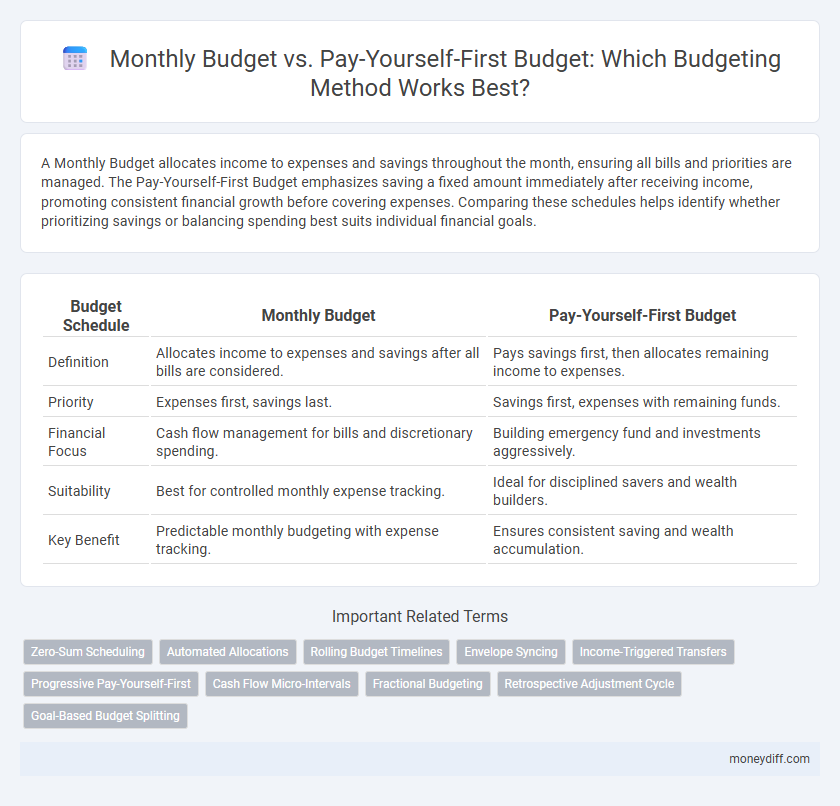

A Monthly Budget allocates income to expenses and savings throughout the month, ensuring all bills and priorities are managed. The Pay-Yourself-First Budget emphasizes saving a fixed amount immediately after receiving income, promoting consistent financial growth before covering expenses. Comparing these schedules helps identify whether prioritizing savings or balancing spending best suits individual financial goals.

Table of Comparison

| Budget Schedule | Monthly Budget | Pay-Yourself-First Budget |

|---|---|---|

| Definition | Allocates income to expenses and savings after all bills are considered. | Pays savings first, then allocates remaining income to expenses. |

| Priority | Expenses first, savings last. | Savings first, expenses with remaining funds. |

| Financial Focus | Cash flow management for bills and discretionary spending. | Building emergency fund and investments aggressively. |

| Suitability | Best for controlled monthly expense tracking. | Ideal for disciplined savers and wealth builders. |

| Key Benefit | Predictable monthly budgeting with expense tracking. | Ensures consistent saving and wealth accumulation. |

Understanding Monthly Budgeting: An Overview

Monthly budgeting involves allocating income across various expenses and savings within a specific month, promoting control over cash flow and financial goals. The Pay-Yourself-First budget method prioritizes saving by setting aside a predetermined amount before covering other expenses, ensuring consistent wealth building. Comparing these schedules highlights the importance of disciplined saving alongside careful monthly expense planning for effective financial management.

What Is the Pay-Yourself-First Budget Method?

The Pay-Yourself-First budget method prioritizes saving a fixed portion of income before allocating funds to expenses, ensuring consistent wealth accumulation. This approach contrasts with the traditional Monthly Budget, where spending categories are planned first, and savings are treated as leftover funds. By automating savings at the start of each pay period, the Pay-Yourself-First method promotes disciplined financial habits and long-term financial security.

Key Differences Between Monthly and Pay-Yourself-First Budgets

Monthly budgets allocate income across all expenses within a set timeframe, providing a detailed snapshot of spending and saving patterns. Pay-Yourself-First budgets prioritize saving by automatically setting aside a fixed amount before covering any expenses, fostering consistent wealth accumulation. The key difference lies in timing: monthly budgets manage expenses throughout the month, while pay-yourself-first ensures savings happen upfront, optimizing financial discipline.

Pros and Cons of Monthly Budget Schedules

Monthly budget schedules offer a clear overview of income and expenses for each month, facilitating timely bill payments and expense tracking. They help maintain spending discipline but may lack flexibility for irregular income or unexpected costs. The pay-yourself-first budget prioritizes savings upfront, whereas monthly budgets typically allocate funds after expenses are accounted, risking lower savings if overspending occurs.

Benefits of the Pay-Yourself-First Approach

The Pay-Yourself-First budget method prioritizes saving by automatically allocating funds to savings or investments before covering expenses, fostering consistent wealth growth and financial security. This approach reduces the temptation to overspend by treating savings as a non-negotiable expense, ensuring disciplined financial habits. Compared to traditional Monthly Budget schedules, Pay-Yourself-First enhances financial resilience and accelerates progress toward long-term goals.

Ideal Scenarios for Each Budgeting Method

The Monthly Budget method suits individuals with fluctuating incomes or expenses, providing flexibility to adjust allocations based on real-time financial status. The Pay-Yourself-First Budget is ideal for disciplined savers prioritizing consistent savings goals, as it automatically reserves funds before other expenditures. Selecting the right budgeting schedule enhances financial control by aligning strategy with personal income patterns and financial objectives.

