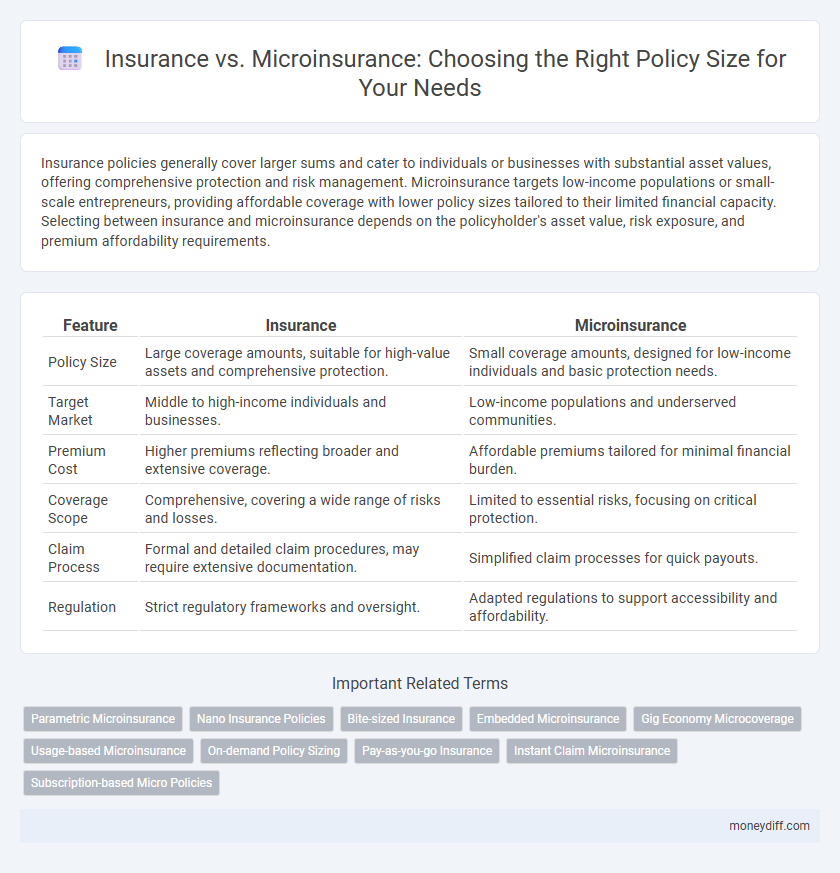

Insurance policies generally cover larger sums and cater to individuals or businesses with substantial asset values, offering comprehensive protection and risk management. Microinsurance targets low-income populations or small-scale entrepreneurs, providing affordable coverage with lower policy sizes tailored to their limited financial capacity. Selecting between insurance and microinsurance depends on the policyholder's asset value, risk exposure, and premium affordability requirements.

Table of Comparison

| Feature | Insurance | Microinsurance |

|---|---|---|

| Policy Size | Large coverage amounts, suitable for high-value assets and comprehensive protection. | Small coverage amounts, designed for low-income individuals and basic protection needs. |

| Target Market | Middle to high-income individuals and businesses. | Low-income populations and underserved communities. |

| Premium Cost | Higher premiums reflecting broader and extensive coverage. | Affordable premiums tailored for minimal financial burden. |

| Coverage Scope | Comprehensive, covering a wide range of risks and losses. | Limited to essential risks, focusing on critical protection. |

| Claim Process | Formal and detailed claim procedures, may require extensive documentation. | Simplified claim processes for quick payouts. |

| Regulation | Strict regulatory frameworks and oversight. | Adapted regulations to support accessibility and affordability. |

Understanding Insurance and Microinsurance: Key Differences

Insurance typically involves larger policy sizes with comprehensive coverage options aimed at individuals or businesses seeking extensive financial protection. Microinsurance offers smaller policy sizes tailored to low-income populations, providing affordable, basic coverage for risks such as health, life, and property. Understanding the distinction between these policy sizes helps in selecting appropriate coverage solutions based on financial capacity and risk exposure.

