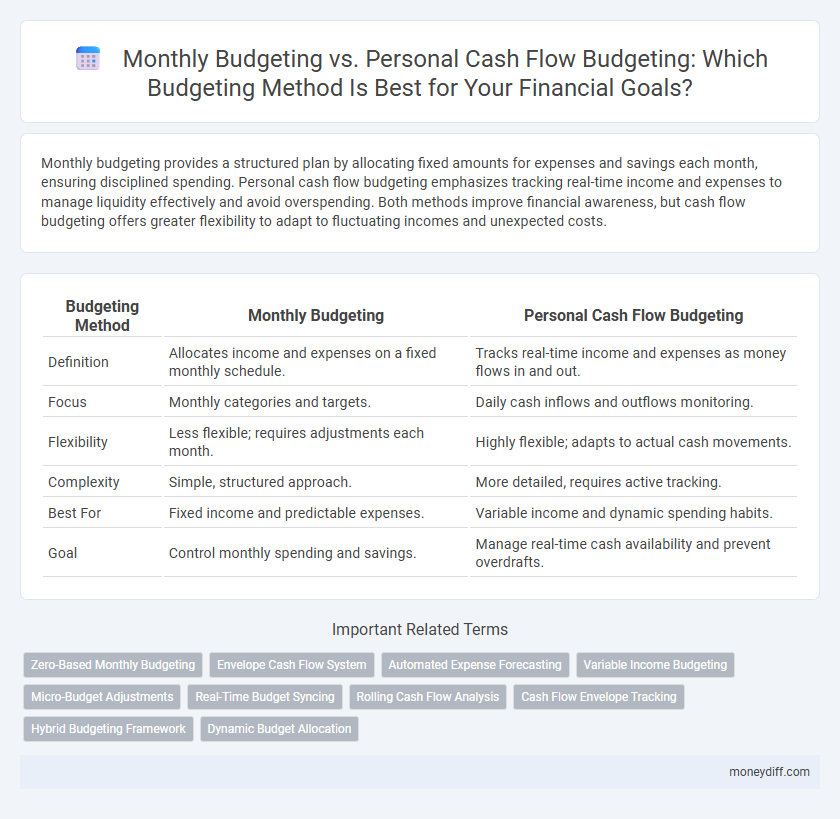

Monthly budgeting provides a structured plan by allocating fixed amounts for expenses and savings each month, ensuring disciplined spending. Personal cash flow budgeting emphasizes tracking real-time income and expenses to manage liquidity effectively and avoid overspending. Both methods improve financial awareness, but cash flow budgeting offers greater flexibility to adapt to fluctuating incomes and unexpected costs.

Table of Comparison

| Budgeting Method | Monthly Budgeting | Personal Cash Flow Budgeting |

|---|---|---|

| Definition | Allocates income and expenses on a fixed monthly schedule. | Tracks real-time income and expenses as money flows in and out. |

| Focus | Monthly categories and targets. | Daily cash inflows and outflows monitoring. |

| Flexibility | Less flexible; requires adjustments each month. | Highly flexible; adapts to actual cash movements. |

| Complexity | Simple, structured approach. | More detailed, requires active tracking. |

| Best For | Fixed income and predictable expenses. | Variable income and dynamic spending habits. |

| Goal | Control monthly spending and savings. | Manage real-time cash availability and prevent overdrafts. |

Understanding Monthly Budgeting: Key Concepts

Monthly budgeting involves creating a detailed plan that allocates income toward fixed and variable expenses within a specific month, ensuring financial discipline and timely bill payments. It emphasizes tracking income sources, categorizing expenses, and setting spending limits to avoid overspending. Key concepts include distinguishing between essential and discretionary expenses and adjusting allocations based on monthly income fluctuations.

What Is Personal Cash Flow Budgeting?

Personal cash flow budgeting involves tracking income and expenses on a monthly basis to manage the actual movement of money in and out of accounts. Unlike traditional monthly budgeting, which allocates fixed amounts to spending categories, personal cash flow budgeting emphasizes real-time cash availability and prioritizes spending based on incoming cash flow. This approach helps individuals maintain liquidity, avoid overdrafts, and adjust spending dynamically based on current financial conditions.

Comparing Monthly and Personal Cash Flow Budgets

Monthly budgeting organizes income and expenses based on fixed calendar periods, providing a clear overview of financial obligations and savings goals each month. Personal cash flow budgeting tracks daily inflows and outflows, offering real-time insight into liquidity and spending habits to prevent shortfalls. Comparing both methods reveals that monthly budgets aid in long-term planning, while personal cash flow budgets enhance short-term financial control and flexibility.

Pros and Cons of Monthly Budgeting

Monthly budgeting offers a clear overview of income and expenses within a fixed period, making it easier to track regular bills and savings goals. However, it may overlook daily spending fluctuations and irregular expenses, leading to less flexibility in managing unexpected costs. While monthly budgeting promotes discipline, it can sometimes result in budget fatigue and less accurate real-time cash flow insights.

Benefits of Tracking Personal Cash Flow

Tracking personal cash flow provides real-time insight into income and expenses, enabling more accurate adjustments to spending habits. It helps identify cash shortages or surpluses promptly, improving financial decision-making and avoiding debt accumulation. This method enhances financial transparency and supports long-term money management goals beyond fixed monthly budgeting limits.

Which Budget Method Suits Your Financial Goals?

