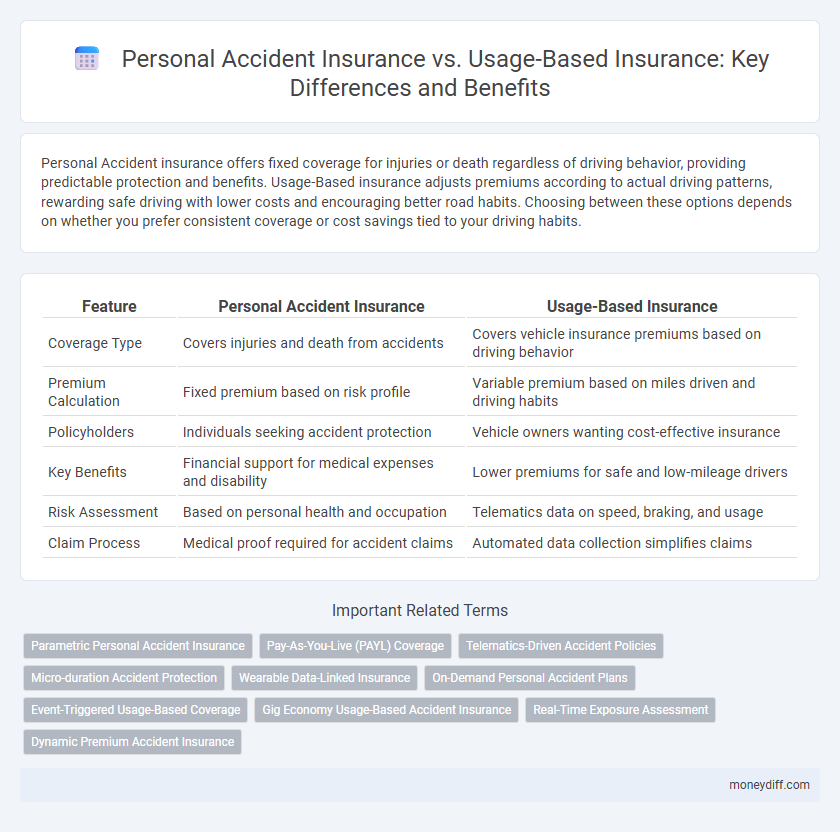

Personal Accident insurance offers fixed coverage for injuries or death regardless of driving behavior, providing predictable protection and benefits. Usage-Based insurance adjusts premiums according to actual driving patterns, rewarding safe driving with lower costs and encouraging better road habits. Choosing between these options depends on whether you prefer consistent coverage or cost savings tied to your driving habits.

Table of Comparison

| Feature | Personal Accident Insurance | Usage-Based Insurance |

|---|---|---|

| Coverage Type | Covers injuries and death from accidents | Covers vehicle insurance premiums based on driving behavior |

| Premium Calculation | Fixed premium based on risk profile | Variable premium based on miles driven and driving habits |

| Policyholders | Individuals seeking accident protection | Vehicle owners wanting cost-effective insurance |

| Key Benefits | Financial support for medical expenses and disability | Lower premiums for safe and low-mileage drivers |

| Risk Assessment | Based on personal health and occupation | Telematics data on speed, braking, and usage |

| Claim Process | Medical proof required for accident claims | Automated data collection simplifies claims |

Understanding Personal Accident Insurance: Coverage and Benefits

Personal Accident Insurance provides financial protection against injuries, disability, or death caused by unforeseen accidents, covering medical expenses, hospitalization, and compensation for loss of income. It offers fixed-sum benefits regardless of fault, ensuring policyholders or their beneficiaries receive timely payouts. This type of insurance is vital for individuals seeking comprehensive accident coverage beyond third-party liabilities.

