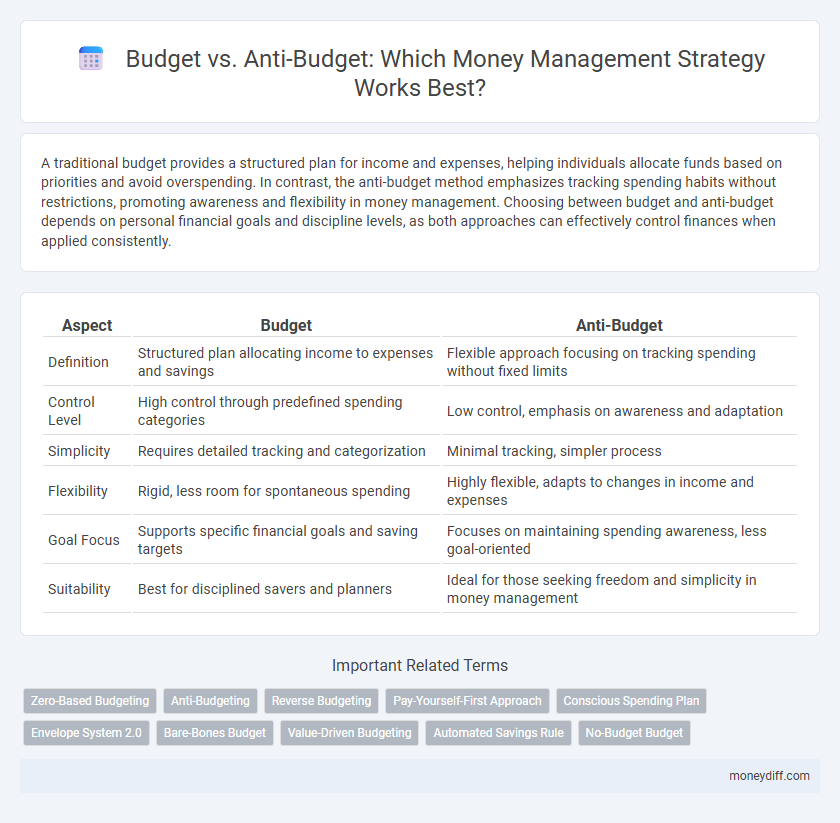

A traditional budget provides a structured plan for income and expenses, helping individuals allocate funds based on priorities and avoid overspending. In contrast, the anti-budget method emphasizes tracking spending habits without restrictions, promoting awareness and flexibility in money management. Choosing between budget and anti-budget depends on personal financial goals and discipline levels, as both approaches can effectively control finances when applied consistently.

Table of Comparison

| Aspect | Budget | Anti-Budget |

|---|---|---|

| Definition | Structured plan allocating income to expenses and savings | Flexible approach focusing on tracking spending without fixed limits |

| Control Level | High control through predefined spending categories | Low control, emphasis on awareness and adaptation |

| Simplicity | Requires detailed tracking and categorization | Minimal tracking, simpler process |

| Flexibility | Rigid, less room for spontaneous spending | Highly flexible, adapts to changes in income and expenses |

| Goal Focus | Supports specific financial goals and saving targets | Focuses on maintaining spending awareness, less goal-oriented |

| Suitability | Best for disciplined savers and planners | Ideal for those seeking freedom and simplicity in money management |

Understanding Budgeting: Traditional Methods Explained

Traditional budgeting involves creating a detailed plan that allocates income to specific expenses, savings, and investments, helping individuals control spending and achieve financial goals. Anti-budget methods, such as the "pay-yourself-first" approach, prioritize saving before allocating funds to expenses, offering greater flexibility and reducing the stress of strict spending limits. Understanding these contrasting money management strategies enables better personal finance decisions tailored to individual habits and financial objectives.

What is Anti-Budgeting? Core Principles

Anti-budgeting centers on tracking cash flow instead of imposing strict spending limits, allowing greater flexibility in managing finances. Core principles include prioritizing savings goals, monitoring expenses without rigid categories, and adjusting spending based on actual income rather than fixed budgets. This approach reduces financial stress by adapting to evolving monetary situations rather than constraining users to predetermined allocations.

Key Differences Between Budget and Anti-Budget

A budget involves detailed planning and allocation of income towards specific expenses, savings, and investments to control spending and achieve financial goals. The anti-budget approach simplifies money management by allowing unrestricted spending within essential categories and directing surplus funds towards savings or debt repayment without rigid tracking. Key differences include the structured, rule-based nature of budgeting versus the flexible, minimalist system of the anti-budget, emphasizing ease and financial awareness over micromanagement.

Pros and Cons of Traditional Budgeting

Traditional budgeting provides a structured framework for tracking income and expenses, helping individuals maintain financial discipline and prepare for future goals. However, it can be rigid and time-consuming, often leading to frustration when unexpected expenses arise or spending limits feel restrictive. Critics argue that traditional budgets may discourage flexibility and adaptability, which are crucial for effective money management in dynamic financial situations.

Advantages and Drawbacks of Anti-Budgeting

Anti-budgeting offers flexibility by allowing individuals to spend freely without rigid categories, fostering a stress-free financial mindset and adaptability to changing expenses. However, this approach can lack structure, making it difficult to track spending patterns or save systematically, potentially leading to overspending and insufficient financial goals achievement. While traditional budgeting emphasizes control and predictability, anti-budgeting prioritizes autonomy but requires strong self-discipline and regular financial review to avoid pitfalls.

