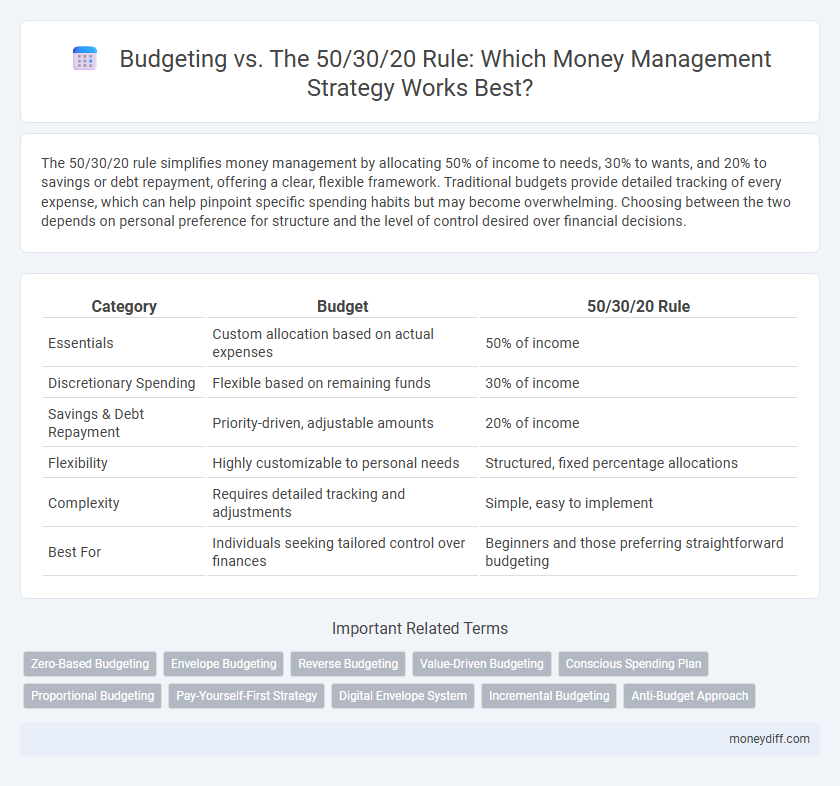

The 50/30/20 rule simplifies money management by allocating 50% of income to needs, 30% to wants, and 20% to savings or debt repayment, offering a clear, flexible framework. Traditional budgets provide detailed tracking of every expense, which can help pinpoint specific spending habits but may become overwhelming. Choosing between the two depends on personal preference for structure and the level of control desired over financial decisions.

Table of Comparison

| Category | Budget | 50/30/20 Rule |

|---|---|---|

| Essentials | Custom allocation based on actual expenses | 50% of income |

| Discretionary Spending | Flexible based on remaining funds | 30% of income |

| Savings & Debt Repayment | Priority-driven, adjustable amounts | 20% of income |

| Flexibility | Highly customizable to personal needs | Structured, fixed percentage allocations |

| Complexity | Requires detailed tracking and adjustments | Simple, easy to implement |

| Best For | Individuals seeking tailored control over finances | Beginners and those preferring straightforward budgeting |

Understanding Traditional Budgeting Methods

Traditional budgeting methods focus on allocating fixed amounts of income to essential categories like housing, food, and transportation, ensuring disciplined control over expenses. Unlike the 50/30/20 rule, which divides income into needs, wants, and savings percentages, traditional budgets offer detailed tracking and prioritization of every dollar spent. This granular approach helps identify unnecessary costs and optimize financial planning for short-term and long-term goals.

What Is the 50/30/20 Rule?

The 50/30/20 rule is a simplified money management guideline that allocates 50% of income to needs, 30% to wants, and 20% to savings or debt repayment. This budgeting framework emphasizes balanced financial planning by ensuring essentials are covered first, followed by discretionary spending and long-term financial goals. Its flexibility allows individuals to maintain control over their finances while promoting responsible saving habits.

Key Differences Between Budgeting and the 50/30/20 Rule

Budgeting involves creating a detailed plan that allocates every dollar of income to specific expenses, savings, and debt repayment categories, offering precise control over finances. The 50/30/20 rule simplifies money management by dividing income into three broad categories: 50% for needs, 30% for wants, and 20% for savings or debt repayment, promoting balanced spending without granular tracking. Key differences include the level of specificity and flexibility; budgeting requires continuous monitoring and adjustments, whereas the 50/30/20 rule provides a straightforward guideline ideal for those seeking simplicity.

Pros and Cons of Traditional Budgeting

Traditional budgeting provides a detailed plan for income allocation, promoting disciplined spending and savings habits that can prevent financial shortfalls. However, its rigidity often leads to frustration due to unrealistic expense predictions and limited flexibility, which can result in budget fatigue and decreased adherence over time. Unlike the 50/30/20 rule that offers simplicity and adaptive guidance, traditional budgeting demands continuous tracking and adjustments, potentially overwhelming individuals without strong financial discipline.

Benefits and Limitations of the 50/30/20 Rule

The 50/30/20 rule simplifies money management by allocating 50% of income to needs, 30% to wants, and 20% to savings or debt repayment, promoting clear financial priorities and easy tracking. This method benefits those seeking a straightforward framework for balanced spending without complex calculations but may be less effective for individuals with irregular incomes or unique financial obligations. Limitations include its lack of customization for high-cost living areas and insufficient guidance for long-term investment planning, making it a starting point rather than a comprehensive solution.

