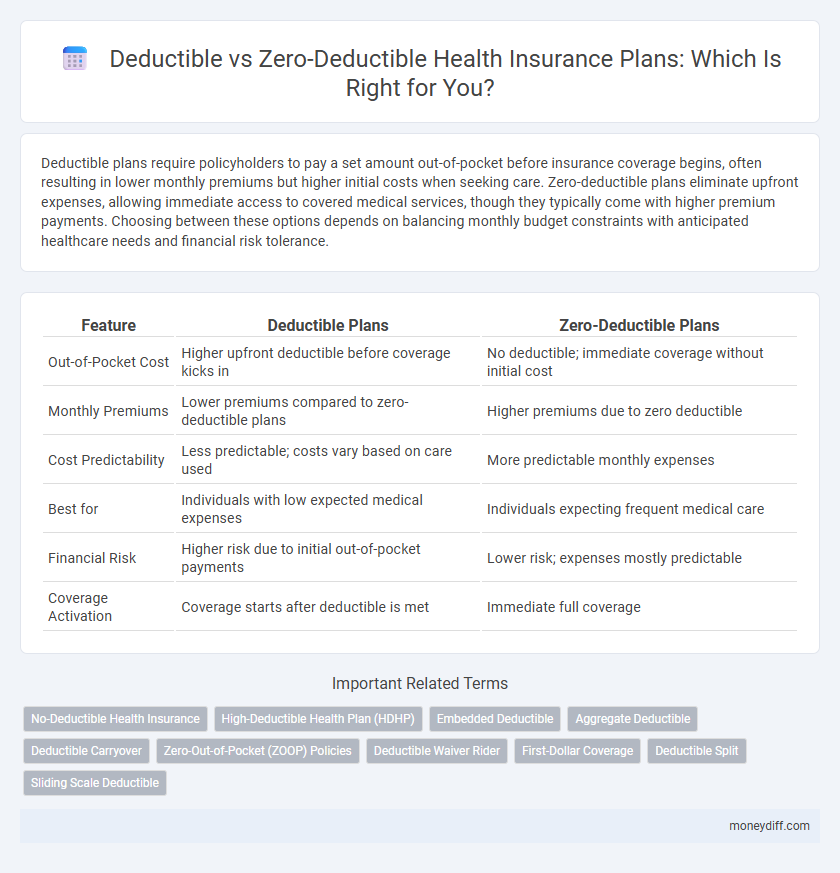

Deductible plans require policyholders to pay a set amount out-of-pocket before insurance coverage begins, often resulting in lower monthly premiums but higher initial costs when seeking care. Zero-deductible plans eliminate upfront expenses, allowing immediate access to covered medical services, though they typically come with higher premium payments. Choosing between these options depends on balancing monthly budget constraints with anticipated healthcare needs and financial risk tolerance.

Table of Comparison

| Feature | Deductible Plans | Zero-Deductible Plans |

|---|---|---|

| Out-of-Pocket Cost | Higher upfront deductible before coverage kicks in | No deductible; immediate coverage without initial cost |

| Monthly Premiums | Lower premiums compared to zero-deductible plans | Higher premiums due to zero deductible |

| Cost Predictability | Less predictable; costs vary based on care used | More predictable monthly expenses |

| Best for | Individuals with low expected medical expenses | Individuals expecting frequent medical care |

| Financial Risk | Higher risk due to initial out-of-pocket payments | Lower risk; expenses mostly predictable |

| Coverage Activation | Coverage starts after deductible is met | Immediate full coverage |

Understanding Deductible and Zero-Deductible Health Plans

Deductible health plans require policyholders to pay a set amount out-of-pocket before insurance coverage begins, often resulting in lower premiums but higher upfront costs. Zero-deductible health plans eliminate this initial payment, providing immediate coverage for medical expenses but typically come with higher monthly premiums. Choosing between these plans depends on an individual's healthcare usage, financial situation, and risk tolerance for out-of-pocket expenses.

