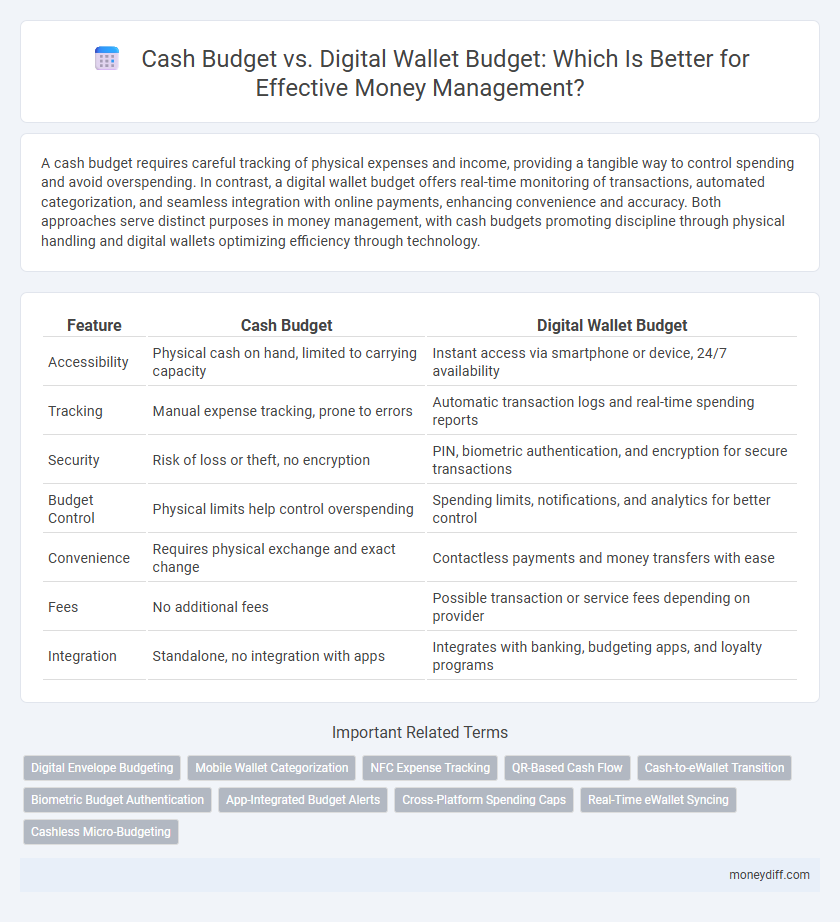

A cash budget requires careful tracking of physical expenses and income, providing a tangible way to control spending and avoid overspending. In contrast, a digital wallet budget offers real-time monitoring of transactions, automated categorization, and seamless integration with online payments, enhancing convenience and accuracy. Both approaches serve distinct purposes in money management, with cash budgets promoting discipline through physical handling and digital wallets optimizing efficiency through technology.

Table of Comparison

| Feature | Cash Budget | Digital Wallet Budget |

|---|---|---|

| Accessibility | Physical cash on hand, limited to carrying capacity | Instant access via smartphone or device, 24/7 availability |

| Tracking | Manual expense tracking, prone to errors | Automatic transaction logs and real-time spending reports |

| Security | Risk of loss or theft, no encryption | PIN, biometric authentication, and encryption for secure transactions |

| Budget Control | Physical limits help control overspending | Spending limits, notifications, and analytics for better control |

| Convenience | Requires physical exchange and exact change | Contactless payments and money transfers with ease |

| Fees | No additional fees | Possible transaction or service fees depending on provider |

| Integration | Standalone, no integration with apps | Integrates with banking, budgeting apps, and loyalty programs |

Introduction to Cash and Digital Wallet Budgets

Cash budgets provide a tangible method for tracking daily expenses and managing physical money, ensuring strict control over cash flow. Digital wallet budgets leverage technology to monitor spending through apps and online platforms, offering real-time updates and integration with multiple payment methods. Both approaches enhance financial discipline but differ in convenience, tracking capabilities, and accessibility for money management.

Key Differences Between Cash Budgets and Digital Wallet Budgets

Cash budgets rely on physical currency tracking to control spending and ensure liquidity, while digital wallet budgets use app-based platforms offering real-time expense monitoring and automated alerts. Cash budgets offer tangible control but lack transaction categorization, whereas digital wallet budgets provide detailed spending analytics and integration with multiple financial services. The key difference lies in accessibility and data insight, with digital wallets enabling seamless, data-driven money management compared to the manual and limited scope of cash budgeting.

Pros and Cons of Cash Budgeting

Cash budgeting enables precise control over spending by limiting expenditures to the physical money available, reducing the risk of debt accumulation. Its tangible nature promotes financial discipline but can be inconvenient due to limited accessibility and inability to track expenses digitally. Unlike digital wallets, cash budgeting lacks automated transaction records and instant fund transfers, making it less efficient for online or emergency payments.

Advantages and Disadvantages of Digital Wallet Budgeting

Digital wallet budgeting offers real-time tracking and instant notifications, enhancing convenience and enabling better control over spending habits. However, it relies heavily on internet access and may pose security risks due to potential cyber threats, unlike cash budgets which offer anonymity and limit overspending through physical constraints. Integrating digital wallets into budgeting can improve financial transparency but requires digital literacy and vigilance against fraudulent activities.

Security Considerations: Cash vs Digital Wallets

Cash budgets offer tangible control over money, reducing risks of digital theft or hacking incidents prevalent in online transactions. Digital wallet budgets provide encryption and biometric authentication, enhancing protection against unauthorized access and fraud. Users must weigh physical security risks of cash, such as loss or theft, against cybersecurity threats inherent in digital wallets when managing their finances.