Which Method Suits Your Money Personality?

Choosing between a budget and an anti-budget depends on your money personality and spending habits. Traditional budgets work best for those who prefer structured, detailed tracking and set limits to control expenses, while the anti-budget suits individuals who favor freedom and simplicity by focusing on saving first and spending the rest flexibly. Understanding whether you thrive on strict financial discipline or value flexible money management helps determine the most effective approach for your financial goals.

Step-by-Step: How to Start a Traditional Budget

Start a traditional budget by listing all income sources and tracking monthly expenses to gain clear financial visibility. Categorize expenses into fixed, variable, and discretionary to identify spending patterns and areas for adjustment. Allocate specific amounts to each category, setting realistic savings goals to ensure financial discipline and control.

Step-by-Step: Implementing an Anti-Budget Approach

Implementing an anti-budget approach begins with tracking total income and expenses without restrictive categories, allowing for flexible financial management. Prioritize paying essential bills and savings automatically before freely spending the remaining funds, fostering natural money allocation. Regularly review overall spending to ensure alignment with financial goals, promoting conscious yet unrestricted money habits.

Common Pitfalls to Avoid in Both Systems

Common pitfalls in budget and anti-budget systems include failing to track expenses accurately and neglecting to adjust plans based on financial changes. Over-restricting spending in budgets may lead to frustration, while anti-budgets risk overspending without clear limits. Both systems require discipline to monitor cash flow regularly and avoid unplanned debt accumulation.

Choosing the Right Money Management Strategy for You

Selecting the optimal money management strategy depends on individual financial goals and spending habits, with Budgeting offering structured control by allocating specific amounts to categories, while Anti-Budget methods like the 80/20 rule prioritize saving before spending. Budgeting suits those who need detailed tracking and discipline, whereas Anti-Budget appeals to individuals seeking simplicity and flexibility without strict limits. Evaluating personal preferences and lifestyle can guide the choice between rigid budgeting frameworks and more intuitive money management approaches for sustainable financial health.

Related Important Terms

Zero-Based Budgeting

Zero-Based Budgeting (ZBB) allocates every dollar of income to specific expenses, savings, or debt repayment, ensuring no funds are left unassigned and promoting precise financial control. Unlike anti-budgeting methods that avoid strict plans, ZBB drives disciplined money management by justifying all expenditures from a zero base each period.

Anti-Budgeting

The Anti-Budget method emphasizes tracking only total income and savings rather than allocating funds to specific categories, allowing for greater flexibility and reduced stress in money management. This approach promotes automatic saving and discretionary spending, simplifying financial decisions and encouraging personal responsibility without rigid constraints.

Reverse Budgeting

Reverse budgeting prioritizes allocating savings and investments first before assigning funds to expenses, enhancing financial discipline by ensuring goals are met upfront. This approach contrasts with traditional budgeting, which often results in leftover savings rather than planned allocation, positioning reverse budgeting as a more effective strategy for long-term wealth accumulation.

Pay-Yourself-First Approach

The Pay-Yourself-First approach prioritizes allocating a fixed portion of income towards savings and investments before covering expenses, ensuring financial growth and stability. Unlike traditional budgeting that tracks spending after expenses, this method emphasizes proactive wealth building by treating savings as a mandatory expense rather than an optional leftover.

Conscious Spending Plan

A Conscious Spending Plan prioritizes intentional allocation of funds, emphasizing value-driven expenses over strict limits, contrasting with traditional budgets that often impose rigid monetary caps. This approach enhances financial flexibility and mindfulness, promoting sustainable money management by aligning spending with personal goals and priorities.

Envelope System 2.0

The Envelope System 2.0 enhances traditional budgeting by allocating funds into designated digital envelopes, promoting disciplined spending and clear financial boundaries. Unlike anti-budget approaches that emphasize flexibility without strict tracking, this method ensures precise control over expenses, reducing overspending and improving savings consistency.

Bare-Bones Budget

A Bare-Bones Budget prioritizes essential expenses only, eliminating discretionary spending to maximize savings and control cash flow effectively. This strict money management approach contrasts with Anti-Budget strategies, which track income without rigid limits, relying on spending discipline rather than fixed categories.

Value-Driven Budgeting

Value-driven budgeting prioritizes aligning expenses with personal or organizational core values, ensuring money management focuses on maximizing meaningful returns rather than merely tracking every dollar. Unlike traditional anti-budget approaches that avoid constraints, value-driven budgeting creates intentional spending plans that enhance financial discipline while promoting purposeful resource allocation.

Automated Savings Rule

Automated savings rules in budget systems allocate a fixed portion of income to savings accounts, ensuring consistent financial growth and disciplined money management. Anti-budget approaches, in contrast, forgo preset savings allocations, relying on spontaneous or goal-driven saving, which may hinder steady accumulation but offer greater spending flexibility.

No-Budget Budget

The No-Budget Budget approach emphasizes flexible money management by tracking overall spending without rigid category limits, promoting financial awareness without strict constraints. This method contrasts with traditional budgeting by allowing natural spending patterns while still encouraging saving and expense control through continuous monitoring.

Budget vs Anti-Budget for money management. Infographic