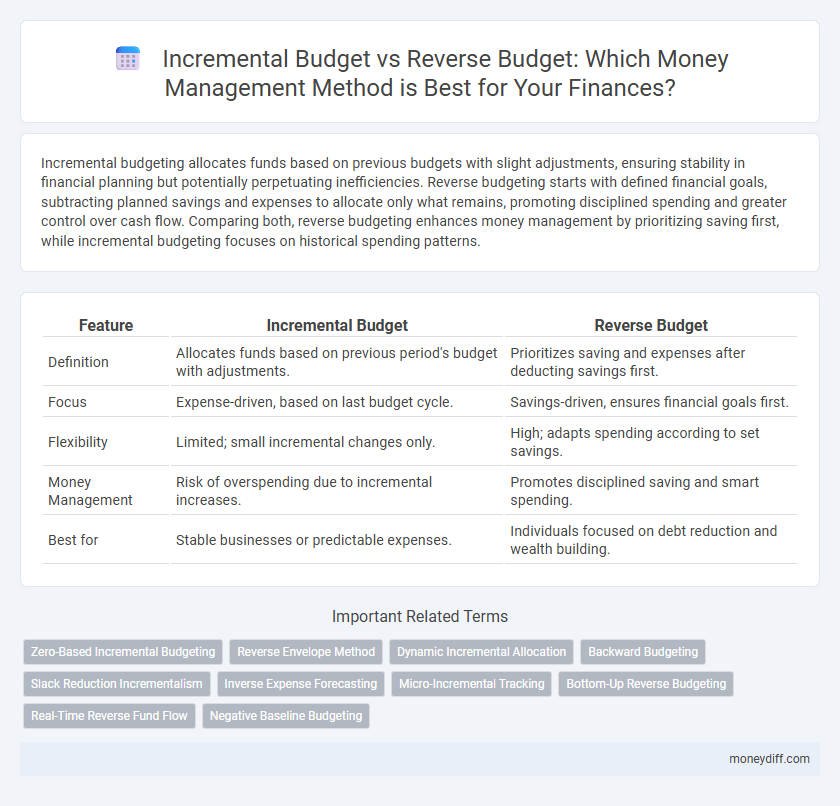

Incremental budgeting allocates funds based on previous budgets with slight adjustments, ensuring stability in financial planning but potentially perpetuating inefficiencies. Reverse budgeting starts with defined financial goals, subtracting planned savings and expenses to allocate only what remains, promoting disciplined spending and greater control over cash flow. Comparing both, reverse budgeting enhances money management by prioritizing saving first, while incremental budgeting focuses on historical spending patterns.

Table of Comparison

| Feature | Incremental Budget | Reverse Budget |

|---|---|---|

| Definition | Allocates funds based on previous period's budget with adjustments. | Prioritizes saving and expenses after deducting savings first. |

| Focus | Expense-driven, based on last budget cycle. | Savings-driven, ensures financial goals first. |

| Flexibility | Limited; small incremental changes only. | High; adapts spending according to set savings. |

| Money Management | Risk of overspending due to incremental increases. | Promotes disciplined saving and smart spending. |

| Best for | Stable businesses or predictable expenses. | Individuals focused on debt reduction and wealth building. |

Understanding Incremental Budgeting in Money Management

Incremental budgeting involves adjusting the previous period's budget by adding or subtracting a specific percentage or amount, making it straightforward for organizations to plan future expenses based on historical data. This method emphasizes consistency, stability, and ease of implementation, allowing managers to allocate resources with minimal disruption. However, it may overlook inefficiencies or changing priorities, unlike reverse budgeting which starts with zero and builds up based on needs.

What Is Reverse Budgeting?

Reverse budgeting is a money management strategy where you prioritize saving and investing before allocating funds to expenses, ensuring financial goals are met first. Unlike incremental budgeting, which starts from expenses and adds savings afterward, reverse budgeting allocates a fixed amount to savings upfront, compelling disciplined spending. This approach promotes consistent saving habits and helps avoid overspending by aligning expenditures with remaining income after savings.

Key Differences Between Incremental and Reverse Budgets

Incremental budgets allocate funds based on the previous period's budget with adjustments for growth or reductions, emphasizing continuity and simplicity in financial planning. Reverse budgets start by setting savings or investment goals first, then allocate remaining funds for expenses, prioritizing financial discipline and goal achievement. Key differences include their approach to fund allocation, with incremental budgets focusing on past expenses and reverse budgets emphasizing future savings targets.

Pros and Cons of Incremental Budgeting

Incremental budgeting simplifies financial planning by adjusting previous budgets with small percentage changes, offering ease of implementation and consistency. However, it can perpetuate inefficiencies, as past expenditures heavily influence future allocations without thorough scrutiny. This approach risks budgetary inertia, limiting strategic resource reallocation and innovation within money management.

Advantages and Disadvantages of Reverse Budgeting

Reverse budgeting prioritizes saving and investing by allocating funds to financial goals before covering expenses, promoting disciplined money management and improved wealth accumulation. This method helps prevent overspending and encourages consistent savings but may be less flexible in handling unexpected costs or fluctuating income. Challenges include the need for strong financial planning skills and potential difficulty adjusting to lifestyle changes compared to traditional incremental budgeting.

