Traditional long-term care insurance provides coverage exclusively for extended care services but often comes with higher premiums and strict underwriting requirements. Hybrid life-long-term care policies combine life insurance or annuities with long-term care benefits, offering more flexibility and a death benefit if care is not used. Choosing between these options depends on budget, coverage preferences, and the desire for legacy planning.

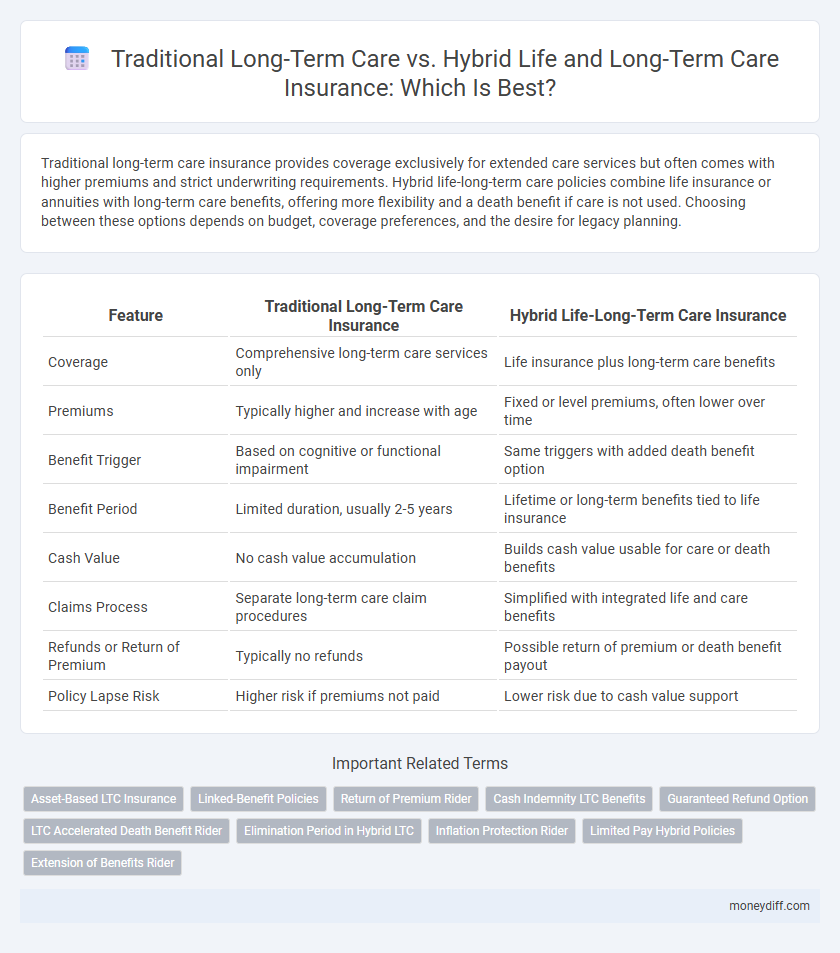

Table of Comparison

| Feature | Traditional Long-Term Care Insurance | Hybrid Life-Long-Term Care Insurance |

|---|---|---|

| Coverage | Comprehensive long-term care services only | Life insurance plus long-term care benefits |

| Premiums | Typically higher and increase with age | Fixed or level premiums, often lower over time |

| Benefit Trigger | Based on cognitive or functional impairment | Same triggers with added death benefit option |

| Benefit Period | Limited duration, usually 2-5 years | Lifetime or long-term benefits tied to life insurance |

| Cash Value | No cash value accumulation | Builds cash value usable for care or death benefits |

| Claims Process | Separate long-term care claim procedures | Simplified with integrated life and care benefits |

| Refunds or Return of Premium | Typically no refunds | Possible return of premium or death benefit payout |

| Policy Lapse Risk | Higher risk if premiums not paid | Lower risk due to cash value support |

Understanding Traditional Long-Term Care Insurance

Traditional long-term care insurance provides coverage specifically for services such as nursing home care, assisted living, and home health care, typically requiring individuals to pay premiums separately from their life insurance policies. This type of insurance is designed to protect assets by covering costs that Medicare and standard health insurance usually don't, but it often involves higher premiums that increase with age. Policyholders should carefully evaluate benefit triggers, elimination periods, and inflation protection options to ensure comprehensive coverage tailored to their future care needs.

