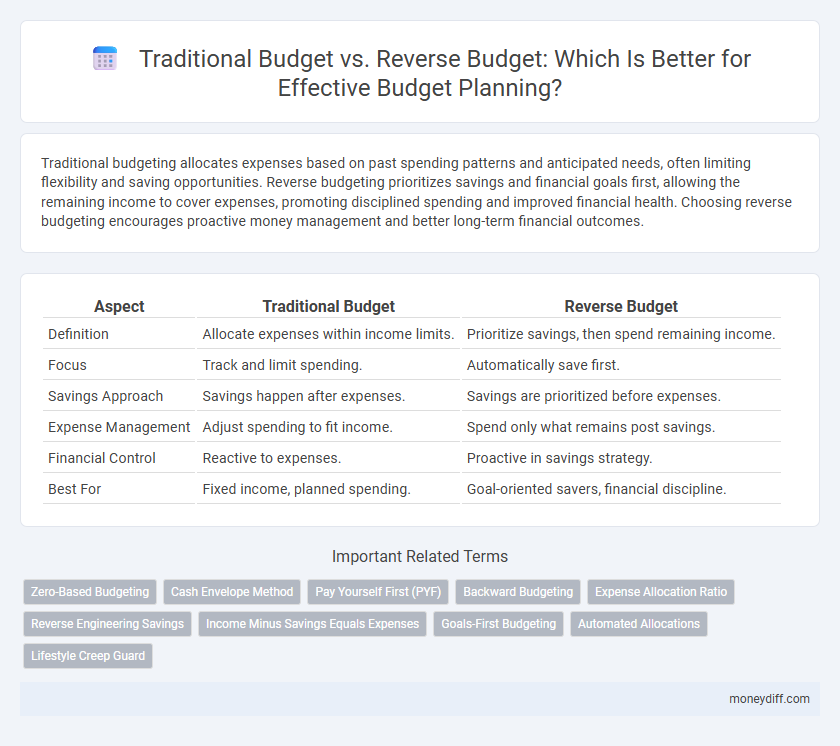

Traditional budgeting allocates expenses based on past spending patterns and anticipated needs, often limiting flexibility and saving opportunities. Reverse budgeting prioritizes savings and financial goals first, allowing the remaining income to cover expenses, promoting disciplined spending and improved financial health. Choosing reverse budgeting encourages proactive money management and better long-term financial outcomes.

Table of Comparison

| Aspect | Traditional Budget | Reverse Budget |

|---|---|---|

| Definition | Allocate expenses within income limits. | Prioritize savings, then spend remaining income. |

| Focus | Track and limit spending. | Automatically save first. |

| Savings Approach | Savings happen after expenses. | Savings are prioritized before expenses. |

| Expense Management | Adjust spending to fit income. | Spend only what remains post savings. |

| Financial Control | Reactive to expenses. | Proactive in savings strategy. |

| Best For | Fixed income, planned spending. | Goal-oriented savers, financial discipline. |

Introduction to Budgeting Methods

Traditional budgeting allocates income to fixed expenses, savings, and discretionary spending in a sequential manner, often leading to rigid financial plans. Reverse budgeting prioritizes savings and investment goals first, then assigns the remaining income to expenses, promoting financial discipline and wealth accumulation. Choosing between these methods depends on individual financial goals and spending behavior to optimize money management.

What is a Traditional Budget?

A Traditional Budget is a financial plan that allocates income to specific expenses, savings, and debt repayment based on historical spending patterns. It involves setting fixed amounts for categories such as housing, groceries, and entertainment before tracking actual expenditures. This method emphasizes controlling costs by comparing planned versus actual spending to maintain financial discipline.

Defining Reverse Budgeting

Reverse budgeting flips the conventional budgeting approach by prioritizing savings and investments before allocating funds for expenses, ensuring financial goals are met systematically. This method begins with setting a savings target, then adjusts spending categories accordingly to prevent overspending. By emphasizing financial discipline and proactive planning, reverse budgeting enhances long-term wealth accumulation compared to traditional budgeting, which typically allocates expenses first.

Key Differences Between Traditional and Reverse Budgets

Traditional budgets allocate income across fixed expense categories based on historical spending patterns, emphasizing expense control and short-term financial goals. Reverse budgets prioritize savings and investments first by setting aside a predetermined percentage of income before allocating funds to expenses, fostering disciplined financial growth and long-term wealth accumulation. Key differences include the sequence of allocation, focus on savings, and adaptability to changing financial priorities.

Pros and Cons of Traditional Budgeting

Traditional budgeting offers a structured approach by allocating funds based on historical spending patterns, providing predictability and control over expenses. However, it often lacks flexibility, potentially leading to inefficient resource allocation and difficulty adapting to unexpected financial changes. This method may encourage rigid adherence to set limits rather than focusing on strategic priorities and innovation.

Advantages and Drawbacks of Reverse Budgeting

Reverse budgeting prioritizes allocating funds to savings and essential expenses before discretionary spending, promoting disciplined financial management and improved savings rates. It enables clearer financial goals by focusing on fixed commitments first but may reduce flexibility for spontaneous purchases or unexpected costs. The method can be challenging for those with irregular incomes yet encourages prioritization that aligns spending with long-term objectives.