Incremental Budgeting: Best Use Cases

Incremental budgeting is ideal for organizations with stable financial environments where previous budgets serve as a reliable baseline for future allocation, ensuring continuity and simplicity in planning. It works best in cases where operational activities and expenses remain consistent year-over-year, allowing minor adjustments based on inflation or policy changes. This method is particularly effective for government agencies, established businesses, and departments with predictable expenditure patterns seeking straightforward budget control.

When to Choose Reverse Budgeting

Choose reverse budgeting when prioritizing savings by allocating funds to investments or emergency funds first, then managing expenses with the remaining income. This method enhances financial discipline by ensuring savings goals are consistently met before discretionary spending occurs. Reverse budgeting is ideal for individuals aiming to build wealth or recover from debt while maintaining strict control over spending habits.

Common Challenges in Both Budgeting Methods

Incremental budget and reverse budget methods both face challenges such as inaccurate expense forecasting, which can lead to resource misallocation and financial strain. Limited flexibility in adjusting to unexpected costs often results in budget overruns or underspending. Both approaches require diligent monitoring and regular adjustments to maintain alignment with financial goals and avoid inefficiencies.

Tips for Transitioning Between Budgeting Styles

Transitioning from an incremental budget to a reverse budget requires a clear understanding of prioritizing savings and essential expenses before discretionary spending. Track all income and fixed costs meticulously to establish accurate baseline figures, then allocate surplus funds towards financial goals or debt reduction first. Regularly review and adjust spending categories to maintain discipline and ensure alignment with your long-term financial objectives.

Choosing the Right Budgeting Method for Your Financial Goals

Incremental budgeting builds upon the previous period's budget by adjusting expenses up or down, ideal for stable financial environments with predictable costs. Reverse budgeting starts with setting savings and investment goals before allocating leftover funds to expenses, promoting disciplined money management and accelerated wealth building. Selecting the right method depends on your financial objectives, with incremental budgeting suited for consistent spending patterns and reverse budgeting favored for aggressive saving strategies.

Related Important Terms

Zero-Based Incremental Budgeting

Zero-based incremental budgeting combines the efficiency of zero-based budgeting by justifying every expense with the simplicity of incremental budgeting, where only changes from the previous budget are evaluated. This hybrid approach ensures precise allocation of resources while minimizing unnecessary expenditures, optimizing overall financial management.

Reverse Envelope Method

The Reverse Envelope Method allocates money by prioritizing savings and essential expenses before discretionary spending, contrasting the Incremental Budget approach that adjusts previous budgets incrementally each period. This strategy enhances money management by ensuring financial goals and emergency funds are funded first, reducing overspending and improving long-term financial stability.

Dynamic Incremental Allocation

Dynamic Incremental Allocation in budgeting strategically increases funds based on performance metrics and project needs, optimizing resource distribution over static increments. This method contrasts with Reverse Budgeting by proactively adjusting allocations to align with evolving financial goals and operational demands, thereby enhancing financial agility and control.

Backward Budgeting

Backward budgeting allocates expenses based on fixed financial goals by working backward from desired savings targets to fixed costs, enhancing control over spending and improving goal achievement. This method contrasts with incremental budgeting, which adjusts prior budgets incrementally without necessarily aligning expenditures to specific savings outcomes.

Slack Reduction Incrementalism

Incremental budgeting allocates funds based on small increases from previous budgets, often preserving slack that reduces efficiency, whereas reverse budgeting actively minimizes slack by focusing on essential expenses and cutting excess, promoting lean financial management. Slack reduction incrementalism enhances budget discipline by systematically identifying and eliminating non-essential expenditures, driving optimized resource allocation and improved fiscal responsibility.

Inverse Expense Forecasting

Incremental budgeting adjusts prior budgets with small changes, focusing on past expenses, while reverse budgeting, or zero-based budgeting, starts from zero and allocates funds based on actual needs, enhancing Inverse Expense Forecasting by predicting expenses in reverse order to optimize cash flow. Reverse budgeting supports more strategic money management by identifying essential costs first, reducing unnecessary spending, and improving financial forecasting accuracy.

Micro-Incremental Tracking

Micro-incremental tracking in incremental budgets allows precise allocation of small expense increases aligned with income growth, enhancing financial control and flexibility. Reverse budgets prioritize savings first by setting aside fixed amounts before spending, but micro-incremental tracking in incremental budgeting provides granular adjustments that optimize daily money management and long-term financial goals.

Bottom-Up Reverse Budgeting

Bottom-Up Reverse Budgeting prioritizes saving and investments by first allocating funds to financial goals before managing expenses, contrasting traditional Incremental Budgeting which adjusts previous budgets incrementally. This method enhances money management by ensuring savings targets are met first, improving financial discipline and long-term wealth accumulation.

Real-Time Reverse Fund Flow

Incremental budget allocates funds based on previous spending patterns, leading to rigid financial plans, whereas reverse budget prioritizes savings first by allocating money backward from income to expenses, enabling real-time reverse fund flow for dynamic money management. Real-time reverse fund flow optimizes cash utilization by immediately directing surplus funds into savings or investments, enhancing financial flexibility and control.

Negative Baseline Budgeting

Incremental budgeting increases the previous period's budget by a set percentage, often perpetuating inefficiencies, while reverse budgeting--also known as Negative Baseline Budgeting--starts from zero and justifies every expense, ensuring stricter cost control and resource optimization. Negative Baseline Budgeting forces organizations to critically evaluate all expenditures, preventing automatic budget increases and promoting more strategic financial management.

Incremental budget vs Reverse budget for money management. Infographic