Traditional budgeting relies on historical data to allocate funds, adjusting previous budgets with incremental changes. Zero-based budgeting requires building the budget from scratch each period, justifying every expense to optimize resource allocation. This approach promotes greater financial discipline and efficiency by eliminating unnecessary expenditures.

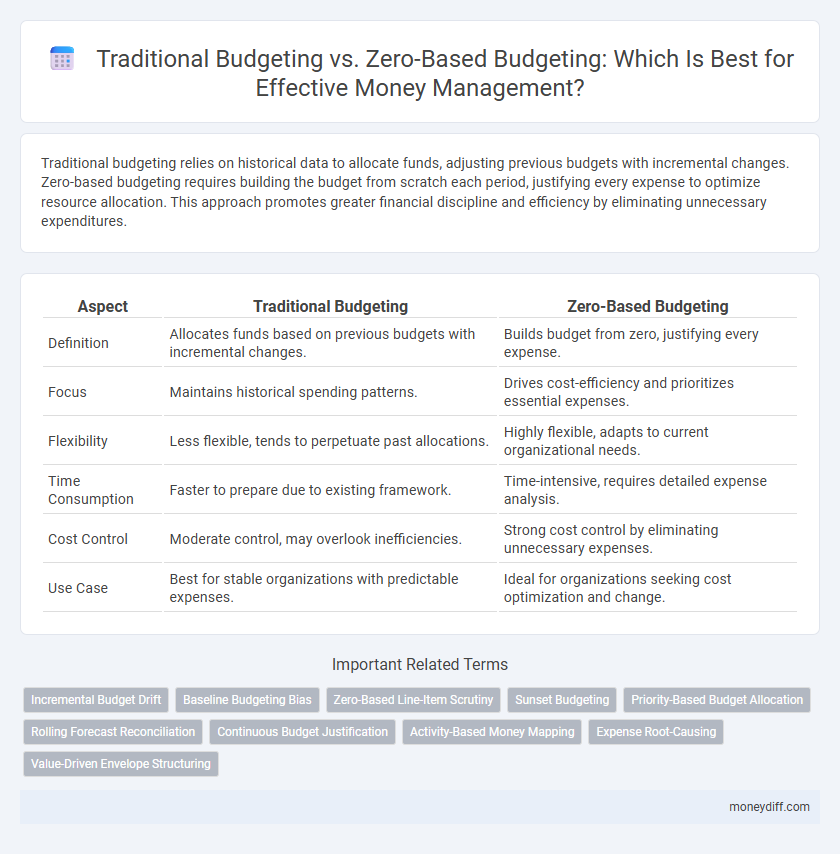

Table of Comparison

| Aspect | Traditional Budgeting | Zero-Based Budgeting |

|---|---|---|

| Definition | Allocates funds based on previous budgets with incremental changes. | Builds budget from zero, justifying every expense. |

| Focus | Maintains historical spending patterns. | Drives cost-efficiency and prioritizes essential expenses. |

| Flexibility | Less flexible, tends to perpetuate past allocations. | Highly flexible, adapts to current organizational needs. |

| Time Consumption | Faster to prepare due to existing framework. | Time-intensive, requires detailed expense analysis. |

| Cost Control | Moderate control, may overlook inefficiencies. | Strong cost control by eliminating unnecessary expenses. |

| Use Case | Best for stable organizations with predictable expenses. | Ideal for organizations seeking cost optimization and change. |

Introduction to Traditional and Zero-Based Budgeting

Traditional budgeting allocates funds based on historical spending patterns, ensuring continuity and simplicity in financial planning, but may perpetuate inefficiencies by assuming past expenses remain relevant. Zero-based budgeting requires every expense to be justified from scratch each period, promoting cost-effectiveness and resource optimization by aligning expenditures directly with current goals. Both methods serve distinct purposes in budgeting strategies, with traditional budgeting favoring stability and zero-based budgeting emphasizing accountability and operational efficiency.

Core Principles of Traditional Budgeting

Traditional budgeting relies on historical data to allocate funds, emphasizing incremental changes from prior budgets to forecast future expenditures. It prioritizes stability and predictability by adjusting previous budget levels rather than reevaluating all expenses from scratch. This method streamlines the budgeting process but may perpetuate inefficiencies by maintaining existing spending patterns without questioning their necessity.

Key Features of Zero-Based Budgeting

Zero-Based Budgeting (ZBB) requires every expense to be justified from zero at the beginning of each budget cycle, contrasting traditional budgeting which often adjusts previous budgets incrementally. ZBB promotes resource optimization by aligning every dollar spent with current organizational goals, eliminating unnecessary expenditures. Key features include detailed cost analysis, priority-based funding, and enhanced financial accountability, leading to improved cost control and strategic allocation of funds.

Advantages of Traditional Budgeting

Traditional budgeting offers simplicity and stability by using historical financial data to guide future spending, making it easier for organizations to plan and predict expenses. It allows for efficient allocation of resources through incremental adjustments, reducing the time and effort required for budget preparation. This method also fosters consistency and accountability across departments, supporting long-term financial goals and operational continuity.

Benefits of Zero-Based Budgeting

Zero-Based Budgeting enhances financial efficiency by requiring justification for all expenses, eliminating unnecessary costs and promoting resource optimization. It increases transparency and accountability in budget allocation, enabling more strategic decision-making aligned with current organizational goals. This approach empowers businesses to adapt quickly to changing financial conditions, ensuring funds are directed toward high-priority initiatives.

