The 50/30/20 budget allocates 50% of income to needs, 30% to wants, and 20% to savings, providing a balanced approach to financial management. In contrast, the 70/10/10/10 budget emphasizes a larger portion toward essentials with 70% for needs, while dividing the remaining 30% equally among wants, savings, and debt repayment or investments. Choosing between these methods depends on individual financial goals, income stability, and priorities for debt reduction or wealth building.

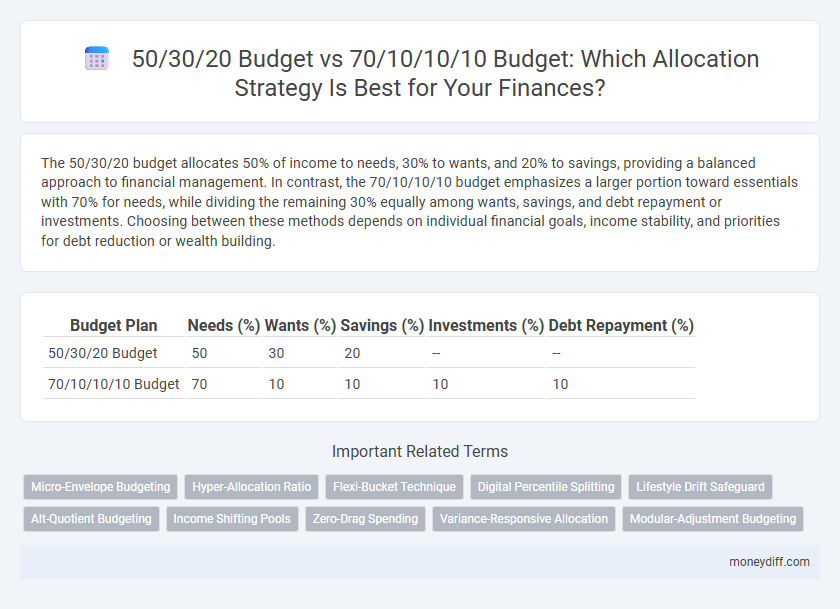

Table of Comparison

| Budget Plan | Needs (%) | Wants (%) | Savings (%) | Investments (%) | Debt Repayment (%) |

|---|---|---|---|---|---|

| 50/30/20 Budget | 50 | 30 | 20 | -- | -- |

| 70/10/10/10 Budget | 70 | 10 | 10 | 10 | 10 |

Understanding the 50/30/20 Budget Rule

The 50/30/20 Budget Rule allocates 50% of income to necessities, 30% to discretionary spending, and 20% to savings or debt repayment, offering a balanced approach to personal finance management. Compared to the 70/10/10/10 Budget, which divides income into 70% needs, 10% wants, 10% savings, and 10% investments or debt, the 50/30/20 method provides greater flexibility in discretionary spending while maintaining strong savings discipline. This rule is optimal for individuals seeking a straightforward framework that promotes financial stability and responsible spending habits.

What Is the 70/10/10/10 Budget Method?

The 70/10/10/10 budget method allocates 70% of income to needs, 10% to savings, 10% to investments, and 10% to discretionary spending, offering a balanced approach to financial management. Unlike the 50/30/20 budget, which divides finances into needs (50%), wants (30%), and savings/debt repayment (20%), the 70/10/10/10 method emphasizes higher essential expenses while ensuring equal focus on saving, investing, and leisure. This structure suits individuals with fixed high living costs aiming for disciplined savings and investment growth.

Core Differences Between 50/30/20 and 70/10/10/10 Budgets

The 50/30/20 budget allocates 50% of income to needs, 30% to wants, and 20% to savings or debt repayment, promoting balanced financial discipline and flexibility. In contrast, the 70/10/10/10 budget distributes 70% for essentials, 10% for wants, 10% for savings, and 10% for debt or investments, emphasizing stricter control on discretionary spending and enhanced focus on financial growth. Core differences lie in the allocation emphasis, with 50/30/20 offering broader spending freedom and 70/10/10/10 prioritizing aggressive savings and reduced lifestyle inflation.