Which Method Suits Different Financial Goals

Traditional budget planning allocates income to fixed expense categories first, making it ideal for individuals with steady, predictable expenses and a focus on controlling spending. Reverse budgeting prioritizes savings and financial goals by setting aside desired savings amounts before expenses, suiting those aiming for aggressive wealth building or debt reduction. Choosing between these methods depends on whether managing daily expenses or maximizing savings aligns better with personal financial objectives.

Common Mistakes in Budget Planning

Common mistakes in budget planning include underestimating expenses and prioritizing discretionary spending over essential savings, which traditional budgeting often overlooks. Reverse budgeting avoids these pitfalls by allocating savings and fixed costs first, ensuring financial goals are met before discretionary funds are assigned. Ignoring this approach can lead to overspending and insufficient emergency funds, undermining overall financial stability.

How to Transition from Traditional to Reverse Budget

Transitioning from a traditional budget, which allocates expenses based on projected income, to a reverse budget starts by prioritizing savings and essential costs first, then adjusting discretionary spending with remaining funds. Tracking all income and expenditures using financial apps or spreadsheets ensures transparency and helps identify areas to reduce spending. Consistently reviewing and adjusting the budget monthly reinforces the new saving-focused mindset and promotes financial discipline.

Choosing the Right Budgeting Strategy for You

Choosing the right budgeting strategy depends on personal financial goals and spending habits, where traditional budgeting allocates income across categories before expenses, focusing on disciplined control. Reverse budgeting prioritizes savings first by setting aside a fixed amount, then managing remaining funds for expenses, promoting automated savings growth. Evaluating your cash flow consistency and saving priorities can guide whether a structured traditional or flexible reverse budget better supports your financial planning.

Related Important Terms

Zero-Based Budgeting

Traditional budgeting allocates resources based on historical expenses, often leading to inefficiencies, while reverse budgeting, particularly zero-based budgeting, requires justifying every expense from a zero base, ensuring optimal allocation of funds and eliminating unnecessary costs. Zero-based budgeting enhances financial discipline by prioritizing needs and aligning expenditures with strategic goals, improving overall budget effectiveness in planning processes.

Cash Envelope Method

The Traditional Budget allocates income to fixed expense categories first, often limiting savings and discretionary spending flexibility, while the Reverse Budget prioritizes saving and investing before expenses, encouraging financial discipline. The Cash Envelope Method complements the Reverse Budget by physically dividing cash into labeled envelopes for specific spending categories, enhancing control over cash flow and minimizing overspending.

Pay Yourself First (PYF)

Traditional budgeting prioritizes expenses before savings, often resulting in inconsistent contributions to savings goals, whereas reverse budgeting emphasizes the Pay Yourself First (PYF) principle by securing savings before allocating funds to other expenses. This approach ensures disciplined financial planning and enhances long-term wealth accumulation by treating savings as a non-negotiable priority.

Backward Budgeting

Backward budgeting prioritizes expenses by first allocating funds to savings and financial goals before addressing discretionary spending, contrasting with traditional budgeting which allocates income starting with expenses. This method ensures disciplined saving habits and aligns spending with long-term priorities, enhancing financial stability and goal achievement.

Expense Allocation Ratio

Traditional budget allocates expenses by estimating income first, typically dedicating around 50-60% to fixed costs, 20-30% to variable costs, and 10-20% to savings and discretionary spending. Reverse budget prioritizes savings by setting a fixed savings ratio of 20-30% of income before distributing the remaining funds across fixed and variable expenses, ensuring financial goals are met more effectively.

Reverse Engineering Savings

Reverse budgeting prioritizes saving first by allocating funds to savings before expenses, ensuring financial goals are met consistently. Traditional budgeting tracks spending then saves what remains, often resulting in less effective saving strategies compared to reverse engineering savings.

Income Minus Savings Equals Expenses

Traditional budgeting starts with defining expenses and subtracting savings from the remaining income, often leading to inconsistent saving habits. Reverse budgeting prioritizes savings by deducting a fixed amount from income first, ensuring disciplined saving before allocating funds for expenses.

Goals-First Budgeting

Goals-first budgeting prioritizes financial objectives by allocating resources based on desired outcomes rather than historical spending patterns found in traditional budgeting methods. Reverse budgeting enhances financial discipline by systematically assigning funds to savings and goals before covering expenses, ensuring alignment with long-term priorities.

Automated Allocations

Traditional budget planning allocates funds by estimating expenses first, often leading to inefficiencies and manual adjustments, whereas reverse budgeting prioritizes automated allocations by setting savings and investment goals upfront, enabling dynamic distribution of remaining income. Automated allocations in reverse budgeting streamline financial management through algorithm-driven adjustments, optimizing cash flow and ensuring consistent achievement of financial targets.

Lifestyle Creep Guard

Traditional budgets allocate expenses based on past spending patterns, often enabling lifestyle creep by increasing discretionary spending as income grows. Reverse budgeting prioritizes savings and essential expenses first, effectively guarding against lifestyle creep by limiting discretionary spending to what remains.

Traditional Budget vs Reverse Budget for planning. Infographic