Common Challenges with Traditional Budgeting

Traditional budgeting often struggles with inflexible allocation based on historical expenses, leading to inefficient resource distribution. This approach can cause budgetary padding and reduced cost control, limiting financial transparency and adaptability. Organizations frequently face challenges such as entrenched spending patterns and lack of alignment with current strategic goals.

Potential Drawbacks of Zero-Based Budgeting

Zero-Based Budgeting (ZBB) can be time-consuming and resource-intensive, requiring detailed justification for every expense each budgeting cycle. Its complexity may overwhelm employees and managers, leading to potential bottlenecks and inefficiencies in the budgeting process. Furthermore, frequent scrutiny and re-evaluation can cause short-term decision-making, possibly neglecting long-term financial planning and strategic goals.

Cost-Saving Opportunities: Traditional vs Zero-Based

Traditional budgeting often perpetuates past expenses, which can limit the identification of new cost-saving opportunities, while zero-based budgeting requires every expense to be justified from scratch, uncovering inefficiencies and waste. By eliminating assumptions based on historical spending, zero-based budgeting enables organizations to allocate resources more strategically and prioritize high-impact initiatives. This rigorous review process typically results in greater cost savings compared to traditional methods, making zero-based budgeting a powerful tool for optimizing financial performance.

Selecting the Right Budgeting Method for Your Finances

Selecting the right budgeting method depends on your financial goals and spending habits; traditional budgeting allocates funds based on historical expenses, offering stability and simplicity for consistent cash flow management. Zero-based budgeting requires every dollar to be assigned a specific purpose, promoting efficient allocation by justifying expenses from scratch each period, which is ideal for those seeking tighter control and cost optimization. Evaluating your income variability and financial discipline helps determine whether a predictable framework or a detailed, needs-based approach best supports your money management strategy.

Summary: Which Budgeting Style Fits Your Money Management Goals?

Traditional budgeting relies on historical data to allocate funds, making it suitable for stable expenses and predictable cash flow. Zero-based budgeting requires justifying every expense from scratch, promoting efficiency and aligning spending with current financial goals. Choose traditional budgeting for consistency and zero-based budgeting for adaptive, goal-driven money management.

Related Important Terms

Incremental Budget Drift

Incremental budget drift commonly occurs in traditional budgeting, where previous budgets form the baseline and small adjustments accumulate over time, leading to inefficiencies and outdated allocations. Zero-based budgeting eliminates this drift by requiring each expense to be justified from scratch, ensuring a more accurate and rational allocation of resources aligned with current priorities.

Baseline Budgeting Bias

Traditional budgeting often suffers from baseline budgeting bias, where past expenditures become the default reference point, leading to incremental increases regardless of current needs or priorities. Zero-based budgeting eliminates this bias by requiring all expenses to be justified from scratch, promoting more efficient resource allocation and cost control.

Zero-Based Line-Item Scrutiny

Zero-based budgeting requires each expense to be justified from scratch, promoting detailed line-item scrutiny that eliminates unnecessary costs and improves financial efficiency. Unlike traditional budgeting, which adjusts previous budgets incrementally, zero-based budgeting ensures every dollar is purposefully allocated based on current needs and priorities.

Sunset Budgeting

Sunset Budgeting integrates principles from both Traditional and Zero-Based Budgeting by regularly reviewing and eliminating outdated or unnecessary expenses within each budget cycle, ensuring funds are allocated only to active, justified projects. This approach enhances financial discipline and resource optimization by mandating periodic reassessment and automatic expiration of budget items unless renewed.

Priority-Based Budget Allocation

Traditional budgeting allocates funds based on historical spending patterns, often perpetuating inefficiencies by prioritizing previous allocations rather than current needs. Zero-based budgeting improves money management by requiring every expense to be justified from scratch, enabling priority-based budget allocation that aligns resources with organizational goals and shifts spending towards high-impact activities.

Rolling Forecast Reconciliation

Rolling forecast reconciliation enhances financial accuracy by continuously aligning budget forecasts with actual spending, reducing discrepancies common in traditional budgeting cycles. Zero-based budgeting complements this process by requiring justification for every expense, promoting more precise resource allocation and dynamic adjustments throughout the forecast period.

Continuous Budget Justification

Traditional budgeting relies on incremental adjustments from previous budgets, often leading to unquestioned expenditure baselines, while zero-based budgeting requires continuous budget justification for every expense, promoting more efficient resource allocation. Continuous budget justification in zero-based budgeting enhances financial discipline and prevents budget inflation by scrutinizing each cost element from a zero base.

Activity-Based Money Mapping

Activity-based money mapping provides granular insight into spending patterns by tracing every expense to specific activities, enhancing accuracy in zero-based budgeting compared to traditional budgeting's reliance on historical data. This approach enables more precise allocation of resources by evaluating the necessity and value of each activity, driving cost efficiency and strategic financial management.

Expense Root-Causing

Traditional budgeting relies on historical spending patterns, making it less effective at identifying the root causes of expenses and often perpetuating inefficient costs. Zero-based budgeting starts from a "zero base," requiring every expense to be justified, which enhances expense root-causing by promoting detailed financial scrutiny and optimized resource allocation.

Value-Driven Envelope Structuring

Traditional budgeting allocates funds based on historical spending patterns, often perpetuating inefficiencies, while zero-based budgeting requires each expense to be justified from scratch, promoting value-driven envelope structuring by aligning expenditures precisely with organizational goals. This approach enhances financial discipline and resource optimization by categorizing budgets into specific value envelopes that reflect strategic priorities and measurable outcomes.

Traditional Budgeting vs Zero-Based Budgeting for money management. Infographic