Building Financial Discipline with Budgeting Schedules

The Monthly Budget allocates income across expenses and savings at month-end, promoting consistent tracking of spending habits. The Pay-Yourself-First Budget prioritizes saving by setting aside a fixed amount immediately upon receiving income, reinforcing disciplined financial habits. Both budgeting schedules cultivate financial discipline by ensuring regular contributions to savings and controlled expenditure.

How to Transition Between Budget Schedules

Transitioning from a Monthly Budget to a Pay-Yourself-First Budget schedule requires prioritizing savings by automatically allocating a fixed percentage of income to savings accounts before budgeting for expenses. Setting up direct deposits and adjusting bill payments according to the new schedule facilitates smoother cash flow management. Tracking expenses through budgeting apps or spreadsheets ensures adherence to the new allocation, promoting financial discipline and growth.

Common Budgeting Mistakes to Avoid

Monthly Budget schedules often lead to overspending as they allocate funds only after expenses occur, risking depletion before the next paycheck. Pay-Yourself-First Budget prioritizes saving by automatically setting aside a portion of income upfront, preventing the mistake of neglecting savings. Avoiding common budgeting mistakes like ignoring emergency funds and failing to track variable expenses is essential in both methods for long-term financial stability.

Choosing the Best Budget Strategy for Your Goals

A Monthly Budget allocates income across expenses, savings, and debts on a fixed schedule, ideal for managing variable cash flows and tracking spending patterns. The Pay-Yourself-First Budget prioritizes saving a predetermined amount immediately after income is received, fostering consistent wealth accumulation and financial discipline. Selecting the best budget strategy depends on your financial goals, income stability, and spending habits, with Pay-Yourself-First best for aggressive saving and Monthly Budget suited for comprehensive expense management.

Related Important Terms

Zero-Sum Scheduling

The Monthly Budget allocates every dollar of income to expenses, savings, and debt payments, achieving a zero-sum schedule where total income minus total outflows equals zero, ensuring no unassigned funds. The Pay-Yourself-First Budget prioritizes savings by setting aside a fixed amount upfront before expenses, embedding zero-sum scheduling discipline to guarantee savings goals are met before discretionary spending.

Automated Allocations

Monthly Budget schedules typically involve manual allocation of expenses and savings each month, requiring continuous tracking and adjustments. Pay-Yourself-First Budget leverages automated allocations by prioritizing savings transfers immediately upon income receipt, ensuring consistent investment in financial goals without relying on active management.

Rolling Budget Timelines

A Monthly Budget allocates income and expenses within fixed calendar months, providing clear short-term financial tracking but often lacks flexibility for irregular income. The Pay-Yourself-First Budget emphasizes saving a set amount before expenses, aligning well with rolling budget timelines by prioritizing savings continuously regardless of monthly fluctuations.

Envelope Syncing

Monthly Budget allocates funds based on income and expenses for the entire month, requiring regular manual tracking, while Pay-Yourself-First Budget prioritizes setting aside savings as the first expenditure, ensuring automatic Envelope Syncing aligns savings goals before spending categories. Envelope Syncing in the Pay-Yourself-First approach streamlines fund allocation by automatically adjusting available balances according to savings targets, reducing the risk of overspending in discretionary envelopes.

Income-Triggered Transfers

Monthly Budget schedules allocate expenses based on fixed dates, often leading to delayed savings, while Pay-Yourself-First Budget prioritizes income-triggered transfers that automatically set aside savings immediately upon receiving income. This income-driven approach enhances cash flow management and ensures consistent saving habits aligned with paycheck cycles.

Progressive Pay-Yourself-First

The Progressive Pay-Yourself-First budget method prioritizes setting aside savings before allocating funds to expenses, gradually increasing the savings rate each month to build financial security. Unlike traditional Monthly Budget schedules that distribute income primarily towards fixed and variable expenses, this approach ensures consistent wealth growth by systematically boosting savings contributions over time.

Cash Flow Micro-Intervals

Monthly Budget allocates expenses and income on a fixed monthly basis, which may overlook daily or weekly cash flow fluctuations, whereas the Pay-Yourself-First Budget prioritizes savings at the beginning of each income cycle, optimizing cash flow micro-intervals by ensuring funds are allocated before discretionary spending. This micro-interval focus improves financial discipline and liquidity management across varying income and expense timings.

Fractional Budgeting

Monthly Budget structures expenses by allocating income across fixed and variable categories each month, enabling detailed tracking of cash flow. Pay-Yourself-First Budget prioritizes saving a defined portion of income upfront, leveraging Fractional Budgeting to automatically divide funds into designated savings, investments, and spending fractions for disciplined financial growth.

Retrospective Adjustment Cycle

The Monthly Budget allows for regular expense tracking but often requires frequent retrospective adjustment cycles to realign spending with financial goals. In contrast, the Pay-Yourself-First Budget minimizes the need for such adjustments by prioritizing savings and fixed allocations upfront, creating a more stable and disciplined budget schedule.

Goal-Based Budget Splitting

Monthly budgets allocate expenses across standard categories to manage regular cash flow, while Pay-Yourself-First budgets prioritize saving or investing a set amount immediately upon income receipt, ensuring financial goals are met before discretionary spending. Goal-based budget splitting in Pay-Yourself-First strategies enhances financial discipline by directing funds specifically toward targeted objectives such as emergency savings, retirement, or debt reduction.

Monthly Budget vs Pay-Yourself-First Budget for Budget Schedules Infographic