What Is Hybrid Life-Long-Term Care Insurance?

Hybrid Life-Long-Term Care insurance combines life insurance with long-term care benefits, offering a death benefit if care is not needed and coverage for long-term care expenses if it is. This type of policy provides flexibility by allowing policyholders to use the death benefit for long-term care or pass it on to beneficiaries. Hybrid plans often feature cash value accumulation, tax advantages, and protection against the high costs of extended nursing home or in-home care.

Key Differences Between Traditional and Hybrid Policies

Traditional long-term care insurance offers standalone coverage specifically for extended care services, typically with fixed benefit periods and monthly benefit limits. Hybrid life-long-term care insurance combines life insurance or annuities with long-term care benefits, providing death benefits if care is not needed and more flexible premium structures. Key differences include the integration of life insurance features in hybrid policies, the financial protection for beneficiaries, and the potential for premium stability versus higher initial costs associated with traditional policies.

Costs and Premium Structures Explained

Traditional long-term care insurance typically requires higher upfront premiums and separate payments for extended care services, often leading to unpredictable long-term costs. Hybrid life-long-term care insurance combines life insurance or annuities with long-term care benefits, offering fixed premiums and potential cash value accumulation that can offset future expenses. This hybrid structure provides more stable premium payments and added financial flexibility compared to the escalating costs commonly seen in traditional long-term care policies.

Coverage Flexibility: Traditional vs Hybrid Options

Traditional long-term care insurance typically offers specialized coverage for nursing home, assisted living, and home care services with fixed benefit limits and strict eligibility criteria. Hybrid life-long-term care insurance combines life insurance with long-term care benefits, providing more flexible payout options and the ability to access cash value if long-term care is not needed. Hybrid policies often allow for coverage customization, including inflation protection and varying benefit periods, enhancing flexibility compared to traditional plans.

Benefits Payout: How Each Policy Delivers Value

Traditional long-term care insurance offers comprehensive coverage with daily benefit payouts specifically for long-term care services, providing straightforward claims for nursing home, assisted living, or home care expenses. Hybrid life-long-term care policies combine life insurance or annuities with long-term care benefits, allowing policyholders to access death benefits or cash value if long-term care is not required, enhancing flexibility and value delivery. Both options optimize benefits payout through either dedicated care funding or integrated life insurance value, catering to different financial planning and care needs.

Tax Advantages and Implications

Traditional long-term care insurance premiums may be tax-deductible as medical expenses if they exceed a certain percentage of adjusted gross income, offering potential tax savings. Hybrid life-long-term care policies combine life insurance with long-term care benefits, allowing tax-free withdrawals for qualifying care expenses and providing a death benefit that can pass to heirs. Policyholders should evaluate the tax implications and benefits of each option in relation to their financial goals and care needs.

Suitability: Who Should Consider Each Type?

Traditional long-term care insurance suits individuals who want dedicated coverage solely for extended care services, typically ideal for those with family history of chronic illness and who can afford higher premiums. Hybrid life-long-term care insurance is better suited for individuals seeking dual benefits of life insurance protection combined with long-term care coverage, appealing to those who want to build cash value or leave a legacy while preparing for potential care needs. Suitability depends on financial goals, health status, and preference for either standalone coverage or integrated policy options.

Risk Factors and Financial Security

Traditional long-term care insurance carries higher risk factors due to rising premiums and limited flexibility, which can strain financial security during prolonged care needs. Hybrid life-long-term care policies combine life insurance with long-term care benefits, offering more predictable costs and the potential to recover value if long-term care is not needed. Choosing hybrid solutions mitigates the risk of outliving coverage and enhances financial stability by integrating death benefits with care funding.