Policy Size Comparison: Insurance vs Microinsurance

Traditional insurance policies typically involve higher premiums and coverage amounts, catering to individuals or businesses with substantial financial assets or risks. Microinsurance offers smaller policy sizes designed to provide affordable protection for low-income populations or those with limited exposure, featuring lower premiums and reduced coverage limits. The policy size comparison highlights a significant disparity, where standard insurance covers larger risks and values, while microinsurance targets accessibility and financial inclusion with scaled-down policy options.

Coverage Limits in Traditional Insurance Policies

Traditional insurance policies typically feature higher coverage limits, often ranging from tens of thousands to millions of dollars, providing substantial financial protection against significant losses. In contrast, microinsurance targets low-income populations with smaller coverage limits, usually between a few hundred to a few thousand dollars, designed to cover specific risks like health, agriculture, or life events. The disparity in coverage limits reflects the policy size and affordability, making microinsurance a more accessible option for underserved markets while traditional insurance caters to broader, high-value asset protection.

Microinsurance: Tailored Coverage for Low-Income Groups

Microinsurance provides affordable, tailored coverage specifically designed for low-income groups who typically cannot afford traditional insurance policies with higher premiums and extensive coverage. It offers smaller policy sizes with simplified terms, ensuring essential protection against risks like health emergencies, natural disasters, and crop failure. By focusing on accessibility and cost-effectiveness, microinsurance bridges the gap between vulnerable communities and financial security.

Premium Costs: Scale and Affordability

Traditional insurance policies typically involve higher premium costs due to larger coverage amounts and extensive risk pooling, making them less accessible for low-income individuals. Microinsurance offers scaled-down coverage with significantly lower premiums tailored to affordable levels, improving financial inclusion in underserved markets. Premium costs in microinsurance reflect its design for smaller policy sizes, enabling broader access without compromising essential protection.

Claim Process and Payout Size: What to Expect

Insurance policies typically involve larger policy sizes with comprehensive claim processes that may require extensive documentation and longer approval times, resulting in higher payout amounts suited for significant financial protection. Microinsurance offers smaller policy sizes with streamlined claim procedures designed for quick approvals and minimal paperwork, providing faster payouts that cater to low-income individuals seeking affordable coverage. Expect microinsurance to prioritize accessibility and speed, while traditional insurance emphasizes detailed assessments and substantial financial compensation.

Suitability of Policy Size for Diverse Financial Needs

Traditional insurance policies typically involve larger coverage amounts suitable for individuals or businesses with significant financial assets, while microinsurance offers smaller, affordable policy sizes tailored to low-income populations. Microinsurance addresses the financial constraints of underserved communities by providing essential coverage for risks like health, agriculture, or property at minimal premiums. Selecting the appropriate policy size depends on the insured's financial capacity, risk exposure, and need for protection against specific vulnerabilities.

Accessibility: Insurance vs Microinsurance Options

Microinsurance offers greater accessibility for low-income individuals by providing affordable policy sizes tailored to their specific needs, often with simplified enrollment processes and lower premiums. Traditional insurance policies typically require higher premiums and larger coverage amounts, making them less attainable for economically vulnerable populations. This accessibility gap makes microinsurance a crucial solution for expanding financial protection to underserved communities.

Impact of Policy Size on Risk Coverage

Larger insurance policies typically offer broader risk coverage and higher financial protection compared to microinsurance, which targets low-income populations with smaller, more affordable premiums and limited coverage scopes. Policy size directly influences the extent of risk transfer, where substantial policies cover diverse and high-value risks, reducing individual financial burden significantly. Microinsurance fills critical coverage gaps by providing essential protection against specific risks while maintaining accessibility and affordability for underserved segments.

