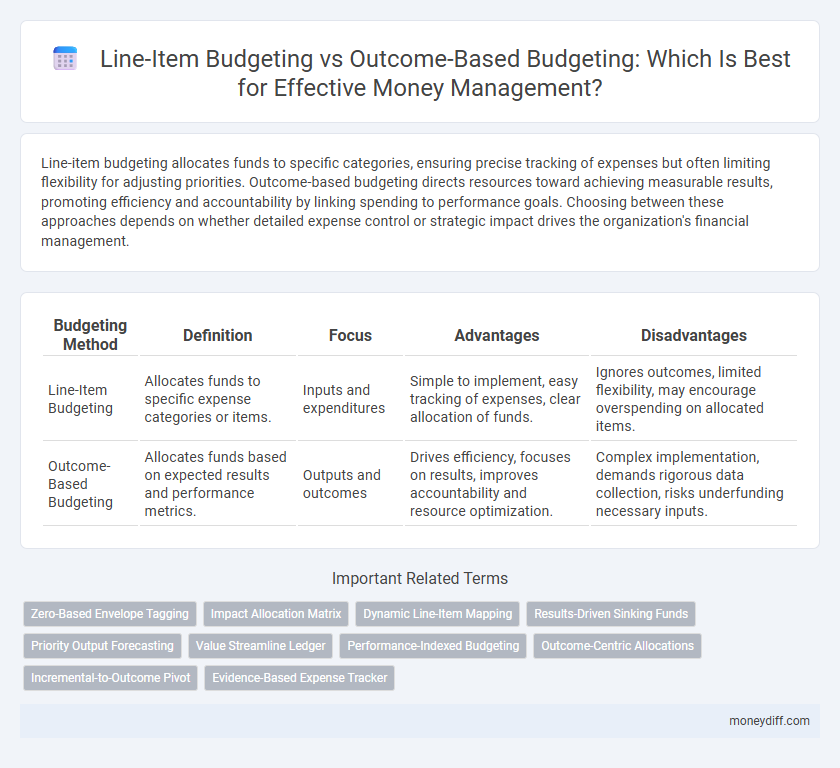

Line-item budgeting allocates funds to specific categories, ensuring precise tracking of expenses but often limiting flexibility for adjusting priorities. Outcome-based budgeting directs resources toward achieving measurable results, promoting efficiency and accountability by linking spending to performance goals. Choosing between these approaches depends on whether detailed expense control or strategic impact drives the organization's financial management.

Table of Comparison

| Budgeting Method | Definition | Focus | Advantages | Disadvantages |

|---|---|---|---|---|

| Line-Item Budgeting | Allocates funds to specific expense categories or items. | Inputs and expenditures | Simple to implement, easy tracking of expenses, clear allocation of funds. | Ignores outcomes, limited flexibility, may encourage overspending on allocated items. |

| Outcome-Based Budgeting | Allocates funds based on expected results and performance metrics. | Outputs and outcomes | Drives efficiency, focuses on results, improves accountability and resource optimization. | Complex implementation, demands rigorous data collection, risks underfunding necessary inputs. |

Introduction to Line-Item and Outcome-Based Budgeting

Line-item budgeting allocates funds based on specific categories or expenses, providing detailed control over financial resources and simplifying tracking for accountability. Outcome-based budgeting focuses on linking expenditures to measurable results and organizational goals, enhancing the ability to evaluate the effectiveness of spending. Both methods serve distinct purposes in money management, with line-item budgeting prioritizing control and transparency, while outcome-based budgeting emphasizes performance and impact.

Key Principles of Line-Item Budgeting

Line-item budgeting centers on detailed allocation of funds to specific categories such as salaries, supplies, and equipment, enabling precise tracking of expenses. This method emphasizes strict control and accountability by monitoring financial inputs rather than outcomes. Key principles include clear categorization, fixed budget amounts for each line item, and regular monitoring to prevent overspending and ensure compliance with fiscal policies.

Understanding Outcome-Based Budgeting

Outcome-Based Budgeting (OBB) allocates funds by linking financial resources directly to expected results, enhancing accountability and strategic focus. Unlike Line-Item Budgeting, which categorizes expenses by specific costs, OBB prioritizes measurable outcomes, enabling organizations to assess performance and adjust spending accordingly. This approach promotes efficient money management by aligning budgetary decisions with organizational goals and stakeholder needs.

Comparing Budgeting Approaches for Money Management

Line-item budgeting allocates funds to specific categories, providing detailed control over expenditures but often lacks flexibility to adjust based on program results. Outcome-based budgeting ties financial resources directly to performance metrics and goals, promoting efficiency by linking spending to measurable outcomes. Comparing these approaches reveals that line-item budgeting ensures accountability through detailed tracking, while outcome-based budgeting enhances strategic allocation by focusing on the impact of funds.

Advantages of Line-Item Budgeting

Line-item budgeting offers precise control over expenditures by allocating funds to specific categories, enhancing transparency and accountability in financial management. It simplifies tracking and auditing processes, making it easier to identify variances and prevent overspending. This method supports detailed financial reporting, which is essential for maintaining budget discipline and facilitating compliance with regulatory requirements.

Benefits of Outcome-Based Budgeting

Outcome-Based Budgeting enhances financial accountability by linking expenditures directly to measurable results, ensuring funds drive strategic goals. It promotes efficient resource allocation by prioritizing programs with tangible impacts, reducing waste and optimizing return on investment. This approach fosters transparency and performance evaluation, enabling informed decision-making and continuous improvement in budget management.

