Incremental budgeting allocates funds based on prior budgets with minor adjustments, ensuring steady financial control and predictable resource distribution. In contrast, a sinking fund strategy involves setting aside money over time for specific future expenses, promoting disciplined savings and reducing financial strain during large capital expenditures. Choosing between these approaches depends on organizational goals, with incremental budgeting supporting operational consistency and sinking funds enhancing long-term financial preparedness.

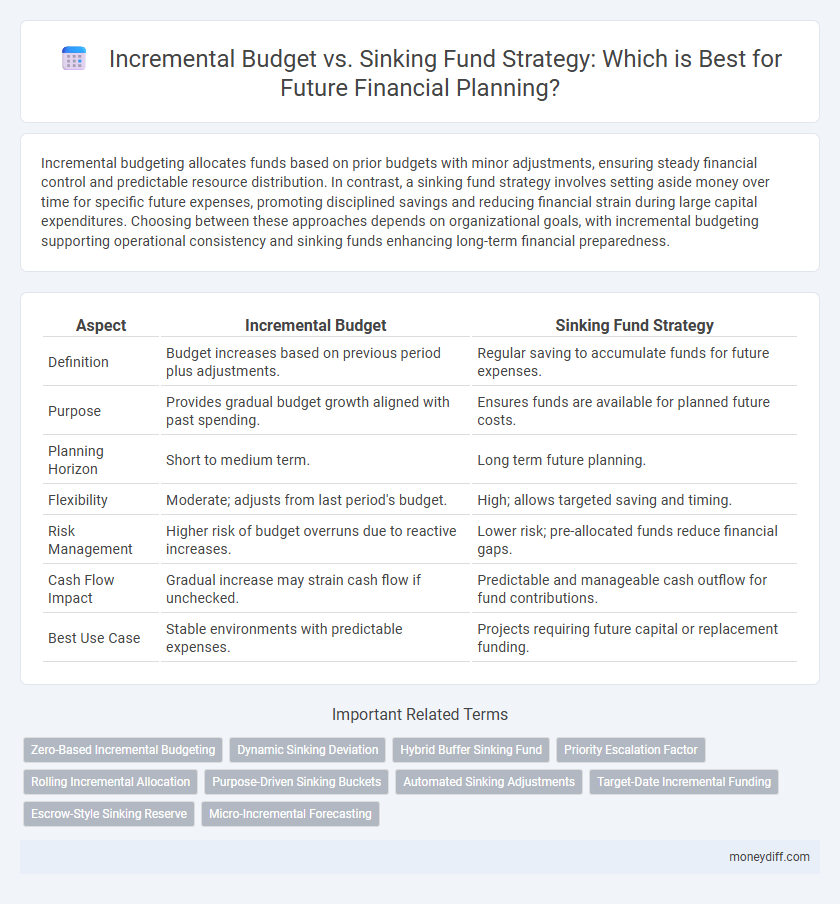

Table of Comparison

| Aspect | Incremental Budget | Sinking Fund Strategy |

|---|---|---|

| Definition | Budget increases based on previous period plus adjustments. | Regular saving to accumulate funds for future expenses. |

| Purpose | Provides gradual budget growth aligned with past spending. | Ensures funds are available for planned future costs. |

| Planning Horizon | Short to medium term. | Long term future planning. |

| Flexibility | Moderate; adjusts from last period's budget. | High; allows targeted saving and timing. |

| Risk Management | Higher risk of budget overruns due to reactive increases. | Lower risk; pre-allocated funds reduce financial gaps. |

| Cash Flow Impact | Gradual increase may strain cash flow if unchecked. | Predictable and manageable cash outflow for fund contributions. |

| Best Use Case | Stable environments with predictable expenses. | Projects requiring future capital or replacement funding. |

Understanding Incremental Budgeting

Incremental budgeting involves adjusting previous budgets by a fixed percentage to forecast future financial needs, simplifying the budgeting process and ensuring continuity in resource allocation. This method allows organizations to plan incrementally based on past expenditures, making small adjustments for anticipated changes in operations or inflation. Unlike sinking fund strategies that set aside funds for future expenses, incremental budgeting focuses on gradual budget increases tied to historical data, facilitating ongoing financial management and control.