Key Differences Between Deductible and Zero-Deductible Plans

Deductible plans require policyholders to pay a specified amount out-of-pocket before insurance coverage begins, which often results in lower monthly premiums but higher initial costs when receiving care. Zero-deductible plans eliminate this upfront cost, providing immediate coverage for medical expenses but typically with higher monthly premiums. The choice between these plans hinges on balancing upfront costs against ongoing premium expenses and anticipated healthcare needs.

How Deductibles Impact Out-of-Pocket Expenses

Deductible plans require policyholders to pay a fixed amount out-of-pocket before insurance coverage begins, directly increasing initial healthcare expenses. Zero-deductible plans eliminate this upfront cost, leading to higher premiums but lower out-of-pocket spending during medical treatments. Understanding the balance between deductible amounts and premium costs is crucial for managing overall healthcare affordability.

Premium Costs: Deductible vs Zero-Deductible Health Insurance

Deductible health insurance plans often feature lower premium costs compared to zero-deductible plans, making them more affordable upfront for policyholders. Zero-deductible plans typically have higher premiums as they cover medical expenses from the first dollar without requiring out-of-pocket spending before benefits apply. Choosing between deductible and zero-deductible health insurance depends on balancing monthly premium affordability against potential out-of-pocket costs during healthcare usage.

Financial Benefits of Deductible Health Plans

Deductible health plans typically offer lower monthly premiums, making them financially advantageous for individuals seeking cost savings upfront. These plans encourage responsible healthcare usage by requiring policyholders to pay a predetermined amount before insurance coverage begins, potentially reducing unnecessary medical expenses. Over time, the combination of lower premiums and controlled healthcare spending can result in significant out-of-pocket savings for policyholders compared to zero-deductible plans.

Advantages of Zero-Deductible Health Policies

Zero-deductible health policies offer immediate coverage by eliminating upfront out-of-pocket costs, ensuring policyholders receive medical care without delay. These plans enhance financial predictability by providing consistent monthly premiums and reducing unexpected expenses during healthcare visits. They are particularly advantageous for individuals with frequent medical needs or chronic conditions requiring regular treatments.

Suitability: Which Plan Matches Your Financial Situation?

Deductible plans suit individuals with stable finances who prefer lower monthly premiums and can cover out-of-pocket costs before insurance kicks in, making them ideal for those expecting fewer medical expenses. Zero-deductible plans benefit people seeking predictable healthcare costs and frequent medical care, as higher premiums offset immediate out-of-pocket spending. Assessing your financial stability and healthcare usage helps determine which plan aligns with your budget and risk tolerance.

Common Misconceptions About Deductibles in Health Insurance

Many policyholders mistakenly believe that zero-deductible plans always offer the best value, but these often come with higher monthly premiums compared to deductible plans, which can be more cost-effective for individuals who require minimal medical care. Another common misconception is that deductible amounts apply to all services uniformly, whereas certain preventive care services may be exempt from the deductible under most health insurance policies. It is also widely misunderstood that meeting a deductible means all remaining costs are fully covered, while in reality, co-pays and co-insurance may still apply, influencing the total out-of-pocket expenses.

Tips for Choosing Between Deductible and Zero-Deductible Plans

Evaluate your annual healthcare usage and financial stability when choosing between deductible and zero-deductible health plans to ensure optimal cost-efficiency. Deductible plans typically have lower premiums but require out-of-pocket expenses before coverage begins, while zero-deductible plans offer immediate coverage with higher premiums. Analyze your medical needs, budget constraints, and risk tolerance to select a plan that balances premium costs with potential out-of-pocket expenses effectively.

Making a Smart Money Management Choice in Health Insurance

Choosing between deductible plans and zero-deductible plans hinges on balancing upfront costs with out-of-pocket expenses to optimize health insurance affordability. Deductible plans usually offer lower monthly premiums but require paying a set amount before coverage kicks in, which benefits those with infrequent medical needs and strong emergency savings. Zero-deductible plans eliminate initial out-of-pocket payments, making them ideal for individuals seeking predictable healthcare costs despite higher premium rates.