Choosing the Right Money Management Strategy

Selecting the right money management strategy depends on your financial goals and spending habits, with the 50/30/20 rule offering a simple framework dividing income into needs, wants, and savings, while a detailed budget provides personalized control over every dollar. The 50/30/20 rule suits those seeking straightforward guidance, allocating 50% to necessities, 30% to discretionary spending, and 20% to savings or debt repayment. A tailored budget, however, enables tracking and adjusting expenses precisely, ideal for complex financial situations and achieving specific targets.

Who Should Use the 50/30/20 Rule?

The 50/30/20 rule is ideal for individuals seeking a straightforward, flexible framework to manage their finances without detailed expense tracking. This method suits people with stable incomes who want to balance needs, wants, and savings by allocating 50% to essentials, 30% to discretionary spending, and 20% to savings or debt repayment. Beginners in personal finance and those looking to simplify budgeting while maintaining financial discipline benefit most from this approach.

Common Budgeting Mistakes to Avoid

Overspending under the 50/30/20 rule often occurs when discretionary expenses exceed the 30% allocation, leading to financial imbalance. Failing to adjust budget categories in response to income changes can result in insufficient savings or debt accumulation. Ignoring emergency funds and unexpected expenses undermines long-term financial stability and disrupts effective money management.

How to Transition from Traditional Budgeting to the 50/30/20 Rule

Transitioning from traditional budgeting to the 50/30/20 rule involves categorizing income into three clear segments: 50% for needs, 30% for wants, and 20% for savings or debt repayment. Start by identifying fixed expenses like rent and utilities to fit into the needs category, then allocate discretionary spending under wants, ensuring flexible financial management. Tracking expenses with budgeting apps can facilitate adherence to these proportions, promoting balanced financial health and reducing overspending.

Practical Tips for Sticking to Your Chosen Method

Set clear spending limits aligned with your budget or 50/30/20 allocations to control expenses effectively. Track every transaction using budgeting apps or spreadsheets to maintain transparency and identify overspending early. Regularly review and adjust your spending categories to reflect lifestyle changes and stay committed to your financial goals.

Related Important Terms

Zero-Based Budgeting

Zero-based budgeting requires allocating every dollar of income to specific expenses, savings, or debt repayment, ensuring no money is left unassigned. Unlike the 50/30/20 rule which divides income into fixed percentages for needs, wants, and savings, zero-based budgeting provides granular control and customization to maximize financial efficiency and reduce waste.

Envelope Budgeting

Envelope budgeting divides income into specific categories with fixed amounts to control spending and ensure savings, aligning effectively with the 50/30/20 rule's allocation to needs, wants, and savings. This method enhances financial discipline by physically or digitally separating funds, preventing overspending in discretionary areas and promoting adherence to predetermined budget percentages.

Reverse Budgeting

Reverse budgeting allocates savings and essential expenses before discretionary spending, aligning with the 50/30/20 rule by prioritizing financial goals and necessities first. This method enhances money management by securing savings targets upfront, reducing the risk of overspending in non-essential categories.

Value-Driven Budgeting

Value-driven budgeting prioritizes aligning expenses with core personal goals and values rather than rigid percentage allocations like the 50/30/20 rule, which divides income into needs, wants, and savings uniformly. This approach enhances financial flexibility and meaningful spending by customizing budgets to reflect individual priorities and maximize long-term satisfaction and financial well-being.

Conscious Spending Plan

The Conscious Spending Plan aligns with the 50/30/20 rule by allocating 50% of income to needs, 30% to wants, and 20% to savings or debt repayment, enhancing financial discipline through intentional choices. This approach improves money management by promoting awareness of spending habits and prioritizing long-term financial goals over impulsive expenditures.

Proportional Budgeting

Proportional budgeting allocates income into fixed percentages, such as 50% for needs, 30% for wants, and 20% for savings or debt repayment, providing a structured yet flexible framework for money management. This method contrasts with traditional budgeting by emphasizing balance and priority distribution, helping individuals maintain financial discipline while adapting to changing expenses.

Pay-Yourself-First Strategy

The Pay-Yourself-First strategy prioritizes saving a fixed percentage of income before allocating funds to expenses, aligning closely with the 50/30/20 rule by ensuring 20% goes directly into savings or investments. This approach enhances financial discipline, promoting wealth accumulation and reducing reliance on discretionary spending categories outlined in the 50/30/20 framework.

Digital Envelope System

The Digital Envelope System enhances the 50/30/20 rule by allocating funds into specific virtual categories, ensuring precise control over needs, wants, and savings without rigid percentages. This flexible budgeting approach leverages technology for real-time tracking, promoting disciplined spending while adapting to changing financial goals.

Incremental Budgeting

Incremental budgeting focuses on adjusting previous budgets by allocating additional funds based on incremental changes, contrasting with the 50/30/20 rule that divides income into fixed percentages for needs, wants, and savings. This approach allows organizations to systematically refine resources while maintaining financial targets, optimizing operational efficiency in budget management.

Anti-Budget Approach

The anti-budget approach simplifies money management by focusing on the 50/30/20 rule, allocating 50% of income to needs, 30% to wants, and 20% to savings or debt repayment without tracking every expense. This method reduces stress and increases flexibility compared to traditional budgets that require detailed tracking and rigid spending limits.

Budget vs 50/30/20 Rule for money management. Infographic