure. Investors seeking stable, fixed returns may prefer Non-Participating Endowment Plans, while those aiming for market-linked growth might opt for ULIPs.

ULIP Fund Switch

Unit Linked Insurance Plans (ULIPs) offer the flexibility to switch between equity, debt, and balanced funds, allowing investors to optimize returns based on market conditions and risk appetite. In contrast, Endowment policies provide fixed benefits without fund-switching options, focusing more on guaranteed maturity returns than market-linked growth.

Mortality Charge

Endowment policies typically have a fixed mortality charge that reflects the guaranteed payout upon survival or death, offering stable risk coverage with predictable costs. Unit linked policies (ULIPs) charge mortality fees based on the policyholder's age and sum assured, varying with market-linked fund performance and providing flexible investment options alongside life cover.

Loyalty Additions (ULIP)

Loyalty Additions in Unit Linked Insurance Plans (ULIPs) significantly enhance wealth accumulation by crediting additional units based on the policyholder's tenure and premiums paid, which is absent in traditional Endowment Policies. This feature in ULIPs leverages market-linked growth potential and rewards long-term commitment, offering superior investment returns compared to the fixed benefits of Endowment Policies.

Guaranteed Additions (Endowment)

Endowment policies provide Guaranteed Additions, ensuring a fixed growth component regardless of market performance, which enhances the policyholder's maturity benefits. In contrast, Unit Linked Policies (ULIPs) offer market-linked returns without guaranteed additions, making their maturity value dependent on investment performance.

Wealth Booster

Endowment policies offer guaranteed returns and a lump sum payout at maturity, providing a stable wealth booster through disciplined savings and risk protection. Unit Linked Policies (ULIPs) combine investment and life insurance, allowing policyholders to potentially amplify wealth growth via market-linked funds while maintaining insurance coverage.

Lock-in Period (ULIP)

Endowment policies typically have no lock-in period, allowing policyholders flexibility to withdraw funds prematurely, whereas Unit Linked Insurance Plans (ULIPs) enforce a mandatory lock-in period of five years, promoting long-term investment discipline and potential tax benefits. This lock-in period in ULIPs is crucial for investors aiming for wealth accumulation through market-linked returns while benefiting from insurance coverage.

Fund Value Tracking

Endowment policies offer a guaranteed maturity benefit with fixed returns, making fund value predictable but generally lower compared to market-linked growth. Unit Linked Policies (ULIPs) provide fund value tracking based on the performance of underlying market-linked investment funds, allowing potential for higher returns but with greater variability in fund value.

Surrender Value Adjustment

Endowment policies typically offer a guaranteed surrender value that increases over time based on the sum assured and premiums paid, providing a more predictable exit option for policyholders. Unit Linked Policies (ULIPs) have a surrender value dependent on the market value of the underlying investment funds, which can fluctuate significantly and may result in lower or higher returns at the time of surrender.

Endowment Policy vs Unit Linked Policy for investment insurance. Infographic