What Is a Sinking Fund Strategy?

A sinking fund strategy involves setting aside a specific amount of money regularly to accumulate funds for a future expense or debt repayment, ensuring financial readiness without impacting the operating budget. Unlike incremental budgeting, which adjusts budget amounts based on past expenditures, the sinking fund method promotes disciplined saving over time for targeted financial goals. This approach minimizes the risk of sudden large financial burdens by smoothing out expenses through planned, incremental contributions.

Key Differences Between Incremental Budget and Sinking Fund

Incremental budgeting allocates funds based on previous budgets with slight adjustments, emphasizing predictable annual expenditures, while sinking fund strategy involves setting aside money gradually for a specific future expense, ensuring availability without borrowing. Incremental budgets prioritize short-term flexibility and continuity, whereas sinking funds focus on long-term financial planning and debt avoidance. Organizations seeking stability favor incremental budgeting, whereas strategic investments and debt-heavy projects benefit from sinking fund approaches.

Benefits of Incremental Budgeting for Financial Planning

Incremental budgeting offers a streamlined approach to financial planning by adjusting previous budgets with predictable increases or decreases, ensuring stability and ease of implementation. This method enhances accuracy in forecasting future expenditures and revenues, facilitating better control over operational costs. Its simplicity reduces administrative burden, allowing organizations to allocate resources efficiently while maintaining focus on core activities.

Advantages of Using a Sinking Fund Approach

A sinking fund strategy allows organizations to systematically set aside funds over time, ensuring that future expenses or debt repayments are covered without causing financial strain. This method enhances financial discipline by reducing the risk of sudden large expenditures and improving cash flow predictability. Compared to incremental budgeting, sinking funds provide a clear, long-term savings plan that supports fiscal stability and reduces the need for emergency borrowing.

Drawbacks of Incremental Budgeting Methods

Incremental budgeting often leads to inefficiencies by perpetuating past expenditures without critically evaluating the necessity or potential savings, causing resource misallocation and limiting innovation. This method can mask underlying financial issues as it assumes previous budgets are largely appropriate, hindering strategic adjustments for future uncertainties. Organizations using incremental budgeting may also struggle with inflexibility, making it difficult to reallocate funds in response to changing priorities or unexpected expenses.

Limitations of Sinking Fund Strategies

Sinking fund strategies for future planning often face limitations such as reduced flexibility due to earmarked reserves that cannot be reallocated to other urgent needs. These funds may also lead to opportunity costs, as capital tied up in sinking funds cannot be invested in higher-yield ventures. Additionally, sinking funds require disciplined, consistent contributions, and any lapses can jeopardize the availability of funds when large expenditures arise.

Choosing the Right Savings Strategy for Your Goals

Incremental Budgeting involves allocating additional funds periodically to cover future expenses, providing flexibility for evolving financial goals. The Sinking Fund Strategy requires setting aside fixed amounts regularly to accumulate a specific target, ensuring disciplined savings for planned expenditures. Selecting the right savings strategy depends on your timeline, financial discipline, and the predictability of your expenses.

Real-Life Examples: Incremental Budget vs Sinking Fund

Incremental budgeting, as used by corporations like Apple, focuses on adjusting prior budgets slightly to accommodate predictable expenses, promoting stability and ease of planning. Conversely, the sinking fund strategy, employed by municipal governments for infrastructure projects, involves setting aside funds gradually over time to cover large future expenses without sudden financial strain. Comparing real-life applications reveals that incremental budgeting suits steady-growth contexts, while sinking funds excel in managing long-term, capital-intensive commitments.