Introduction to Usage-Based Insurance: How It Works

Usage-Based Insurance (UBI) employs telematics technology to monitor drivers' real-time behavior, such as speed, braking patterns, and mileage, enabling insurers to tailor premiums based on actual risk profiles. Unlike traditional Personal Accident insurance that offers fixed coverage regardless of driving habits, UBI rewards safe driving with potential discounts and promotes risk reduction through continuous feedback. By leveraging data analytics, UBI improves pricing accuracy and incentivizes motorists to adopt safer driving practices, enhancing both cost efficiency and road safety.

Key Differences Between Personal Accident and Usage-Based Insurance

Personal Accident insurance offers fixed coverage for injuries and disabilities due to accidents, typically with predetermined sums insured regardless of driving behavior or mileage. Usage-Based Insurance (UBI) relies on telematics data to adjust premiums based on actual driving patterns, such as distance driven, speed, and braking habits, providing personalized risk assessment and cost savings for low-risk drivers. Key differences lie in the pricing methodology, risk evaluation, and policy customization, where Personal Accident is static and event-specific, while UBI is dynamic and behavior-driven.

Pros and Cons of Personal Accident Insurance

Personal accident insurance offers financial protection against injuries resulting from accidents, providing lump-sum payouts for medical expenses, disability, or death, which ensures immediate support for policyholders and their families. However, it often comes with fixed premiums that do not adjust based on individual risk behavior, potentially leading to overpayment for low-risk individuals. Unlike usage-based insurance, which bases premiums on actual driving habits, personal accident plans lack personalized pricing but offer broad coverage without the need for telematics devices or continuous monitoring.

Advantages and Limitations of Usage-Based Insurance Policies

Usage-Based Insurance (UBI) policies leverage telematics technology to monitor driving behavior, offering personalized premiums that reward safe driving habits and potentially lower costs. These policies provide advantages such as increased transparency, real-time feedback for risk reduction, and incentivization of responsible driving. Limitations include privacy concerns, potential inaccuracies in data capture, and limited applicability for infrequent drivers who may not benefit from usage-based discounts.

Cost Comparison: Personal Accident vs Usage-Based Insurance

Personal Accident insurance typically offers a fixed premium based on coverage limits and risk factors, providing predictable costs regardless of driving behavior. Usage-Based Insurance (UBI) calculates premiums dynamically using telematics data, often resulting in lower costs for safe drivers due to mileage and driving habits. Comparing cost efficiency, UBI can be more economical for low-mileage or cautious drivers, while Personal Accident insurance maintains steady pricing for consistent coverage.

Suitability: Which Insurance Type Matches Your Lifestyle?

Personal Accident insurance offers comprehensive coverage for unexpected injuries and disabilities, ideal for individuals with high-risk occupations or active lifestyles. Usage-Based Insurance (UBI) tailors premiums based on actual driving behavior, making it suitable for cautious drivers seeking cost-effective auto coverage. Evaluating daily habits and risk exposure determines which option aligns best with personal safety needs and budget considerations.

Claims Process: What to Expect From Each Insurance Option

Personal Accident insurance typically involves a straightforward claims process based on documented injuries, medical reports, and accident verification, allowing for quick settlements. Usage-Based insurance claims require detailed telematics data analysis, assessing driving behavior and incident specifics, which can extend evaluation time. The choice impacts claim timelines and complexity, with Personal Accident favoring fixed payouts and Usage-Based focusing on evidence-driven assessments.

Factors to Consider When Choosing Between Personal Accident and Usage-Based Insurance

When choosing between Personal Accident and Usage-Based Insurance, consider factors such as risk coverage scope, premium calculation, and individual driving behavior. Personal Accident Insurance provides lump-sum benefits for injuries or death regardless of driving patterns, ideal for broad protection. Usage-Based Insurance offers dynamic premiums based on real-time driving metrics, benefiting safe drivers and promoting cost efficiency.

Expert Tips for Optimizing Your Insurance Strategy

Personal accident insurance provides fixed coverage for injuries regardless of driving behavior, while usage-based insurance tailors premiums based on real-time driving data, rewarding safer habits. Experts recommend combining personal accident coverage with usage-based policies to maximize protection and cost efficiency. Analyzing driving patterns and accident risks through telematics can significantly optimize your overall insurance strategy.