Common Challenges in Implementing Both Methods

Line-item budgeting often struggles with rigidity, limiting flexibility and failing to link expenditures directly to results, while outcome-based budgeting faces challenges in setting measurable goals and accurately attributing financial resources to specific outcomes. Both methods require extensive data collection and analysis, creating administrative burdens and potential resistance from staff unaccustomed to new financial tracking systems. Organizations frequently encounter difficulties in aligning budgeting processes with strategic objectives, causing delays and inefficiencies in resource allocation.

Practical Examples of Line-Item Budgeting

Line-item budgeting allocates funds by specific categories such as salaries, utilities, and equipment, providing clear control over expenses and simplifying financial tracking. For example, a municipal government might allocate $200,000 for road maintenance, $150,000 for public safety equipment, and $100,000 for administrative costs, allowing precise oversight of spending in each area. This method enhances accountability by enabling managers to monitor deviations in each line item, ensuring funds are used exactly as planned.

Real-World Applications of Outcome-Based Budgeting

Outcome-Based Budgeting (OBB) enhances financial efficiency by allocating funds based on measurable program results, driving accountability in sectors such as healthcare, education, and public safety. Governments employing OBB, like Washington State and Texas, report improved service delivery and transparent resource management by linking expenditures directly to specific outcomes. This approach contrasts with traditional Line-Item Budgeting, which focuses on input costs rather than assessing the effectiveness and impact of spending.

Choosing the Right Budgeting Method for Your Financial Goals

Line-item budgeting organizes expenses by specific categories, providing clarity and control over individual costs, ideal for strict expense tracking and accountability. Outcome-based budgeting allocates funds based on expected results, aligning spending with strategic goals and promoting efficiency in achieving financial objectives. Selecting the right method depends on prioritizing either detailed cost management or goal-driven resource allocation to optimize money management.

Related Important Terms

Zero-Based Envelope Tagging

Zero-Based Envelope Tagging integrates zero-based budgeting principles with envelope budgeting by assigning every dollar a specific purpose, ensuring funds are allocated from scratch each period based on actual needs rather than historical spending. This approach enhances money management by combining precise line-item tracking with outcome-focused accountability, optimizing resource allocation and minimizing waste.

Impact Allocation Matrix

Line-item budgeting allocates funds to specific expense categories, providing detailed control but limited insight into performance outcomes, while outcome-based budgeting emphasizes funding programs based on their measurable impacts. The Impact Allocation Matrix enhances outcome-based budgeting by mapping financial resources directly to desired outcomes, enabling transparent tracking of how budget allocations drive specific results and optimize resource effectiveness.

Dynamic Line-Item Mapping

Dynamic Line-Item Mapping enhances traditional Line-Item Budgeting by enabling real-time adjustments and detailed tracking of expenses, improving financial flexibility and accuracy. This method contrasts with Outcome-Based Budgeting by emphasizing granular control over individual expense categories rather than solely focusing on financial results or program outcomes.

Results-Driven Sinking Funds

Line-item budgeting allocates funds to specific categories, providing granular control but often lacking flexibility to adapt to changing priorities, while outcome-based budgeting focuses on achieving specific results by linking expenditures to measurable outcomes. Results-driven sinking funds strategically set aside money over time to finance future obligations, enhancing fiscal responsibility by ensuring funds are available when needed without disrupting annual budgets.

Priority Output Forecasting

Line-item budgeting allocates funds based on specific expense categories, providing detailed control but often lacking clear alignment with overall goals. Outcome-based budgeting prioritizes forecasting the financial requirements needed to achieve defined priority outputs, enhancing resource allocation efficiency and strategic impact.

Value Streamline Ledger

Line-Item Budgeting allocates funds based on specific expense categories, enhancing detailed tracking but often limiting adaptability and strategic focus, whereas Outcome-Based Budgeting prioritizes funding according to expected results and performance metrics, aligning expenditures with organizational goals. Integrating a Value Streamline Ledger enables real-time tracking of financial flows across both budgeting methods, improving transparency and supporting data-driven decision-making for optimized resource allocation.

Performance-Indexed Budgeting

Performance-Indexed Budgeting enhances traditional line-item budgeting by linking financial allocations directly to measurable outcomes, enabling more efficient resource management and accountability. This approach prioritizes funding based on program performance metrics, ensuring money is directed toward initiatives that demonstrate tangible results and impact.

Outcome-Centric Allocations

Outcome-centric allocations in budgeting prioritize funding based on measurable results and organizational goals, ensuring resources are directed towards initiatives with the highest impact. This approach contrasts with traditional line-item budgeting by focusing on performance metrics and accountability rather than merely tracking expenses by category.

Incremental-to-Outcome Pivot

Line-item budgeting itemizes expenses based on historical allocations, often leading to incremental increases without direct linkage to program outcomes, whereas outcome-based budgeting allocates funds tied to measurable results, driving a strategic shift from input control to performance accountability. This incremental-to-outcome pivot enhances resource efficiency by prioritizing expenditures that directly contribute to defined goals, enabling organizations to optimize financial management and improve program effectiveness.

Evidence-Based Expense Tracker

Line-item budgeting allocates funds by specific categories, offering granular control over expenses but often lacking direct links to performance outcomes. Outcome-based budgeting prioritizes funding based on measurable results, leveraging evidence-based expense trackers to ensure spending aligns with organizational goals and enhances financial accountability.

Line-Item Budgeting vs Outcome-Based Budgeting for money management. Infographic