Making the Right Choice for Your Money Management Strategy

Traditional long-term care insurance provides dedicated coverage for extended care needs but often comes with higher premiums and separate policy fees. Hybrid life-long-term care insurance combines life insurance benefits with long-term care coverage, offering more flexible financial planning and potential cash value accumulation. Evaluating your risk tolerance, budget, and long-term financial goals is essential to selecting the most efficient and cost-effective insurance strategy for managing future care expenses.

Related Important Terms

Asset-Based LTC Insurance

Asset-based long-term care (LTC) insurance integrates traditional LTC benefits with life insurance or annuity products, offering policyholders a death benefit alongside coverage for chronic care expenses. Hybrid life-long-term care plans provide greater flexibility and potential cash value growth compared to traditional long-term care insurance, which solely focuses on covering long-term care costs without an investment component.

Linked-Benefit Policies

Linked-benefit policies combine life insurance with long-term care benefits, offering policyholders access to funds if care is needed while preserving a death benefit for beneficiaries. Traditional long-term care insurance focuses solely on care expenses without providing death benefits, making linked-benefit policies a flexible option for comprehensive financial planning and risk management.

Return of Premium Rider

The Return of Premium Rider enhances both traditional long-term care and hybrid life-long-term care insurance by reimbursing premiums if long-term care benefits are unused, increasing policyholder value and financial security. Hybrid policies typically bundle this rider, providing a death benefit and long-term care coverage, whereas traditional policies may offer it as an optional add-on.

Cash Indemnity LTC Benefits

Traditional long-term care insurance policies provide cash indemnity benefits that reimburse policyholders for actual care expenses up to set limits, offering direct financial support for custodial care services. Hybrid life-long-term care insurance combines life insurance with LTC benefits, delivering cash indemnity payouts that flexibly cover care costs while ensuring a death benefit, optimizing both protection and cash flow for policyholders.

Guaranteed Refund Option

Traditional long-term care insurance often lacks a guaranteed refund option, meaning policyholders may forfeit premiums if benefits are not utilized, whereas hybrid life-long-term care insurance typically includes a guaranteed return of premiums, offering financial security regardless of claims. This refund feature enhances the value of hybrid policies by combining long-term care coverage with a life insurance or annuity component, ensuring policyholders or their beneficiaries receive a payout.

LTC Accelerated Death Benefit Rider

The LTC Accelerated Death Benefit Rider in traditional long-term care insurance allows policyholders to access a portion of their death benefit to cover qualified long-term care expenses, enhancing financial flexibility. Hybrid life-long-term care policies integrate this rider with life insurance, providing dual benefits of long-term care coverage and a death benefit payout, often resulting in more comprehensive protection and potential cash value accumulation.

Elimination Period in Hybrid LTC

Hybrid Life-Long-Term Care insurance features a significantly shorter elimination period compared to Traditional Long-Term Care policies, allowing policyholders to access benefits sooner after qualifying care needs arise. This accelerated access helps reduce out-of-pocket expenses during the initial phase of care, offering increased financial stability and peace of mind.

Inflation Protection Rider

Traditional long-term care insurance offers an inflation protection rider that typically increases benefits annually by a fixed percentage to keep pace with rising care costs. Hybrid life-long-term care policies integrate inflation protection directly into the premium structure, often providing more predictable and stable coverage increases over time.

Limited Pay Hybrid Policies

Limited pay hybrid life-long-term care insurance policies combine permanent life insurance coverage with long-term care benefits, offering policyholders a cost-effective solution that builds cash value while protecting against nursing home or assisted living expenses. These policies require a finite number of premium payments, reducing the financial burden compared to traditional long-term care insurance's ongoing premiums and minimizing the risk of coverage lapses due to non-payment.

Extension of Benefits Rider

Extension of Benefits Rider in traditional long-term care insurance provides continued coverage beyond the policy limits, ensuring extended financial protection for chronic care needs. Hybrid life-long-term care policies integrate life insurance with long-term care benefits, offering a more flexible Extension of Benefits Rider that can convert unused benefits into a death benefit or cash value, enhancing overall policy value.

Traditional Long-Term Care vs Hybrid Life-Long-Term Care for insurance. Infographic