Monthly budgeting provides a structured approach by allocating fixed amounts to expenses each month, ideal for those with steady incomes and regular bills. Personal cash flow budgeting tracks actual inflows and outflows daily, making it suitable for individuals with variable income or fluctuating expenses who need real-time financial insights. Choosing between these methods depends on your financial goals, such as maintaining consistent savings targets or managing irregular cash flow for maximum control.

Tools and Apps for Effective Budget Management

Monthly budgeting tools like YNAB and EveryDollar provide structured frameworks for tracking fixed expenses and setting spending limits, helping users maintain discipline in their spending habits. Personal cash flow budgeting apps such as Mint and PocketGuard offer real-time updates on income and expenses, enabling more dynamic money management through alerts and automatic transaction categorization. Combining these apps enhances budget accuracy and financial insight, promoting effective budget management tailored to individual needs.

Common Mistakes in Budget Planning

Common mistakes in budget planning include underestimating monthly expenses and neglecting irregular cash inflows when using monthly budgeting. Personal cash flow budgeting often fails due to inaccurate tracking of day-to-day spending and overlooking variable income sources. Effective budgeting requires precise categorization of fixed and variable costs along with continuous monitoring to avoid overspending and financial shortfalls.

Adapting Budget Strategies to Income Fluctuations

Monthly budgeting provides a fixed framework for managing expenses based on a set income, offering stability for predictable earnings. Personal cash flow budgeting adapts to income fluctuations by tracking inflows and outflows in real-time, ensuring flexibility during variable pay periods. Implementing cash flow strategies helps individuals maintain financial control and adjust spending proactively, minimizing the risk of overspending during low-income phases.

Tips for Staying Consistent with Your Budgeting Approach

Establishing a clear routine by setting specific days each month for reviewing your monthly budget or personal cash flow helps maintain consistency. Using budgeting apps that track expenses in real-time enhances accuracy and accountability for both methods. Prioritize adjusting budget categories based on spending patterns identified during reviews to stay aligned with financial goals and avoid overspending.

Related Important Terms

Zero-Based Monthly Budgeting

Zero-based monthly budgeting requires allocating every dollar of income to specific expenses, savings, or debt repayment, ensuring no unassigned funds remain at the end of each month. This approach enhances cash flow control by promoting disciplined spending and maximizing financial efficiency compared to traditional personal cash flow budgeting methods.

Envelope Cash Flow System

The Envelope Cash Flow System enhances monthly budgeting by allocating specific cash amounts to categorized envelopes, ensuring disciplined spending aligned with personal financial goals. This method improves personal cash flow budgeting by providing a tangible framework to track and control expenses, promoting better money management and preventing overspending.

Automated Expense Forecasting

Monthly budgeting provides a fixed framework for tracking income and expenses each month, while personal cash flow budgeting offers dynamic, real-time insights into cash inflows and outflows. Automated expense forecasting enhances both methods by using historical data and machine learning to predict future spending patterns, improving financial planning accuracy and helping avoid cash shortages.

Variable Income Budgeting

Monthly budgeting allocates fixed amounts to expenses based on anticipated income, while personal cash flow budgeting dynamically tracks variable income and expenses in real-time, providing flexibility for irregular earnings such as freelance payments or commissions. Effective variable income budgeting relies on forecasting income fluctuations and prioritizing essential expenses to maintain financial stability despite inconsistent cash flow.

Micro-Budget Adjustments

Monthly budgeting provides a structured overview of income and expenses, allowing for scheduled micro-budget adjustments that align spending with financial goals. Personal cash flow budgeting tracks daily transactions in real-time, enabling immediate micro-adjustments to prevent overspending and maintain financial stability.

Real-Time Budget Syncing

Real-time budget syncing enhances monthly budgeting by automatically updating expenses and income, providing an accurate snapshot of financial status at any moment. Personal cash flow budgeting benefits from this dynamic synchronization by tracking daily inflows and outflows, enabling timely adjustments to spending habits and financial goals.

Rolling Cash Flow Analysis

Rolling cash flow analysis provides a dynamic approach to monthly budgeting by continuously updating inflows and outflows, allowing for real-time adjustments and improved financial forecasting. Personal cash flow budgeting emphasizes tracking actual income and expenses to maintain liquidity, ensuring spending aligns with financial goals and prevents shortfalls.

Cash Flow Envelope Tracking

Monthly budgeting provides a fixed allocation of expenses based on income earned within a month, while personal cash flow budgeting emphasizes real-time tracking of inflows and outflows to maintain optimal liquidity. Cash flow envelope tracking segments funds into virtual envelopes tied to specific spending categories, enabling precise control over variable expenses and preventing overspending by aligning budget limits with actual cash availability.

Hybrid Budgeting Framework

Hybrid budgeting frameworks combine monthly budgeting with personal cash flow analysis to create a dynamic financial plan optimized for both short-term expense tracking and long-term financial health. By integrating fixed monthly budget categories with variable cash flow insights, individuals can better manage irregular income and anticipate fluctuations, enhancing overall budget accuracy and financial stability.

Dynamic Budget Allocation

Monthly budgeting offers a static snapshot focused on predetermined income and expenses, while personal cash flow budgeting enables dynamic budget allocation by continuously tracking real-time inflows and outflows. Leveraging cash flow data allows for agile adjustments to spending, savings, and debt repayment strategies, optimizing financial flexibility and responsiveness.

Monthly Budgeting vs Personal Cash Flow Budgeting for Budget Infographic