Allocating Your Income: Needs vs. Wants

The 50/30/20 budget plan allocates 50% of income to needs, 30% to wants, and 20% to savings or debt repayment, emphasizing balance between essentials and discretionary spending. In contrast, the 70/10/10/10 budget divides income into 70% for needs, 10% for wants, 10% for savings, and 10% for debt or investments, prioritizing a higher share for essential expenses. Choosing between these models depends on individual financial goals, with the 50/30/20 approach offering more flexibility for discretionary spending and the 70/10/10/10 allowing stricter control over wants and increased focus on savings.

Flexibility and Simplicity: Which Budget Suits Beginners?

The 50/30/20 budget offers simplicity and flexibility by dividing income into essentials, wants, and savings, making it ideal for beginners seeking straightforward financial management. The 70/10/10/10 budget allocates funds more granularly toward essentials, savings, debt, and personal goals, which can provide better control but may overwhelm those new to budgeting. Beginners typically benefit from the 50/30/20 approach due to its ease of implementation and adaptability to changing financial situations.

Saving and Investing: How Do They Compare?

The 50/30/20 budget allocates 20% of income towards saving and investing, whereas the 70/10/10/10 budget dedicates only 10%, emphasizing a more aggressive approach to discretionary spending. With the 50/30/20 method, higher savings and investments can accelerate wealth building and financial security. Conversely, the 70/10/10/10 budget may limit long-term growth potential due to reduced funds allocated for savings and investments.

Debt Repayment Strategies in Each Budget Model

In the 50/30/20 budget model, allocating 20% of income toward debt repayment ensures a balanced approach between essentials, discretionary spending, and debt reduction, promoting steady progress toward financial freedom. Conversely, the 70/10/10/10 budget allocates only 10% to debt repayment, prioritizing necessities with 70% of income, which may prolong the debt payoff period but can be effective for those managing high living costs. Tailoring debt repayment strategies in each model depends on individual financial goals, income stability, and the urgency of reducing liabilities.

Long-Term Financial Goals and Planning

The 50/30/20 budget allocation prioritizes essential expenses, flexible spending, and savings, promoting balanced short-term and long-term financial goals through manageable savings and debt repayment. In contrast, the 70/10/10/10 budget allocates a larger portion to necessities but dedicates equal smaller percentages to savings, investments, and debt reduction, potentially accelerating long-term wealth accumulation with disciplined financial planning. Both methods support long-term financial goals but differ in saving intensity and spending flexibility, impacting overall financial growth and security.

Pros and Cons of 50/30/20 vs. 70/10/10/10

The 50/30/20 budget allocates 50% to needs, 30% to wants, and 20% to savings, offering simplicity and balanced flexibility for most financial situations. In contrast, the 70/10/10/10 budget divides income into 70% for essentials, and 10% each for savings, investments, and leisure, promoting aggressive saving and investment habits but requiring stricter spending discipline. The 50/30/20 is easier to maintain but may underemphasize investment potential, while the 70/10/10/10 maximizes wealth growth but can limit discretionary spending freedom.

Choosing the Best Budgeting Method for Your Lifestyle

The 50/30/20 budget allocates 50% of income to needs, 30% to wants, and 20% to savings, offering a balanced approach for most lifestyles. In contrast, the 70/10/10/10 budget focuses 70% on essentials, with equal 10% splits for wants, savings, and debt repayment, ideal for aggressive debt management and disciplined savers. Selecting the best budgeting method depends on your financial goals, spending habits, and flexibility required for daily expenses.

Related Important Terms

Micro-Envelope Budgeting

The 50/30/20 budget divides income into essential expenses, lifestyle choices, and savings, whereas the 70/10/10/10 budget applies Micro-Envelope Budgeting by allocating funds into more precise categories such as needs, savings, investments, and discretionary spending. Micro-Envelope Budgeting enhances financial control and accountability by segmenting money into specific, purpose-driven envelopes, reducing overspending through detailed allocation.