Final Thoughts: Optimizing Long-Term Financial Planning

Incremental budgeting focuses on adjusting previous budgets to allocate resources with minor changes, while sinking fund strategy involves setting aside specific amounts regularly for future liabilities or investments. Choosing the sinking fund approach enhances financial discipline and ensures dedicated resources for anticipated expenses, reducing reliance on uncertain revenues. Integrating both methods strategically optimizes long-term financial planning by balancing adaptability with proactive savings.

Related Important Terms

Zero-Based Incremental Budgeting

Zero-based incremental budgeting allocates funds by justifying each expense from a zero base, ensuring precise resource distribution aligned with current organizational goals. This strategic approach contrasts with sinking fund strategies by emphasizing cost-efficiency and detailed financial scrutiny rather than gradual accumulation for future liabilities.

Dynamic Sinking Deviation

Incremental budget strategies allocate funds based on past expenditures, risking inefficiencies when future needs deviate significantly, whereas sinking fund strategies accumulate reserves over time to better absorb dynamic sinking deviations and unforeseen financial demands. Employing a sinking fund approach enhances fiscal flexibility and accuracy in future planning by systematically addressing anticipated and variable liabilities, reducing the impact of budget shortfalls common in incremental budgeting.

Hybrid Buffer Sinking Fund

Hybrid Buffer Sinking Fund combines incremental budget allocations with a dedicated sinking fund to ensure steady financial growth while maintaining liquidity for future expenses. This strategy optimizes cash flow management by spreading contributions over time and consolidating reserves, reducing the risk of large, abrupt financial outlays.

Priority Escalation Factor

Incremental budget allocates funds based on past expenditures, often limiting flexibility in addressing Priority Escalation Factors that require rapid resource reallocation for emerging needs. In contrast, the sinking fund strategy accumulates reserves over time, enabling proactive responses to escalating priorities by ensuring dedicated financial resources are available when needed.

Rolling Incremental Allocation

Rolling Incremental Allocation in budgeting involves continuously adjusting funds based on prior expenditures and projected needs, enabling flexible and responsive financial planning. This strategy contrasts with the Sinking Fund approach by emphasizing incremental yearly budget increments rather than accumulating lump-sum reserves for future expenses.

Purpose-Driven Sinking Buckets

Incremental budgeting allocates funds based on previous budgets with slight adjustments, which may overlook future financial obligations, whereas purpose-driven sinking buckets earmark specific amounts regularly to cover anticipated large expenses, ensuring targeted savings and reducing fiscal risks. Employing sinking fund strategies enhances financial discipline by aligning budget allocations directly with planned expenditures, promoting transparent and goal-oriented fiscal management.

Automated Sinking Adjustments

Incremental budgeting allocates fixed increases based on previous budgets, which may overlook changing financial needs, whereas the sinking fund strategy automates sinking adjustments by systematically setting aside funds at predetermined intervals for future expenses or debt repayment. Automated sinking adjustments optimize cash flow management and enhance long-term financial planning accuracy by reducing manual intervention and forecasting errors.

Target-Date Incremental Funding

Target-date incremental funding allocates specific amounts of budget each period to meet a predefined financial goal by a set date, ensuring steady progress toward future obligations. This approach contrasts with sinking fund strategies by emphasizing gradual, time-bound increments rather than accumulating a lump sum, optimizing cash flow management and risk mitigation in long-term planning.

Escrow-Style Sinking Reserve

An escrow-style sinking reserve strategically allocates funds over time to cover large future expenses, ensuring financial stability without sudden budget shocks, unlike incremental budgeting which increases funds gradually but may lack long-term risk mitigation. This method provides a systematic approach to future planning by accumulating reserves in a dedicated account, promoting disciplined savings and improved cash flow management.

Micro-Incremental Forecasting

Micro-incremental forecasting enhances the incremental budget approach by allowing precise, small-scale adjustments aligned with real-time financial performance, improving accuracy in resource allocation. Compared to the sinking fund strategy, which allocates fixed sums for future expenses, micro-incremental budgeting offers greater flexibility and responsiveness to evolving operational needs and market conditions.

Incremental Budget vs Sinking Fund Strategy for future planning. Infographic