Related Important Terms

Parametric Personal Accident Insurance

Parametric Personal Accident Insurance offers fixed payouts triggered by predefined parameters such as injury severity or hospitalization duration, providing faster claims settlement compared to traditional Personal Accident insurance. Usage-Based insurance, while reliant on monitored behavior for premium calculation, lacks the predefined trigger mechanism that ensures immediate compensation in parametric models.

Pay-As-You-Live (PAYL) Coverage

Pay-As-You-Live (PAYL) coverage innovatively links Personal Accident insurance premiums to real-time user behavior, offering a more personalized and cost-effective alternative to traditional coverage. By leveraging telematics data, PAYL adjusts rates based on lifestyle factors and accident risk, enhancing policyholder engagement and promoting safer living habits.

Telematics-Driven Accident Policies

Telematics-driven accident policies leverage real-time data from vehicle sensors and GPS to personalize premiums based on actual driving behavior, offering more accurate risk assessment compared to traditional personal accident insurance. Usage-based insurance incentivizes safer driving by monitoring factors such as speed, braking patterns, and mileage, resulting in dynamic coverage and potentially lower costs for responsible drivers.

Micro-duration Accident Protection

Micro-duration accident protection offers targeted coverage for brief periods of heightened risk, ideal for personal accident insurance by providing flexible, event-specific safeguards. Usage-based insurance leverages telematics and real-time data to dynamically adjust premiums and coverage based on user behavior, enhancing cost efficiency and personalization.

Wearable Data-Linked Insurance

Wearable data-linked insurance enhances personal accident coverage by providing real-time monitoring of physical activity, enabling precise risk assessment and personalized premium adjustments. Usage-based insurance leverages continuous wearable data to detect behavioral patterns and improve claim accuracy, offering tailored protection that aligns with individual lifestyle and accident risk profiles.

On-Demand Personal Accident Plans

On-demand personal accident plans offer flexible insurance coverage activated only when needed, contrasting with traditional usage-based insurance that relies on continuous monitoring of driving behavior or activity levels. These plans provide cost-effective, tailored protection for individuals seeking immediate, situational risk coverage without long-term commitments or extensive data tracking.

Event-Triggered Usage-Based Coverage

Event-triggered usage-based insurance coverage activates protection specifically during defined risk events such as driving, offering cost-efficient premiums by charging only when exposure occurs. Personal accident insurance provides a fixed benefit independent of activity, whereas usage-based models dynamically adjust coverage and pricing based on real-time behavior and event-specific data.

Gig Economy Usage-Based Accident Insurance

Gig Economy Usage-Based Accident Insurance adapts premiums and coverage based on real-time data from work patterns and risk exposure, offering tailored protection for gig workers compared to traditional Personal Accident Insurance, which typically provides fixed coverage regardless of activity level. Leveraging telematics and mobile app integration, usage-based policies enhance accuracy in risk assessment, reduce costs, and increase claims efficiency for flexible, on-demand labor markets.

Real-Time Exposure Assessment

Personal Accident insurance provides fixed coverage based on pre-determined risk factors, while Usage-Based Insurance (UBI) utilizes telematics and real-time data to dynamically assess driver behavior and exposure, enabling personalized premiums that reflect actual risk. Real-time exposure assessment in UBI enhances risk accuracy, improves loss prevention, and incentivizes safer driving habits through continuous monitoring.

Dynamic Premium Accident Insurance

Dynamic premium accident insurance adjusts rates based on real-time data such as driving behavior, usage frequency, and risk exposure, offering a personalized alternative to traditional personal accident policies with fixed premiums. This usage-based model enhances affordability and risk accuracy by continuously monitoring factors like speed, braking patterns, and mileage.

Personal Accident vs Usage-Based for insurance. Infographic