Choosing the Right Policy Size: Factors to Consider

Choosing the right policy size in insurance versus microinsurance hinges on factors like coverage needs, premium affordability, and risk exposure. Traditional insurance policies typically offer higher coverage amounts suited for significant asset protection, while microinsurance provides lower premiums with limited coverage ideal for low-income individuals. Assessing income stability, asset value, and potential financial loss ensures selecting a policy size that balances adequate protection and cost-effectiveness.

Related Important Terms

Parametric Microinsurance

Parametric microinsurance offers a highly specialized solution for low-income groups facing small-scale risks by providing pre-defined payouts based on specific triggers, contrasting with traditional insurance that typically involves larger policy sizes and indemnity-based claims processes. This targeted approach enables faster settlements and affordability, making parametric microinsurance particularly effective in sectors vulnerable to natural disasters such as agriculture and climate-related events.

Nano Insurance Policies

Nano insurance policies typically cover extremely small sums insured, often under $100, making them suitable for microinsurance frameworks aimed at low-income individuals. Traditional insurance policies usually involve higher coverage amounts and premiums, whereas nano insurance offers affordable, minimal coverage to address very specific risks at the grassroots level.

Bite-sized Insurance

Bite-sized insurance offers microinsurance policies designed for low-income individuals, providing affordable, limited coverage with smaller premiums and sums insured compared to traditional insurance policies. These compact plans tailor risk protection to specific needs, enabling broader access to essential financial security in underserved markets.

Embedded Microinsurance

Embedded microinsurance offers affordable, small-scale coverage integrated directly into everyday products or services, making it accessible for low-income individuals with limited policy sizes. Traditional insurance policies typically require higher premiums and larger coverage amounts, often limiting accessibility for underserved populations.

Gig Economy Microcoverage

Gig economy microcoverage offers tailored microinsurance policies with lower premiums and smaller coverage amounts compared to traditional insurance, aligning with the unpredictable income and specific risks faced by gig workers. These microinsurance plans provide flexible, cost-effective protection that bridges the coverage gap for gig economy participants, ensuring accessible risk management without the financial burden of standard policy sizes.

Usage-based Microinsurance

Usage-based microinsurance offers tailored coverage with lower policy sizes compared to traditional insurance, optimizing premiums based on actual risk exposure and usage patterns. This approach increases affordability and accessibility for low-income individuals while maintaining essential protection through real-time data and telematics technology.

On-demand Policy Sizing

On-demand insurance offers flexible, policy-sized coverage tailored to individual needs, typically featuring customizable limits and premiums that adjust in real-time, whereas microinsurance provides low-cost, basic protection with fixed, small coverage amounts designed for low-income populations. The scalable nature of on-demand policies allows precise risk management and affordability across diverse assets, contrasting with microinsurance's standardized, minimal coverage that addresses limited, specific risks.

Pay-as-you-go Insurance

Pay-as-you-go insurance offers flexible premium payments based on actual usage, making it ideal for low-income individuals who require smaller policy sizes compared to traditional insurance. Microinsurance typically provides limited coverage with minimal premiums tailored for underserved populations, whereas pay-as-you-go models optimize affordability and accessibility by aligning costs directly with the insured's risk exposure and consumption.

Instant Claim Microinsurance

Instant Claim Microinsurance offers ultra-small policy sizes tailored for low-income individuals, providing immediate coverage and swift claim processing compared to traditional insurance policies that typically involve higher premiums and longer claim settlement times. This microinsurance model enhances accessibility and financial inclusion by delivering affordable, on-demand protection with digital instant claim disbursal mechanisms.

Subscription-based Micro Policies

Subscription-based microinsurance policies offer affordable, flexible coverage tailored to low-income individuals with smaller policy sizes, typically providing protection for specific risks or short durations. Traditional insurance policies generally involve larger premiums and comprehensive coverage, targeting higher-income clients with broader risk management needs.

Insurance vs Microinsurance for policy size. Infographic