Hyper-Allocation Ratio

The 50/30/20 budget allocates 50% to needs, 30% to wants, and 20% to savings, promoting balanced financial health with moderate hyper-allocation. In contrast, the 70/10/10/10 budget emphasizes a hyper-allocation ratio by dedicating 70% to primary expenses and splitting the remaining 30% evenly among savings, investments, and discretionary spending, intensifying focus on essential costs.

Flexi-Bucket Technique

The 50/30/20 budget allocates 50% to needs, 30% to wants, and 20% to savings, offering a straightforward framework, while the 70/10/10/10 budget divides income into 70% essentials, 10% savings, 10% investments, and 10% discretionary spending, providing more granular control. The Flexi-Bucket Technique enhances both models by allowing dynamic reallocation within categories, optimizing financial flexibility and adaptability based on real-time expenses and goals.

Digital Percentile Splitting

The 50/30/20 budget allocates 50% to needs, 30% to wants, and 20% to savings or debt repayment, providing a clear percentage split ideal for digital expense tracking and percentile analysis. In contrast, the 70/10/10/10 budget divides income into 70% essentials, 10% savings, 10% investments, and 10% leisure, offering a more granular digital percentile splitting that enhances financial precision and control over digital spending categories.

Lifestyle Drift Safeguard

The 50/30/20 budget allocates 50% to needs, 30% to wants, and 20% to savings, providing a balanced approach that minimizes lifestyle drift by ensuring consistent savings. In contrast, the 70/10/10/10 budget dedicates 70% to essentials, with smaller percentages for wants, savings, and debt repayment, offering a stricter safeguard against lifestyle inflation by prioritizing essential expenses and financial obligations.

Alt-Quotient Budgeting

Alt-Quotient Budgeting refines traditional methods by emphasizing flexible allocation, contrasting the 50/30/20 rule which designates fixed percentages for needs, wants, and savings, with the 70/10/10/10 model that diversifies spending into essential expenses, leisure, savings, and investments. By dynamically adjusting proportions based on financial goals and personal priorities, Alt-Quotient Budgeting offers a tailored framework that enhances financial efficiency and long-term wealth accumulation.

Income Shifting Pools

The 50/30/20 budget allocates 50% of income to needs, 30% to wants, and 20% to savings or debt repayment, optimizing financial flexibility by balancing essential and discretionary expenses. In contrast, the 70/10/10/10 budget shifts income into four pools: 70% for necessities, and 10% each for savings, debt repayment, and lifestyle choices, promoting more targeted income distribution towards financial goals.

Zero-Drag Spending

The 50/30/20 budget allocates 50% to needs, 30% to wants, and 20% to savings or debt repayment, promoting flexible spending while maintaining financial discipline. In contrast, the 70/10/10/10 budget divides income into 70% essentials, 10% wants, 10% savings, and 10% investments, optimizing zero-drag spending by minimizing discretionary expenses and maximizing long-term wealth growth.

Variance-Responsive Allocation

The 50/30/20 budget allocates 50% to needs, 30% to wants, and 20% to savings or debt repayment, providing flexibility for varying financial priorities, while the 70/10/10/10 budget allocates 70% to essentials, with equal 10% portions for savings, investments, and discretionary spending, enhancing responsiveness to changing financial goals. Variance-responsive allocation in the 70/10/10/10 model allows more precise adjustments by narrowing core expenses, increasing savings and investment adaptability compared to the broader categories of the 50/30/20 framework.

Modular-Adjustment Budgeting

The 50/30/20 budget allocates 50% to needs, 30% to wants, and 20% to savings or debt repayment, promoting balanced financial health, while the 70/10/10/10 modular-adjustment budgeting method divides income into more specific categories of essentials, discretionary spending, savings, and investments, offering greater flexibility and precision for dynamic financial goals. Modular-adjustment budgeting facilitates personalized recalibration of each module, allowing individuals to adapt allocations based on changing circumstances without disrupting the overall budget structure.

50/30/20 Budget vs 70/10/10/10 Budget for allocation. Infographic