Expense Tracking: Paper Receipts vs Digital Records

Cash budgets rely heavily on paper receipts for expense tracking, which can lead to misplacement and manual data entry errors. Digital wallet budgets utilize automated digital records that provide real-time expense tracking, enhancing accuracy and ease of access. This shift to electronic documentation significantly streamlines budgeting processes and improves financial oversight.

Accessibility and Convenience in Budgeting Methods

Cash budgets provide tangible control over spending, allowing users to physically allocate money for different expenses, which can enhance discipline but may limit accessibility outside of home. Digital wallet budgets offer seamless access from multiple devices, enabling real-time tracking and adjustments anytime, anywhere, thereby increasing convenience and flexibility for managing finances. The choice between these methods depends on the user's preference for physical cash handling versus digital convenience in budgeting.

Budgeting for Different Personality Types

Cash budgets offer tangible control for individuals who prefer physical money handling and visual spending limits, enhancing discipline for those with impulsive tendencies. Digital wallet budgets provide real-time tracking and customizable alerts, catering to tech-savvy personalities seeking convenience and detailed analytics. Tailoring budget methods to personality types improves financial adherence and reduces overspending risks by aligning with individual behavioral patterns.

Transitioning from Cash to Digital Wallet: Tips and Challenges

Transitioning from a cash budget to a digital wallet budget requires understanding transaction tracking and adapting spending habits to digital interfaces. Challenges include managing digital security risks and ensuring real-time balance monitoring to avoid overspending. Embracing budgeting apps linked to digital wallets can streamline expense categorization and enhance financial control.

Choosing the Right Budget Method for Effective Money Management

Choosing the right budget method is crucial for effective money management, as cash budgets provide tangible control over spending by limiting expenses to available physical cash. Digital wallet budgets offer real-time tracking, automated payment reminders, and integration with financial apps, enabling enhanced convenience and detailed expense monitoring. Selecting the optimal approach depends on personal financial habits, spending patterns, and the need for either strict cash discipline or tech-enabled financial oversight.

Related Important Terms

Digital Envelope Budgeting

Digital envelope budgeting enhances money management by allocating funds into virtual categories within digital wallets, enabling precise tracking and control over spending. Compared to traditional cash budgets, digital wallets offer real-time updates, automated reminders, and seamless integration with financial apps, improving budget adherence and reducing overspending.

Mobile Wallet Categorization

Cash budgets track physical currency flow, emphasizing cash inflows and outflows for precise daily expense control, while digital wallet budgets leverage mobile wallet categorization to automatically sort transactions by categories like groceries, utilities, and entertainment, enhancing real-time spending insights and financial planning efficiency. Mobile wallet apps such as Apple Pay, Google Wallet, and Samsung Pay integrate AI-driven categorization features, enabling users to monitor budget adherence and adjust spending habits dynamically.

NFC Expense Tracking

Cash budgets provide a tangible method for managing expenses but lack real-time tracking and detailed categorization available in digital wallet budgets. Digital wallets with NFC expense tracking enable instant transaction logging, automated spending analysis, and seamless budget adjustments, enhancing precision and control over personal finances.

QR-Based Cash Flow

QR-based cash flow enhances digital wallet budgets by enabling real-time transaction tracking and seamless payments, improving financial accuracy and spending control compared to traditional cash budgets. Integrating QR codes into cash budgets bridges the gap between physical cash handling and digital financial management, streamlining cash flow monitoring and reducing errors.

Cash-to-eWallet Transition

Transitioning from a cash budget to a digital wallet budget enhances real-time expense tracking and reduces cash handling risks, increasing financial accuracy and convenience. Digital wallet budgets leverage automated alerts and spending insights, optimizing money management compared to traditional cash-only methods.

Biometric Budget Authentication

Cash budgets require manual tracking and physical verification, often leading to errors and slower reconciliation, whereas digital wallet budgets leverage biometric budget authentication to secure transactions and enable real-time monitoring. Biometric authentication methods like fingerprint or facial recognition enhance security, reduce fraud risk, and streamline budget adherence in digital wallets compared to traditional cash management.

App-Integrated Budget Alerts

Cash budgets offer tangible control by tracking physical spending, but lack real-time notifications, whereas digital wallet budgets provide app-integrated budget alerts that instantly notify users of spending limits and transaction anomalies. These real-time alerts enhance money management by promoting timely adjustments and preventing overspending, making digital wallets a more efficient tool for maintaining budget discipline.

Cross-Platform Spending Caps

Cash budgets rely on physical limits and tangible tracking methods, while digital wallet budgets enable real-time monitoring and automated spending caps across multiple platforms, enhancing control over expenses. Cross-platform spending caps in digital wallets integrate with various merchant systems and apps, providing seamless enforcement of budget limits that cash methods cannot replicate.

Real-Time eWallet Syncing

Real-time eWallet syncing enables seamless updates between digital wallet budgets and cash budgets, enhancing accurate money management by instantly reflecting transactions across platforms. This synchronization minimizes overspending risks and improves financial tracking by providing up-to-date budget status without manual entry.

Cashless Micro-Budgeting

Cashless micro-budgeting leverages digital wallet budgets to provide real-time tracking, enhanced security, and seamless transaction categorization, enabling precise control over small-scale expenses. Unlike traditional cash budgets, digital wallets reduce cash handling risks and support automated spending limits, optimizing money management for everyday microtransactions.

Cash budget vs Digital wallet budget for money management. Infographic