Related Important Terms

No-Deductible Health Insurance

No-deductible health insurance plans eliminate upfront out-of-pocket costs, providing immediate coverage for medical expenses and reducing financial barriers to care. These plans often feature higher monthly premiums but lower unexpected expenses, making them ideal for individuals seeking predictable healthcare costs and frequent medical services.

High-Deductible Health Plan (HDHP)

High-Deductible Health Plans (HDHPs) require policyholders to pay higher out-of-pocket costs before insurance coverage begins, typically featuring deductibles exceeding $1,400 for individuals and $2,800 for families in 2024. These plans often integrate with Health Savings Accounts (HSAs), allowing tax-advantaged savings to cover medical expenses, contrasting with zero-deductible plans that offer immediate coverage but usually come with higher premiums.

Embedded Deductible

Embedded deductible plans in health insurance require individual family members to pay a set deductible before coverage applies, while the total family out-of-pocket deductible caps the overall spending, offering more predictable costs compared to zero-deductible plans. Zero-deductible plans eliminate upfront costs but generally come with higher premiums and limited provider networks, impacting long-term affordability and access.

Aggregate Deductible

Aggregate deductible plans require insured individuals to pay a fixed amount out-of-pocket before insurance covers all subsequent medical expenses within a policy period, providing predictable cost management. Zero-deductible plans eliminate initial out-of-pocket costs, offering immediate coverage but often come with higher premiums, making aggregate deductible options cost-effective for those expecting multiple or high medical costs.

Deductible Carryover

Deductible carryover allows insured individuals with deductible health plans to apply a portion of their out-of-pocket expenses from one year toward the deductible of the following year, effectively reducing future financial burden and enhancing cost predictability. Zero-deductible plans eliminate initial out-of-pocket payments but typically come with higher premiums, limiting the benefit of deductible carryover and potentially increasing overall healthcare costs.

Zero-Out-of-Pocket (ZOOP) Policies

Zero-Out-of-Pocket (ZOOP) health insurance policies eliminate deductibles, copayments, and coinsurance, ensuring insured individuals pay no expenses when accessing medical care. These plans provide maximum financial protection and predictability, making them ideal for those seeking comprehensive coverage without unexpected out-of-pocket costs.

Deductible Waiver Rider

Deductible waiver riders in deductible health insurance plans alleviate out-of-pocket expenses by waiving the deductible under specific conditions, providing policyholders with enhanced financial protection during hospitalizations or critical treatments. Zero-deductible plans eliminate upfront costs entirely but often come with higher premiums, making deductible waiver riders a cost-effective alternative for reducing initial medical expenses while maintaining lower monthly insurance payments.

First-Dollar Coverage

Zero-deductible health insurance plans offer first-dollar coverage, meaning policyholders pay no out-of-pocket costs before insurance starts covering medical expenses, providing immediate financial protection. In contrast, deductible plans require members to meet a set amount in medical costs annually before benefits apply, resulting in higher initial out-of-pocket expenses but often lower premium payments.

Deductible Split

Deductible plans require policyholders to pay a set amount out-of-pocket before insurance coverage begins, often resulting in lower monthly premiums, while zero-deductible plans eliminate this upfront cost but generally have higher premium rates. Splitting deductibles into categories like individual and family components allows tailored cost-sharing, enhancing affordability and flexibility in health insurance policies.

Sliding Scale Deductible

Sliding scale deductibles in health insurance adjust the amount a policyholder pays out-of-pocket based on factors such as income or medical usage, offering a customizable alternative to fixed deductible plans. This approach balances premium costs and out-of-pocket expenses, making healthcare more accessible while maintaining cost control for insurers.

Deductible Plans vs Zero-Deductible Plans for health policies. Infographic